Most articles about cash flow assets give you a list. Real estate. Dividend stocks. Bonds. Maybe a note about REITs. The list is not wrong, but it answers the wrong question.

The question most high earners actually face is not which cash flow assets exist. It is whether the assets they already own, the rental property, the equity positions, the business distributions, the brokerage account, are working together as a coordinated income system, or simply coexisting in the same portfolio.

That distinction determines whether your cash flow holds up under pressure. And it is the one most “passive income” guides skip entirely.

This article covers both: what cash flowing assets are, how the main categories compare, and more importantly, how to structure assets that generate cash flow into a system that performs the way you need it to.

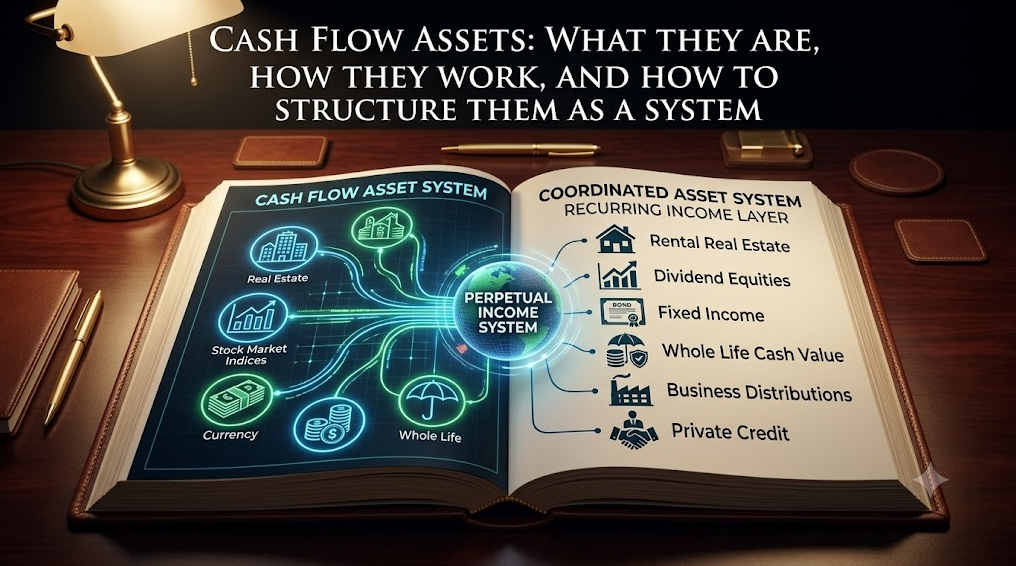

What Are Cash Flow Assets?

A cash flow asset is any asset that generates recurring income independent of active labor input. You own it. It pays you. The income does not require you to show up.

That definition covers a wide range of instruments, rental properties, dividend-producing equities, bonds, whole life insurance cash value, business equity distributions, and private credit arrangements. The category is broader than most people treat it.

What the definition does not include: appreciation. An asset that grows in value but does not distribute income is not a cash flow asset, it is a growth asset. Both matter in a complete wealth system. They are not interchangeable.

Conflating the two is the most common structural error in high-net-worth portfolios: equity in a business that doesn’t distribute, real estate that’s appreciating but not cash-flowing, retirement accounts accumulating but not distributing. These are valuable positions. They are not generating cash flow today.

Within the Perpetual Wealth Strategy™ framework, cash flow assets form one of four Financial Dimensions. They are not the whole system, but they are load-bearing. A wealth structure without a coordinated cash flow layer is exposed in ways that only become visible when a disruption actually arrives.

The Main Categories of Cash Flow Assets

Real Estate (Rental Income)

Direct rental income from residential or commercial property is the category most people name first. Done well, rental real estate produces reliable cash flow and builds equity simultaneously.

Done poorly, it produces the appearance of cash flow while consuming capital in management overhead, vacancy, repairs, and tax friction.

The number that matters is net operating income, what you actually keep after expenses, not gross rent. The gap between those two numbers is larger than most investors model before acquiring the asset.

The other honest note: rental real estate is not passive in the way a dividend stream is. A building requires operational attention. If you own it directly, you are managing an operating asset, not clipping a coupon. This is not a reason to avoid, it is a reason to factor it accurately into your cash flow system design.

Dividend-Producing Equities

Dividend stocks, dividend ETFs, and real estate investment trusts (REITs held as securities) produce income through regular distributions. The liquidity is high, you can exit these positions in a trading session. The management overhead is low. The income is predictable within a reasonable range.

The structural consideration is tax treatment: qualified dividends and ordinary dividends are taxed differently, and REIT distributions carry their own rules. None of this is a reason to avoid the category, it is a reason to know the actual after-tax yield, not the headline rate.

The deeper tension is between income-now and growth-deferred. A high-yield dividend portfolio can be constructed, but it typically trades some portion of appreciation potential to generate current income. That is a legitimate trade, if it is made deliberately, with full awareness of the tradeoff.

