Were you taught to believe that all debt is bad and that a high credit score with zero debt is the ultimate financial goal? While this mindset is common, it’s not how wealth is built. In fact, those who have achieved significant financial success often use strategic debt to their advantage. One powerful tool in this approach is using a policy loan from a whole life insurance policy.

With a policy loan, you can access your policy’s cash value tax-free, giving you the flexibility to fund investments, cover expenses, or create additional income streams—all while your policy continues to grow. This guide will show you how policy loans work, their unique benefits, and why they’re a game-changer for anyone looking to build wealth and financial independence.

What are Life Insurance Policy Loans?

A life insurance policy loan is a unique financial tool that allows you to borrow against the cash value of your whole life insurance policy. Here’s how it works:

- Cash value growth: When you purchase a whole life insurance policy from a mutual insurance company, your policy builds cash value through guaranteed interest and potential non-guaranteed dividends. These earnings, typically in the 4%-6% range, accumulate over time, creating a powerful financial resource.

- Tax-free access: Unlike traditional loans, you can access this cash value tax-free at any time through a policy loan. Think of it as borrowing from your personal financial safety net.

- Repayment flexibility: Policy loans offer unmatched flexibility—you set your repayment terms. If you pass away before repaying the loan, the balance is simply deducted from your policy’s death benefit, ensuring your financial legacy remains intact.

- No credit impact: Since you’re borrowing against your own funds, policy loans don’t require credit checks and won’t affect your credit score.

Using a policy loan is a private contract between you and your insurance company, making it an easy and secure way to access funds without the need for external lenders. It’s a strategic way to leverage your own wealth while keeping your financial goals on track.

Can I Default on a Life Insurance Loan?

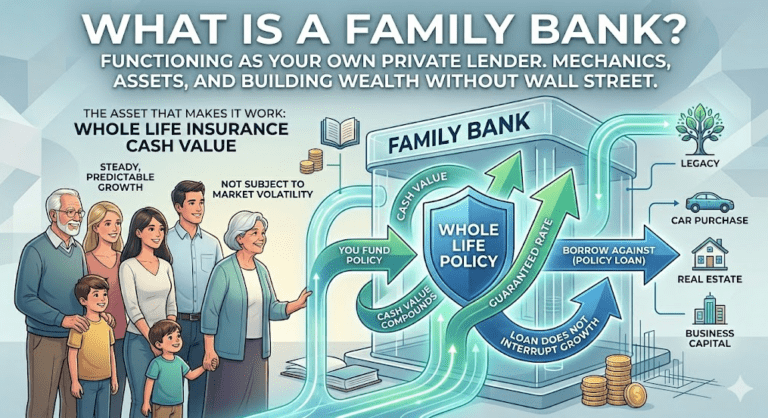

Unlike a typically bank loan or credit card purchase, you’re not relying on anyone else’s money when you use a policy loan. You’re borrowing your own money, plus interest and dividends, from your insurance policy. The policy itself (the death benefit) is the collateral for your loan.

Your insurance company won’t let you take out a loan on your whole life insurance policy for more than the amount of cash value you have in the permanent life insurance policy (the amount in your “bank”). And because the death benefit will exceed the cash value in any whole life insurance policy (otherwise it becomes a Modified Endowment Contract, or MEC) there is always money available for the insurance company to recoup the amount of the loan.

If I’m Borrowing My Own Money, Why Not Just Pay Cash?

It’s easy to misunderstand the benefits of using a policy loan from a whole life insurance policy. Many people think, “Why take a loan when I can just save up and pay cash?” or, “I don’t have heirs, so the cash value component doesn’t matter to me.” The reality is that whole life insurance offers unique advantages that other savings tools can’t match, regardless of your life stage or financial goals.

Here are four key reasons why using a policy loan can be more beneficial than relying on cash or traditional savings accounts:

1. The “And” Asset Advantage

When you save money in traditional accounts like savings accounts, CDs, or the stock market, you earn interest only on the balance in the account. If you withdraw funds for a purchase, your savings decrease, and so does your earning potential. It’s a choice between earning money or spending money.

