The estate attorney did everything right. The trust documents were clean, the beneficiary designations were updated, the asset titling was correct.

Then the business owner died, and within eighteen months the family was forced to sell a commercial property at a 30% discount to cover a $2.4 million estate tax bill. The trust was structurally sound. It just couldn’t execute.

This is the most common wealth transfer failure pattern, and it has almost nothing to do with legal structure. It is a liquidity failure.

The estate plan defined where assets would go. It made no provision for how the transfer would actually happen when the assets were illiquid, the tax clock was running, and the market for the property wasn’t cooperative.

The structural layer of estate planning; trusts, beneficiary designations, titling, LLCs, is widely understood and well-served by competent estate attorneys. What’s rarely discussed is the funding layer that makes that structure executable. This article is about that layer.

Why Estate Plans Fail in Execution, Not Design

A trust instrument is a set of instructions. It specifies who receives assets, under what conditions, and in what sequence.

A well-drafted trust can account for spendthrift provisions, generational skipping, conditions tied to education or employment, and asset protection from creditors. The legal architecture, in most cases, is sound.

The problem is that trust instructions assume the assets they govern are accessible at the moment of transfer. That assumption frequently doesn’t hold.

Estate liquidity failures have three primary causes:

1. Illiquid asset concentration. Business owners and real estate investors tend to hold the majority of their net worth in assets that cannot be converted quickly without a discount.

A family business may be worth $5 million on paper and require eighteen months to sell at that value. Real estate may be worth $3 million in a normal market and $2.1 million under forced-sale conditions. When an estate tax obligation falls due, and the IRS does not negotiate based on asset marketability, the math doesn’t wait.

2. Estate tax timing mismatch. Federal estate taxes are due nine months after death. State estate taxes in many jurisdictions are due within six months. These are hard deadlines against which illiquid assets offer no flexibility.

The estate that is fully invested in productive assets with no liquid reserve will convert those assets to cash under whatever conditions the market offers. The discount is the liquidity premium the estate didn’t provide for in advance.

3. Business interest valuation disputes. Family business interests trigger valuation disputes with regularity. Until the dispute is resolved, the estate may be unable to distribute those assets. Heirs who depend on the estate for cash flow during this period are exposed.

None of these are exotic failure modes. They are predictable, structurally driven, and preventable, with the right funding layer in place.

The gap most estate plans don’t address is this: the trust is the structure; someone has to provide the capital that structure assumes will be there.

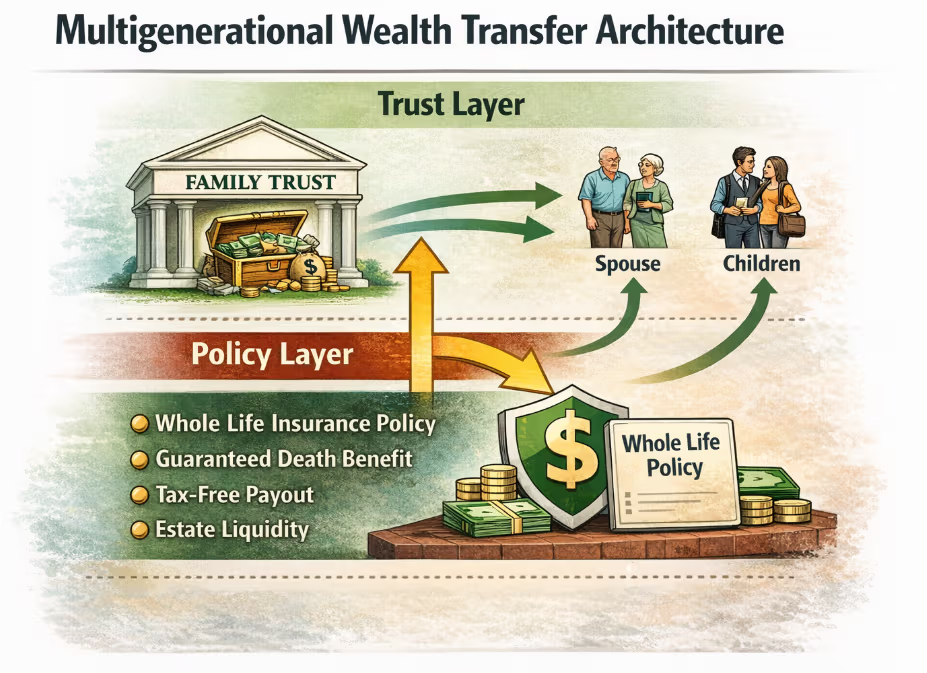

The Policy Layer: What It Does That Other Assets Cannot

A dividend-paying whole life insurance policy solves a specific structural problem that no other asset class addresses with the same precision: it delivers a contractually determined, tax-free sum at the exact moment the estate needs liquidity most.

