Most financial content is written for people trying to get to a million dollars. Very little is written for people who’ve arrived. Here’s what the map looks like on the other side.

The Question Nobody Prepared You For

You optimized for a number.

For years, maybe two decades, every financial decision ran through the same filter: does this get me closer?

The savings rate, the allocation, the reinvested dividends, the foregone vacations. The framework was rigorous. The discipline was real. And eventually, the number arrived.

So did the question nobody prepared you for: now what?

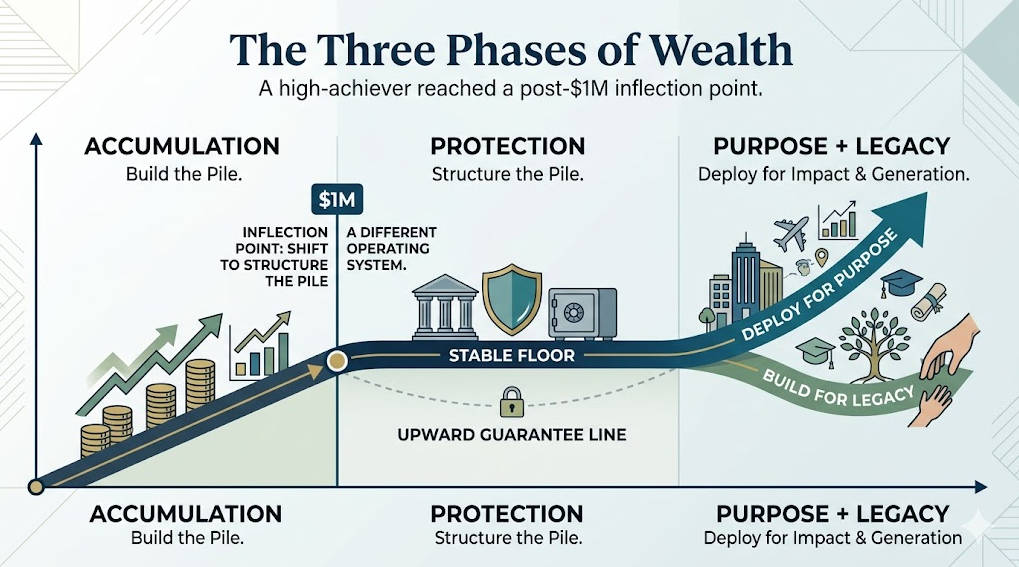

This isn’t a failure of imagination. It’s a design specification of the accumulation phase; it was built to get you here, not to tell you what to do once you arrived.

The tools that served you so well for so long; save more, grow the pile, minimize drag, were built for a specific job. That job is done. And standing at the finish line with a new set of questions isn’t a sign that something went wrong.

It’s a sign that you’re at a real inflection point. One that requires a different operating system than the one that got you here.

That’s what this piece is. Not a celebration, not a warning, a map for the next phase, written for people who’ve actually crossed the threshold.

What the r/FIRE Community Is Actually Telling You

The post-accumulation question isn’t niche. The evidence for this is sitting in plain view.

In recent months, the r/FIRE community; one of the most financially disciplined audiences on the internet, has generated more than 2,600 combined engagement points on a single category of topic: what happens after you’ve built the wealth.

The specific breakdown matters:

- Retirement isolation: 1,619 engagement points — the dominant signal

- Generational wealth: 1,013 engagement points — the aspirational frame

- Spending psychology: 205 engagement points — the friction point

Read the ranking order. Isolation isn’t a mood, but a structural problem. The social and professional identity you built around the process of accumulating wealth doesn’t automatically transfer to holding it.

The goal was the organizing principle. When it’s achieved, the organizing principle disappears.

Generational wealth is the direction people are looking for. Not just “I have money” but “I’ve built something that continues past me.” That aspiration is real and it’s dominant; over a thousand engagement points on this topic alone, in an audience that is notoriously hard to impress.

Spending psychology is smaller in volume but not smaller in significance. The people who’ve spent 15 years training themselves not to spend money discover that the training doesn’t switch off when the financial case for spending has been made.

Permission is a structure problem masquerading as a psychology problem.

These three signals are not separate concerns. They’re the same inflection point viewed from three angles. And every financial framework written for accumulation is completely silent on all three.

The Accumulation Framework Has a Ceiling

There’s nothing wrong with the accumulation framework. It did exactly what it was designed to do.

The problem is treating a phase-specific tool as a permanent operating system. The accumulation framework was optimized for a clear metric: grow the pile. Every decision; savings rate, expense minimization, portfolio allocation toward aggressive growth, was evaluated against that single variable.