Fixed Income (Bonds, Notes, Private Credit)

Government bonds, corporate bonds, and private credit arrangements generate interest income on a defined schedule. The role of this category in a cash flow system is predictability and capital preservation, not growth, not high yield.

For a Sovereign CEO or legacy-stage investor calibrating a structured portfolio, fixed income earns its place as the stability layer. It is not exciting. It performs when everything else is under stress, which is exactly the moment you need at least one layer that doesn’t move.

Private credit, direct lending, note agreements, structured private arrangements, can produce meaningfully higher yields than public bonds at the cost of liquidity. This category belongs in a portfolio where liquidity needs are already covered by other instruments.

Whole Life Insurance Cash Value

This is the category most cash flow asset lists omit entirely, or dismiss as low-yield without understanding the mechanism. That framing misses what whole life actually does in a structured system.

Cash value in a properly designed whole life insurance policy grows on a guaranteed, tax-deferred basis. It does not go backward in a market correction. It accumulates consistently and compounds without interruption.

The income it produces is not a distribution in the traditional sense, it is accessible through policy loans, which are not taxable events. You borrow against the cash value; the full cash value continues compounding as if the loan does not exist.

That uninterrupted compounding during loan periods is the mechanism that separates whole life from every other instrument in this comparison. You are not sacrificing growth to access capital. The asset performs both functions simultaneously.

For legacy-stage planning, the additional dimension is the death benefit: it transfers to heirs income-tax-free, which no other cash flow asset in this list does on its own terms.

Whole life is not the highest-yield instrument in the table. It is the most structurally versatile, which is why it belongs in a coordinated system even when higher-yield assets are available elsewhere.

For a deeper look at how this works as a generational mechanism, the history of America’s great banking families offers a useful lens.

Business Income Streams (Equity Distributions, Royalties, Licensing)

For the Sovereign CEO reading this, equity distributions from owned or co-owned businesses may be the largest cash flow position in the portfolio, and the most overlooked in structural terms, precisely because it does not feel like a separate asset class.

Royalty streams, from intellectual property, mineral rights, licensing arrangements belong here as well. So does any recurring income from a business interest that does not require your active participation to sustain.

The critical distinction: business income is a cash flow asset when the income is structural, meaning it continues without your continued operational involvement. Income that depends on your active role is labor income with a business attached. Both are valuable. They are not the same thing.

Private Equity and Alternative Income Vehicles

Private real estate funds, interval funds, and syndications offer yield potential that public markets do not typically reach. The tradeoffs are real: illiquidity, accredited investor thresholds, lock-up periods, and higher minimum commitments.

The role of this category in a structured portfolio is yield enhancement, not a foundation layer. You deploy capital here after the liquidity, stability, and baseline cash flow roles are already filled by other instruments.

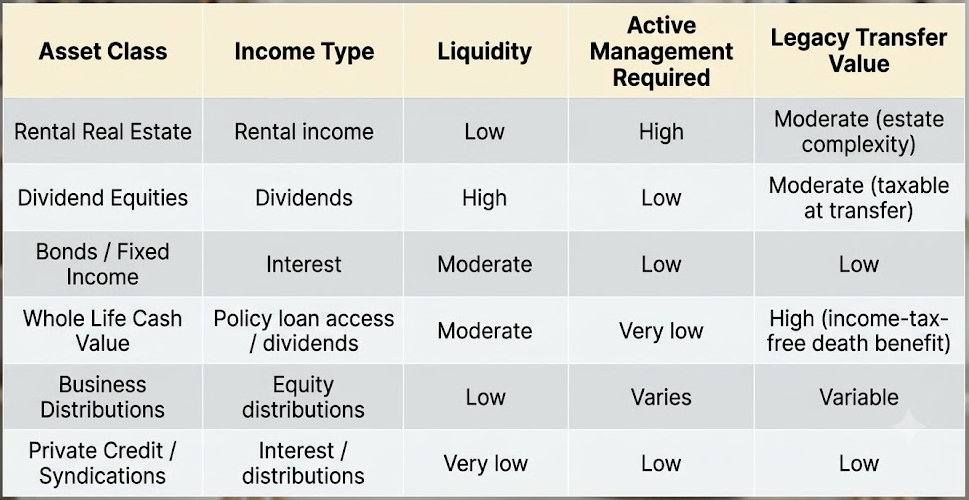

Cash Flow Asset Classes at a Glance

This table is a decision framework, not a ranking. The right mix depends on your current structure, your income needs, and the roles that are already filled, not an abstract score.

The Structural Error Most High Earners Make

The most common error in high-net-worth portfolios is not owning the wrong assets. It is owning the right assets without a coordinated structure.

Positions accumulated tactically over years, a rental property here, a dividend allocation there, a business stake somewhere else, can produce headline yields that look reasonable on paper while delivering actual after-tax, after-fee, after-friction cash flow that falls significantly short. The math looks fine until you run it all the way through.

The second common error is treating appreciation assets as if they were cash flow assets. Equity in a business that has not distributed in three years is not generating cash flow, but generating deferred optionality.