Consider what that means against the failure modes above:

Liquidity on contractual schedule. The death benefit is not correlated to market conditions, asset marketability, or economic timing. It pays regardless of what the business is worth in the current M&A market, regardless of cap rates, regardless of whether it’s a good time to sell anything. The estate receives the capital when it needs it, not when the market happens to be cooperative.

Probate bypass. A life insurance death benefit passes directly to named beneficiaries outside the probate process. It is not subject to estate tax (when structured correctly) and is not part of the publicly visible estate. It transfers with contractual certainty, independent of the estate settlement timeline.

Predictable transfer value. Unlike equities, real estate, or business interests, the transfer value of a properly structured whole life policy is known in advance. The death benefit is set at policy design, not determined by what the market offers the week after death.

For a Legacy Architect building a multigenerational wealth transfer plan, that predictability is load-bearing; it’s the one asset in the estate that doesn’t require a valuation negotiation.

The policy doesn’t replace the trust. It funds it. The trust provides the instructions; the policy provides the capital those instructions assume will be available.

There is a second function that matters for Legacy Architects specifically: the policy’s cash value layer provides controlled access before death. A well-designed policy accumulates cash value that the owner can access, through policy loans, without triggering a taxable event.

This capacity can seed trust contributions during the owner’s lifetime, fund a family limited partnership, or serve as a liquidity reserve when other capital is deployed into less liquid investments.

The same instrument that backstops the estate at death provides working capital during the owner’s productive years.

Structuring the Policy Layer: Ownership and Beneficiary Architecture

How the policy is owned and who the beneficiaries are matter as much as the death benefit amount. The structural decisions made at policy design determine whether the death benefit stays outside the taxable estate, how it interacts with the trust, and what flexibility heirs have in deployment.

Three common structures for Legacy Architect profiles:

Irrevocable Life Insurance Trust (ILIT). The trust owns the policy rather than the individual. At death, the death benefit pays into the trust rather than directly to the estate, keeping it outside the taxable estate and shielding it from estate tax.

The ILIT trustee distributes proceeds according to the trust’s instructions; typically to fund the estate tax obligation, provide liquidity to the primary trust, or distribute outright to named beneficiaries.

The ILIT requires advance planning: the trust must be established and the policy transferred or purchased by the trust before death, and Crummey notices must be properly administered.

Spousal continuation structure. For Legacy Architects in their accumulation phase whose primary transfer concern is a generation away, second-to-die (survivorship) policies are an efficient structure.

The policy insures both spouses and pays the death benefit upon the second death, when the estate tax obligation typically crystallizes for the surviving spouse’s estate.

Premium costs are substantially lower than individual coverage at equivalent death benefit levels, making this an efficient funding mechanism for estates where the spouse is expected to inherit the bulk of assets at the first death.

Split-dollar arrangements. In business-owner contexts where the business has an ongoing interest in the owner’s continued productivity, split-dollar arrangements allow the business to participate in premium funding.

The business’s interest is typically the return of premiums paid; the business owner’s estate receives the excess death benefit.

These require careful legal documentation and compliance with specific IRS regulations, but for business owners whose personal liquidity is constrained, they allow the business to share in funding a liquidity reserve the estate will need at the owner’s death.

The common thread: these are architecture decisions made in coordination with the estate attorney, not products selected in isolation. A policy owned incorrectly, by the insured rather than by a trust or another entity, can produce a result opposite to the intended one, pulling the entire death benefit into the taxable estate.

The policy design is the mechanism; the legal structure is the housing. Both require professional design.