With whole life insurance, you don’t have to choose. Your policy earns interest and potential non-guaranteed dividends on the full cash value, even when you borrow against it. This means your interest continues to compound as if you hadn’t taken a loan, allowing your wealth to grow exponentially over time.

By using a policy loan, you can:

- Earn on every dollar in your policy.

- Spend on what you need—whether it’s a car, real estate, or business expenses.

- Avoid interrupting the compounding growth of your wealth.

2. Double (or Triple) Duty for Your Dollars

Imagine taking a policy loan to fund a business investment or pay for advanced education. These activities generate their own returns, whether it’s through increased income, business growth, or personal skill development.

Meanwhile, your whole life insurance policy continues to grow, earning interest and potential dividends. This means every dollar you contribute works twice as hard—or even three times as hard—by simultaneously:

- Growing within your policy.

- Supporting external investments or goals.

- Generating additional financial returns.

Why Choose a Policy Loan Over Cash?

The ability to earn money and spend it sets whole life insurance apart from other savings tools. With a policy loan, you don’t lose out on compounding growth, and your dollars work harder to help you achieve your financial goals.

Paradigm Life’s Wealth Strategists can help you explore how policy loans can fit into your broader financial strategy, empowering you to maximize your wealth-building potential while maintaining financial flexibility.

Related: See the “AND” asset in action here.

2. Tax-Free Retirement Income

It’s often said that only two things in life are certain: death and taxes. But with mutually funded whole life insurance, the “taxes” part comes with flexibility. Whole life insurance policies offer unique tax advantages that allow you to maximize your retirement income while keeping more of your hard-earned money.

Key Tax Benefits of Whole Life Insurance

- Tax-deferred growth: The interest and potential non-guaranteed dividends earned within your policy grow on a tax-deferred basis. This means your cash value can compound uninterrupted, giving you a powerful way to accumulate wealth over time.

- Tax-free access: Unlike withdrawing cash value directly, which may trigger taxes, policy loans allow you to access your policy’s cash value tax-free. This feature makes policy loans an excellent tool for funding retirement without worrying about taxable income.

Retirement Without Penalties

What if you want to retire before age 59½? Traditional qualified retirement accounts like IRAs and 401(k)s penalize early distributions with an additional 10% fee, plus taxes. Even after age 59½, these accounts are subject to income tax on withdrawals.

With whole life insurance, there are no age restrictions or penalties. You can use policy loans at any time, giving you greater flexibility to retire on your own terms.

Protecting Your Income from Tax Increases

The assumption that you’ll be in a lower tax bracket during retirement may not hold true—especially if you continue earning income through investments, consulting, or freelancing. With rising tax rates and inflation, relying solely on taxable retirement distributions could leave you with less than expected.

Policy loans shield your retirement income from taxes, ensuring you can maintain your lifestyle without giving a significant portion to the government.

What About Loan Repayments?

If you use policy loans to supplement retirement income, the goal is to have enough cash value to continue borrowing for the rest of your life, much like distributions from a qualified retirement account. Any unpaid loan balance is deducted from your policy’s death benefit when you pass away.

While this may reduce the amount your heirs receive, the tax-free income you enjoyed during retirement could more than offset this reduction, depending on your financial goals and family’s needs.

Why Policy Loans Make Sense for Retirement

Whole life insurance offers a unique way to supplement your retirement without the tax burdens and penalties associated with other plans. By using policy loans strategically, you can maintain financial independence, maximize your retirement income, and protect your wealth from taxes—all while leaving a legacy for your loved ones.

At Paradigm Life, our Wealth Strategists can help you integrate policy loans into your retirement strategy to achieve long-term financial security.

3. Life Insurance Policy Riders

One of the most valuable features of a whole life insurance policy is the ability to add policy riders. These riders function as additional layers of protection or benefits, allowing you to customize your policy to fit your unique financial needs and goals. Some riders are included at no extra cost, while others can be added for a modest fee, providing significant value and flexibility. In certain situations, these riders can also help increase your cash flow.