Real estate that has appreciated 40% but nets negative cash flow after mortgage and expenses is not a cash flow asset. These are legitimate positions with real value. Counting them as cash flow understates the structural gap.

The alternative is not a more complex portfolio. It is a portfolio with role clarity. In a properly structured cash flow system, each position has an assigned function: liquidity reserve, income floor, yield enhancement, legacy transfer. Those roles do not overlap by accident, they are designed to coordinate.

When one position is stressed, the others hold. When the business has a bad quarter, the policy loan is available. When the market corrects, the fixed income layer doesn’t move. When a major tenant vacates, the reserve covers the gap without forcing a sale. That is what a system does. A diversified portfolio does not automatically do this.

Want to see how your current assets are actually performing on the cash flow dimension?

The WealthScore assessment measures your portfolio across all four financial dimensions, including how your cash flow assets are structured relative to your income needs and legacy goals.

How to Build a Cash Flow Asset Portfolio That Works as a System

Step 1: Assign roles before selecting assets

Do not start with “which assets should I own.” Start with “what does this layer of my financial architecture need to do?”

Liquidity reserve, income floor, growth-oriented income, legacy transfer, each role has a different asset profile. When you select assets before assigning roles, you get a collection. When you assign roles first, you get a system.

Step 2: Build the liquidity layer first

A cash flow portfolio held without a funded liquidity reserve is exposed. One disruption, a business revenue dip, a market correction, a major unexpected expense, forces liquidation at the wrong time and at prices you do not choose. The reserve is not a cash flow asset; it is what protects your cash flow assets.

For business owners specifically, the conventional “three to six months of expenses” guidance was designed for W-2 households with predictable income. It was not designed for anyone operating at genuine financial complexity.

A reserve sized for personal disruptions only will be inadequate precisely when your business income is also under pressure, which is when you need both at once.

A whole life policy structured for cash value access serves the liquidity function while continuing to compound, making it one of the few instruments that performs the reserve role without the drag of holding idle capital in a low-yield account.

Step 3: Coordinate tax treatment across income streams

Dividend income, rental income, interest income, and policy loan access each carry different tax profiles. The goal is not aggressive tax minimization, it is not paying more than necessary on income from assets you have already structured and funded. This coordination is not optional at significant scale; the friction compounds over decades.

Step 4: Review distribution mechanics against actual needs

Yield on paper and cash flow in hand are different numbers. After expenses, taxes, and fees, what does each position actually distribute? And does that number match what your household or business actually needs from the cash flow layer?

This is where most portfolios reveal structural gaps: the headline allocation to “income-producing assets” is adequate; the actual after-friction income falls short. That gap requires either restructuring existing positions or adding capacity, and you cannot address it until you have measured it accurately.

Step 5: Stress-test the structure

What happens to your cash flow if one position is disrupted? If a major tenant vacates, a dividend is cut, a business distribution is suspended for a quarter?

A resilient cash flow system does not depend on any single position performing. That is not diversification as a general principle — it is engineering for continuity under specific disruption scenarios.

Run the scenario. Identify the single point of failure. Address it before the disruption arrives.

A Note on Whole Life Insurance as a Cash Flow Asset

The omission of whole life insurance from most cash flow asset discussions reflects a misunderstanding of what it does, not a considered judgment about its performance.

In a properly structured whole life policy, designed for cash value optimization, not maximum death benefit, the cash value grows guaranteed and tax-deferred, accessible through policy loans that are not taxable events, while the full cash value continues compounding as if the loan balance does not exist.

That combination does not exist elsewhere in the asset class comparison above. The result is an instrument that performs two load-bearing functions simultaneously: it holds the reserve and it generates the return. You are not choosing between liquidity and growth. The structure provides both.

For legacy-stage wealth builders, the third dimension is the death benefit: it passes to heirs income-tax-free, without the probate complexity of real estate or the tax exposure of a large brokerage account. The asset transfers cleanly.

None of this means whole life replaces other cash flow assets. It means it fills roles in a coordinated system that no other single instrument fills, which is why the families who have built multi-generational wealth consistently included it in their architecture, not as a product purchase but as structural infrastructure.

The Foundation Question

The right question is not “which cash flow assets should I own.” It is “do the assets I already own form a system that will hold up?”

Most high earners who take an honest look at that question find that the answer is “partially.” Good positions. Incomplete coordination. Roles that are implied but not assigned. A liquidity layer that is thinner than the income complexity actually requires.

That gap is addressable. But it requires measuring it accurately first.

If you’re already working with us, complete your WealthScore on the Client Portal: It measures all four financial dimensions, including your cash flow structure, and shows you exactly where the gaps are and in what order they need to be addressed.

Then schedule a strategy session with your Paradigm Life Wealth Strategist to turn the results into a concrete action plan, starting with the layer that needs attention first.

However, if you’re not currently working with an advisor, and would like to know where you stand, you can take this quiz to measure all four financial dimensions and then book a quick 15-minute strategy session with one of our Wealth Strategists.