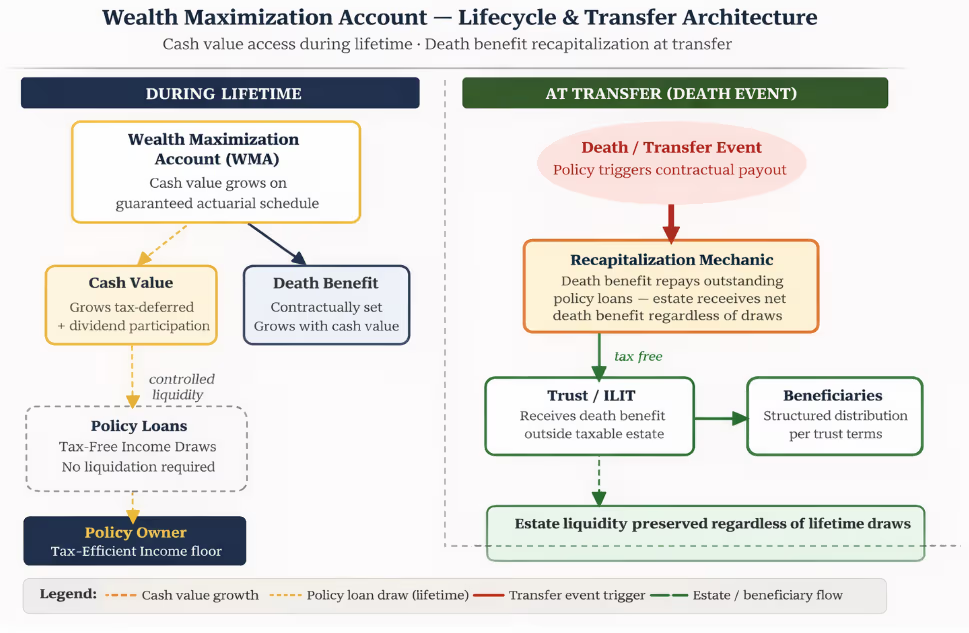

The Wealth Maximization Account in a Transfer Architecture

Paradigm’s implementation of the policy layer is the Wealth Maximization Account; a dividend-paying whole life policy designed specifically to serve multiple functions across the household financial system simultaneously.

A standard whole life policy is structured to minimize premium relative to death benefit. The Wealth Maximization Account inverts that tradeoff. It is structured to maximize cash value accumulation, using paid-up additions riders and careful premium allocation, while preserving the death benefit that serves the transfer function.

The result is a policy that builds usable liquidity during the owner’s productive years while maintaining the capital that executes the estate plan at death.

For a Legacy Architect, the architecture works like this:

The owner builds cash value in the Wealth Maximization Account over time. That cash value can be accessed, through policy loans, without triggering income tax, without disturbing the death benefit, and without a taxable distribution event.

Capital accessed this way can be deployed into other investments, business opportunities, or estate planning structures (like seeding a family limited partnership or funding an ILIT’s ongoing gifting). The policy continues to compound. The death benefit continues to grow.

At death, the death benefit recapitalizes the estate. What was accessed during the owner’s lifetime, deployed productively elsewhere, is replaced by the death benefit. The estate receives the designed transfer amount regardless of what the owner used during their lifetime.

This is the feedback loop that makes the Wealth Maximization Account structurally different from other liquidity tools: it doesn’t deplete the transfer function when used; it maintains both functions simultaneously.

This is also where the Wealth Maximization Account differs from a conventional accumulation strategy. A household that builds wealth primarily in market-correlated assets faces a simple tradeoff: spend the asset or transfer it.

The Wealth Maximization Account is not subject to that tradeoff in the same way. It can serve as a working capital reserve and a transfer mechanism, not as a compromise between the two, but as an instrument designed to do both.

No policy structure eliminates the need for competent professional design. A poorly structured whole life policy, over-illustrated, front-loaded, or designed without regard for premium sustainability, will underperform and may lapse.

The Wealth Maximization Account is a specifically designed instrument; the design is the variable that determines whether it delivers.

The Conversation Most Legacy Architects Haven’t Had

Most Legacy Architects working with financial advisors, estate attorneys, and CPAs are well-served on the structural side of estate planning. The documentation is often excellent. The planning, on the trust and legal side, is frequently thorough.

What doesn’t happen reliably is the cross-disciplinary conversation about the funding layer.

- Estate attorneys design trust structures and don’t typically model the liquidity requirements those structures assume.

- Financial advisors manage investment portfolios and don’t typically analyze what the estate will owe at death and when.

- CPAs focus on tax efficiency during the owner’s lifetime and may not model the estate tax scenario in detail until the estate is too close to transfer for efficient planning.

The result is a structurally complete estate plan with a missing execution mechanism. The trust is prepared. The liquidity is not.

The question worth asking now: Does my current estate plan account for where the liquidity comes from at the moment of transfer? Not “do I have life insurance” that’s a different question.

The relevant question is whether the death benefit, structured correctly and sized to the estate’s projected tax obligation and liquidity need, is in place as a designed component of the estate plan, not as an afterthought.

If the answer is no, or uncertain, that’s not a failure. It’s an extremely common gap that most advisors don’t surface proactively, because closing it requires coordination across disciplines that don’t typically talk to each other.

A Legacy Planning conversation at Paradigm addresses exactly this cross-disciplinary gap, not as a product consultation, but as an architectural review that examines the estate’s structure, projects the liquidity requirement, and identifies where the funding mechanism either exists, needs to be structured, or needs to be rebuilt.

Schedule a Legacy Planning Call

A Well-Designed Architecture Needs Both Layers

The trust provides the instructions for how wealth transfers. The policy layer provides the certainty that those instructions can execute. A trust without the funding mechanism is an architecture with a structural dependency it can’t fulfill. A policy without the estate planning structure is liquidity without direction.

The Legacy Architects who build durable multigenerational wealth don’t pick one. They design both; coordinated, sized to the actual liability, and reviewed by advisors who understand how the two layers interact.

If you’ve invested in building the structural layer and haven’t examined the funding mechanism with the same rigor, that’s where the review starts.