The Disability Waiver of Premium Rider

Think of the disability waiver of premium rider as insurance for your insurance policy. If your policy is your personal financial bank, this rider ensures that your bank stays open—even if life throws you an unexpected curveball.

If you become disabled and unable to pay your policy premiums, the insurance company will cover the premiums for you. This guarantees that your policy remains active, so you continue to:

- Earn interest and potential dividends.

- Access tax-free policy loans whenever needed.

Imagine being unable to work due to a disability and relying on savings. Each withdrawal diminishes your balance, reducing the interest you earn. With a whole life insurance policy and the disability waiver of premium rider, your compound interest continues to grow, ensuring your financial stability even during challenging times.

The Accelerated Death Benefit Rider

Also known as the terminal illness or chronic illness rider, the accelerated death benefit rider provides you with an advance on your death benefit if you face a serious illness.

This rider allows you to:

- Receive funds in the form of a lump sum or monthly payments.

- Continue earning interest and dividends on your policy.

- Access policy loans for additional financial flexibility.

Imagine the stress of relying on savings to fulfill your final wishes. With the accelerated death benefit rider, your life insurance company provides you with extra cash to focus on what matters most—whether it’s creating unforgettable memories with loved ones or checking off your bucket list.

The Power of Riders in Financial Planning

Policy riders enhance the value and versatility of your whole life insurance policy. Whether it’s ensuring your policy remains active during a disability or giving you financial freedom during a serious illness, riders provide added protection and peace of mind.

At Paradigm Life, our Wealth Strategists can help you customize your policy with the right riders to fit your financial goals and ensure your life insurance is working harder for you.

4. The Death Benefit

The primary purpose of a whole life insurance policy is to provide a death benefit for your beneficiaries. While many policies are structured to maximize cash value and the policy’s “banking” potential, the death benefit remains a crucial feature, ensuring your loved ones are financially secure.

How the Death Benefit Works with Policy Loans

When you take a policy loan, the death benefit serves as collateral. This means that if you pass away before repaying the loan, the outstanding balance is deducted from the death benefit, and your beneficiaries receive the remainder.

For example:

- You take a $50,000 policy loan to purchase a truck.

- Your whole life insurance policy has $75,000 in cash value and a $500,000 death benefit.

- If you pass away before repaying the loan, your beneficiaries would receive $450,000 (the death benefit minus the $50,000 loan).

- The remaining $25,000 in cash value is recouped by the insurance company.

Compare this scenario to withdrawing $50,000 from a $75,000 savings account to pay for the truck. In that case, your beneficiaries would inherit only $25,000. The difference is clear: with whole life insurance, your wealth works harder, ensuring greater financial security for your loved ones.

The Death Benefit: A Legacy of Financial Security

Even when structured for cash value growth, the death benefit ensures your family receives substantial support. Whether you’re using policy loans for major purchases, investments, or retirement, your life insurance policy protects your loved ones and leaves a lasting legacy.

At Paradigm Life, we help you design whole life insurance policies that strike the perfect balance between cash value and death benefit, empowering you to enjoy financial freedom while safeguarding your family’s future.

Are Life Insurance Loans Right for You?

Traditional financial advice often falls short when it comes to building lasting wealth. By leveraging policy loans within a whole life insurance policy, you can take control of your finances, acting as your own personal bank. This strategy allows you to earn compound interest and potential dividends while maintaining access to your cash for investments, major purchases, or unexpected needs.

With the death benefit serving as collateral, policy loans eliminate the risk of default or traditional debt burdens. Combined with customizable riders, your whole life insurance policy becomes a versatile tool for generating cash flow and protecting your family’s financial future.

Ready to take the next step? Explore our free eCourses or schedule a complimentary virtual consultation with one of our Wealth Strategists today. Let us show you how to turn your life insurance into a cornerstone of your financial success.