e transforms into a dynamic financial tool—providing tax-efficient growth, liquidity, and protection. In this article, we’ll uncover why this asset deserves a central role in your financial strategy and how it can redefine your approach to wealth building.

What Is Cash Value Life Insurance?

Is another name for permanent life insurance that pays tax-deferred interest to the policyholder. Universal life, indexed universal life, variable life, and whole life are all types of permanent insurance that can be classified as cash value insurance. Term life insurance, the most common and least expensive type of life insurance, doesn’t earn any cash value.

When you pay an insurance premium on a cash value policy, a portion of the premium goes toward the death benefit (aka the face value). The remainder of the premium goes toward a built-in savings component of your policy (aka the cash value).

So, why not just buy less expensive term life insurance and invest the difference?

- Cash value life insurance comes with a number of living benefits. (Term life insurance offers no living benefits.)

- As an interest-earning asset, cash value life insurance is safer and offers more guarantees than most investment options.

- Is a phenomenal way to capture opportunity cost.

At Paradigm Life, we focus on Whole Life Insurance, the most stable and predictable form of cash value life insurance. As part of the Perpetual Wealth Strategy™, Whole Life Insurance integrates guaranteed growth, tax advantages, and liquidity, forming the foundation of your long-term financial plan.

Benefits of Cash Value Life Insurance

Offers more than just a death benefit—it’s a versatile financial tool with living benefits that can be used during your lifetime. These living benefits make it an essential part of any financial portfolio:

- Certainty: When structured through mutual insurance companies, Whole Life Insurance policies offer a guaranteed rate of return, ensuring consistent, predictable growth regardless of market conditions.

- Control: Your cash value is protected from lawsuits, judgments, and asset searches. Unlike many other financial products, your policy is a private contract between you and your insurer, offering unmatched privacy and security.

- Liquidity: Access your cash value without penalties, restrictions, or age requirements. Whether you need funds for emergencies, investments, or major purchases, cash value life insurance offers unparalleled flexibility.

- Protection: Cash value in Whole Life Insurance is insulated from market volatility. While stocks and real estate may fluctuate, your cash value continues to grow consistently.

- Cash flow: Cash value life insurance can supplement or fund retirement, offering tax-free income streams through policy loans or withdrawals

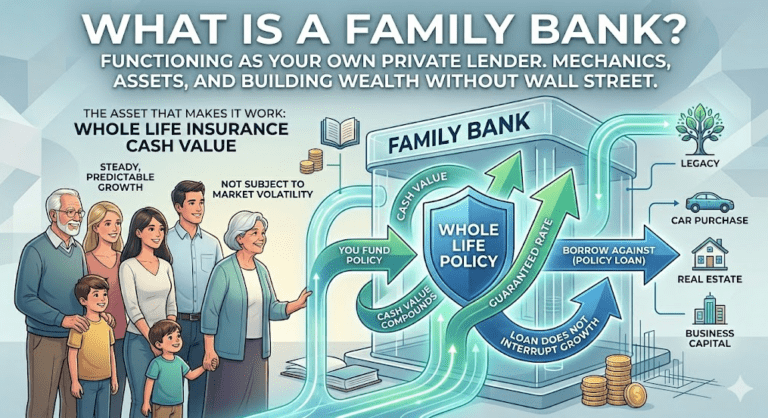

- Legacy: Cash value life insurance is ideal for private family banking and can allow you to pass on wealth the same way the Rockefeller family has. When policies are purchased inside an Irrevocable Life Insurance Trust, the cash value of older policies can pay for premiums on newer policies in perpetuity.

How Do I Access My Cash Value?

Once your cash value accumulates, you can access it through withdrawals or policy loans:

- Withdrawals: You can withdraw cash value directly, but keep in mind that any withdrawal exceeding your premium payments (basis) may be taxable. Additionally, withdrawals reduce the policy’s growth potential and death benefit.

- Policy loans: Borrowing against your cash value is tax-free, and you still earn interest on the full amount of your cash value—even the amount you borrow. Loans don’t require pre-approval or credit checks, and you set your own repayment terms.

Example: If you have $100,000 in cash value and take out a $20,000 loan at 5% interest, your policy continues earning guaranteed interest and dividends on the full $100,000. This ensures your money keeps working for you while providing liquidity.

What Can I Use My Cash Value for?

Cash value life insurance offers unmatched flexibility and serves as a valuable resource for achieving a wide range of financial goals. Through Paradigm Life’s Perpetual Wealth Strategy™, cash value becomes more than savings—it becomes a dynamic tool for building, managing, and protecting your wealth.

College tuition

Rising college tuition rates and student loan burdens can make funding education a challenge. With cash value life insurance, you can finance education expenses without the restrictions or penalties associated with traditional student loans. By borrowing against your policy, you maintain control over repayment terms and continue earning interest on your full cash value, even while the loan is in use.

When you take out a cash value insurance policy on a child, you typically lock in a low premium because children are young and generally very healthy. Use a whole life insurance policy and you’ll lock in that low rate for the remainder of your child’s life.

Business Capital

For entrepreneurs, cash value life insurance is a reliable source of business funding. It provides access to liquidity for launching new ventures, expanding operations, or covering unexpected expenses. Unlike bank loans, policy loans don’t require credit checks or lengthy approval processes, allowing you to act quickly while enjoying the financial advantages of recapturing interest within your policy. It can be used to generate business capital, cover expenses, create a business succession plan or protect key partners.