Post-$1M, that same framework begins to work against you if you don’t update it:

Hyper-frugality that was rational during accumulation becomes an identity constraint in wealth-holding. The psychological muscle you built for conservation doesn’t distinguish between “conserving to build” and “conserving out of habit.”

That distinction has to be made deliberately, or the habit wins by default.

Aggressive growth allocation that made sense at 35 carries a fundamentally different risk profile at 55 when distribution is a real near-term need. A 40% drawdown that was an inconvenience during accumulation becomes a structural problem when it intersects with actual spending requirements.

A growth-optimized portfolio is not automatically a purpose-optimized portfolio. Maximizing return on a number is a different problem than deploying capital toward what you actually want the money to do for the rest of your life and beyond.

The ceiling isn’t a failure. It’s a natural end to a phase. The question is what you build next.

The Three Things That Have to Be Answered — In Order

Here’s the structure of the post-accumulation operating system. Not three simultaneous priorities, three sequential ones. The order matters because each one is the precondition for the next.

1. Protection: Is the Floor Stable?

Before purpose, before legacy, before any of the more interesting questions, the foundation has to be sound.

This means a portion of your wealth in assets that don’t move with markets. Not “diversified.” Not “lower beta.” Non-correlated; money that holds its value whether the S&P is up 20% or down 40%, because it isn’t connected to the S&P at all.

It means a guaranteed growth floor, not just an average expected return. There is a significant practical difference between “my portfolio averages 7% annually” and “a portion of my wealth is contractually guaranteed to grow.”

One is a probability distribution. The other is a certainty. Post-$1M, certainty on your floor is not a conservative instinct, it’s a structural requirement.

It means liquidity that doesn’t require selling assets at the wrong time. The ability to access capital without triggering a taxable event and without disrupting the compounding base is worth a meaningful premium at this stage.

Until this layer is in place, the purpose conversation is premature. You cannot build purposefully on an unstable floor.

(See: Money That Holds Its Value When Markets Don’t — how non-correlated assets function as a stability layer.)

2. Purpose: What Is the Money For Now?

This is the question the accumulation phase never asked. It’s also the question that creates the disorientation.

“Purpose” at this level isn’t a retirement hobby or a philanthropic impulse, though it may include both. It’s a financial identity question: what role do you want your capital to play from here forward?

For most high-achievers who’ve crossed the accumulation threshold, the honest answer has three components: maintaining lifestyle without anxiety, funding the next thing (the next business, the next investment, the next chapter), and building something that matters for the generation that follows.

The specifics vary. The structure of the question is consistent.

The critical mistake is treating purpose as a feeling to manage rather than a structure to build. Aspiration without architecture is just intention. Purpose at this level requires an operating system; a set of rules and structures that translate “what I want the money to do” into “how the money is actually deployed.”

3. Legacy: What Does This Look Like in 30 Years?

The generational question is the one most post-accumulation frameworks completely avoid. Not because it’s unimportant, the FIRE data suggests it’s the second-highest concern in this audience, but because it requires a different kind of infrastructure than most financial products are designed to provide.

The wealthiest families don’t just accumulate and distribute. They build systems. The distinction is significant: distribution is an event; a system is something the next generation can operate, borrow from, and pass forward in turn.

The family bank concept; a whole life policy structure designed to maximize borrowable cash value and extend across generations, is one of the few instruments built specifically for this purpose.

It isn’t an estate planning product. It isn’t a death benefit play. It’s a living capital system: money that compounds, can be borrowed against without interrupting that compounding, and can be structured so the next generation inherits not just a payout but a functional financial infrastructure.

(See: [What Is a Family Bank?] — the mechanics, who it works for, and how Paradigm structures these policies.) *Note to Tyler hyperlink this article when it’s published: https://docs.google.com/document/d/1H7xFZ1j1Jj8SBFStSzpoWhKSWLR0gWU1v0F8F-_Jz0Y/edit?tab=t.0#heading=h.qx438sanpagl

You’ve built it. Now you need a system for what comes next.

What Most Financial Advice Gets Wrong at This Stage

The dominant post-accumulation advice in the financial industry is portfolio mechanics: shift from growth to income, reduce equity exposure, add bonds and dividend-paying assets, target a sustainable withdrawal rate.

That’s not bad advice for the mechanics of a portfolio. It is almost entirely insufficient for the actual problem. The accumulation framework sold you on a number: $1M, $2M, $5M, whatever your target was.

Most of the advice on the other side of that number is still operating in the same lane: you have more money now, so here’s how to manage more money. What’s missing is the architectural question: is the structure of this wealth doing what you actually want it to do?

The specific gaps:

A guaranteed floor that isn’t correlated to the market. Standard portfolio rebalancing shifts the ratio of volatile assets. It doesn’t remove market correlation from the equation, it reduces it. Non-correlated assets don’t reduce market correlation. They eliminate it for that portion of wealth. These are structurally different outcomes.

A capital system the next generation inherits functionally, not just financially. An inheritance is a distribution event. A family bank is an operating infrastructure. One gives the next generation a number. The other gives them a system they can use, compound, and extend. Most estate planning is optimized for the former.

A structure that lets you deploy capital for purpose without destabilizing the base. The policy loan mechanic; borrowing against cash value while it continues to compound, solves a problem that portfolio drawdown strategies don’t address: how do you spend capital without depleting the base that the spending is supposed to be funded by?

The answer is structural, not behavioral.

The Spending Psychology Problem Is Actually a Structure Problem

Here’s the finding from the FIRE community data that doesn’t get enough attention: people who’ve hit $1M frequently can’t spend.

Not because the math says no. The math often says yes, sometimes emphatically. The problem is psychological, but its source is structural. The identity that built the wealth was organized around conservation.

Every spending decision for 15 or 20 years ran through a filter that asked: does this move me closer to the goal, or further away? That filter doesn’t automatically switch off when the goal is reached. It persists as a default cognitive operating mode.

The financial industry’s answer to this is usually behavioral; work with a therapist, give yourself permission, reframe your relationship with money.

That advice isn’t wrong. It’s just incomplete.

The structural answer is more durable: build a system where the act of spending doesn’t deplete the base.

The policy loan mechanic does this. When you borrow against your whole life cash value, you’re not withdrawing money, you’re borrowing against collateral while that collateral continues to compound at a guaranteed rate. You deploy capital without reducing your base. The permission to spend is built into the structure itself, not into a behavioral reframe.

This is why the family bank concept resonates with post-accumulation high-achievers in a way that standard drawdown strategies don’t. It’s not just a more efficient borrowing mechanism. It’s a structural answer to a question the accumulation framework never asked: how do I deploy capital without diminishing what I’ve built?

What the Post-$1M Operating System Looks Like in Practice

For the high-achiever at or past the $1M threshold, the post-accumulation operating system typically has four components:

A guaranteed cash-value layer. A specially designed whole life insurance policy, structured to maximize early cash value rather than death benefit. This is the non-correlated floor; the portion of wealth that compounds at a guaranteed rate regardless of market conditions and can be borrowed against without interrupting that compounding.

A clear capital deployment framework. A deliberate decision structure for how capital is allocated across categories: what percentage lives in the guaranteed floor, what percentage is in market-correlated growth assets, what is liquid and deployable for near-term purpose. The ratio varies by situation. The structure is consistent: these categories need to be explicit, not default.

A generational infrastructure. A policy structure that extends to the next generation as a functional capital base, something they can borrow from, repay, and compound further, not just an inheritance event. This requires design decisions made now, not after the fact.

A regular architecture review. Quarterly or annual review of the structure against the purpose question: is this money still doing what I want it to do? Not a portfolio performance review, an architecture review. The question isn’t “did I beat the benchmark?” It’s “is the structure aligned with what the money is for?”

This is not a portfolio rebalancing conversation. It’s a fundamentally different kind of financial conversation, one that starts with purpose and works backward to structure, rather than starting with returns and working forward to allocation.

The Question Worth Asking

The accumulation phase had a clean organizing question: am I on track to reach my number?

It was a good question. It was tractable, measurable, and motivating for the better part of two decades.

The post-accumulation phase has a harder one, and it doesn’t resolve as cleanly: is my wealth structured to do what I actually want it to do, now, and for the generation after me?

Most high-achievers who’ve crossed the threshold haven’t had that second conversation yet. Not because they don’t care about the answer, the FIRE engagement data suggests they care quite a lot. But because the financial infrastructure they’ve been using was built to answer the first question, not the second. And the advisors they’ve worked with have mostly been trained in the same framework.

The conversation about what comes after accumulation, about structure, purpose, floor, and legacy, is a different discipline. It requires different tools and a different kind of thinking.

That’s the conversation Paradigm was built for.

H2 Ready for a different kind of financial conversation?

Paradigm Life works with high-achievers at the post-accumulation inflection point; people who’ve built real wealth and want a structure that matches their actual goals, not just a bigger version of the one that got them here. Start with a free strategy call.

Not ready for a call yet?

Take this Quiz to determine the strength of your current wealth strategy. In just a few minutes you’ll have the answer.