Investment Opportunities

When opportunities arise, having immediate access to funds can make all the difference. Cash value life insurance provides liquidity, enabling you to capitalize on investments in real estate, stocks, or other assets. Each dollar borrowed from your policy continues to earn interest, effectively allowing your money to work in multiple ways at once—funding your investment, growing your policy, and increasing your wealth.

Real Estate

From down payments to property repairs, cash value life insurance is an ideal funding solution for real estate ventures. Policy loans offer the advantage of quick access to funds, often within days, giving you the ability to make competitive cash offers or address unexpected expenses. Additionally, the predictable growth of your cash value provides stability in fluctuating real estate markets.

Family Purchases

Big-ticket items like cars, vacations, or home improvements can be funded smartly through cash value life insurance. Instead of depleting savings or taking out traditional loans, policy loans allow you to preserve your assets and minimize opportunity cost. Even while using a portion of your cash value, your policy continues to earn interest, making it a financially strategic choice.

Retirement Income

Cash value life insurance,also called a life insurance retirement plan (LIRP) provides a reliable income source during retirement, especially during market downturns. Acting as a volatility buffer, Whole Life Insurance allows you to use policy loans or withdrawals to supplement retirement income without tapping into investment accounts during unfavorable market conditions. For those who’ve maxed out contributions to qualified plans, cash value policies offer additional tax-advantaged retirement savings.

Using cash value for retirement is likely the only scenario in which you purposely utilize policy loans without the intent to pay them back. Instead, you enjoy the cash value of your policy tax-free to fund your retirement. When you pass away, your outstanding loans and interest are deducted from your death benefit.

Does this mean less for your beneficiaries? Yes. But is the goal in this case to leave a death benefit or to fund retirement?

Paying Policy Premiums

Cash value policies often reach a point where the interest earned on the accumulated cash value is sufficient to cover a policy’s premiums. They are referred to as “self-funding” insurance policies.

When you own a whole life insurance policy, where your premiums are set for life, once your policy is at a “self-funding” stage, you effectively stop paying your premiums out of pocket—the policy itself pays for its premiums. This is an especially effective use of cash value in the later years of your policy, where you are likely retired and no longer have a steady source of income outside funds set aside for retirement.

Is It Worth the Cost?

Cash value life insurance costs more than term life insurance, but its benefits often far outweigh the expense for individuals focused on long-term financial security and wealth-building. With proper structuring, it can become the cornerstone of a successful financial portfolio, offering stability, growth, and protection for current and future generations.

Determining If Cash Value Life Insurance Is Right for You

- For temporary coverage needs:

If your primary goal is to provide a death benefit for a specific period, term life insurance may suffice. It’s more affordable initially but offers no cash value or living benefits. If you outlive the term, premiums are lost, and renewing coverage later typically results in higher costs. - For lifelong security:

Permanent life insurance guarantees a death benefit no matter when you pass away. Although cash value growth may be slower if the policy prioritizes the death benefit, it ensures your family receives financial protection while offering some living benefits. - For living benefits and wealth building:

A cash value policy, especially Whole Life Insurance, is ideal for those looking to grow tax-advantaged wealth, access liquidity, or create a financial legacy. Structuring the policy for rapid cash value growth enables you to leverage living benefits for goals like retirement, investments, and family needs.

The Importance of Proper Structure

The value of cash value life insurance lies in how it’s structured:

- Prioritizing the death benefit: Focuses on maximizing the amount left for beneficiaries but may result in slower cash value growth.

- Prioritizing living benefits: Allocates premiums to the cash value, within IRS limits, to avoid Modified Endowment Contract (MEC) status. This ensures accelerated growth and retains the policy’s tax advantages.

Paradigm Life Perspective: At Paradigm Life, we emphasize the importance of designing a policy that aligns with your financial goals. Whole Life Insurance, as part of our Perpetual Wealth Strategy™, is uniquely suited for creating a balance between protection, growth, and liquidity, ensuring your wealth works for you both now and in the future.

Structuring a Policy for Rapid Growth

To maximize the living benefits, consider Paid-Up Additions (PUA)—a rider that allows you to overfund your Whole Life Insurance policy. By contributing extra funds early, PUAs accelerate cash value growth, increase earnings through interest and dividends, and enhance liquidity for financial opportunities.

PUAs are exclusive to Whole Life Insurance, which offers:

- Fixed premiums: Predictable costs.

- Guaranteed growth: Steady returns shielded from market volatility.

- Stability: Reliable performance compared to market-linked policies like Universal Life.

For rapid cash value growth and long-term financial flexibility, Whole Life Insurance with PUAs is the most effective option.

Is Cash Value Life Insurance Right for Me?

This can be a powerful financial tool for individuals who:

- Have a steady income and can consistently pay premiums.

- Have long-term financial goals that require increased cash flow and liquidity.

- Are in good health to qualify for a policy.

- Are proactive about managing their financial future and leveraging the living benefits of a policy.

A properly structured cash value life insurance policy is key to unlocking its full potential. By tailoring the policy to your specific goals, you can create a reliable foundation for wealth-building, financial security, and long-term flexibility.

At Paradigm Life, we specialize in customizing policies to align with your financial goals. Our expert Wealth Strategists are here to answer your questions, provide customized illustrations, and help you design an actionable plan to achieve financial independence and security.