It is one of the most common questions a Paradigm Life Wealth Strategist hears from business owners.

Not: how do I grow my capital faster? Not: what should I be investing in?

But, when can I get the money out without a taxable event?

The question surfaces in strategy sessions, in follow-up calls, in the margins of financial plan reviews.

And it surfaces for a specific reason: most high-earning business owners have built a capital position that looks correct on paper and creates a practical problem in use: The capital is there. Yet, every path to it has a cost.

The 401(k) or IRA distribution is taxable as ordinary income at the highest applicable rate in whatever year the withdrawal occurs. In a high-revenue year, that means a marginal rate of 37% federally before state tax is calculated.

Early withdrawal before 59½ adds a 10% penalty on top. The tax code did not design this as a capital access vehicle, but as a deferral vehicle. The access is incidental, expensive, and penalized.

The brokerage account is more flexible. But selling a position in a high-income year triggers a capital gains event.

Long-term rates range from 15% to 23.8% federally, plus state tax in most jurisdictions, plus the net investment income tax for high earners. In California or New York, the combined marginal rate on a brokerage liquidation can exceed 35%.

And the compounding on that position ends permanently at the moment of sale. The capital you accessed stops growing. Reentry requires a timing decision made under different market conditions.

Real estate is the third common position. The capital is real, the equity is real, and the timeline to access it is measured in weeks for a cash-out refinance or months for a sale. Neither works when the capital need has a 30-day window.

The result: a business owner with $2M in net worth and $80,000 in genuinely accessible capital. Not because the capital does not exist. Because every path to it was built around a different objective than access.

This is a capital access architecture problem. And like any architecture problem, it has a structural solution, not a strategy layered on top of the wrong design, but a design that resolves the problem at the foundation.

The Architecture That Eliminates the Taxable Event Category

Here is the structural insight at the center of this article: a policy loan against whole life insurance cash value does not produce a taxable event, not because of a tax strategy, but because of what it is structurally.

A policy loan is debt, not a distribution. You are borrowing against the cash value in your policy, which serves as collateral held by the insurance company.

There is no withdrawal. There is no redemption. There is no triggering of a distribution event under the tax code. The loan proceeds are not income, they are borrowed capital, and borrowed capital is not taxable regardless of the amount or the year in which you access it.

This is a structural property of the instrument, not a loophole or a planning strategy. The same principle governs a mortgage, a business line of credit, a margin loan. The proceeds of debt are not taxable income. The policy loan is no different, except for what happens to the underlying capital while the loan is outstanding.

This is the second structural property, and it is the one that distinguishes the policy loan from every other debt-based access mechanism available to business owners.

When you take a policy loan, the full cash value in your policy continues to credit guaranteed growth and dividends exactly as if the loan does not exist.

The insurance company credits the full balance, not the net balance after subtracting the outstanding loan. The compounding continues on the total cash value during the entire loan period.

This is not true of a margin loan. A margin loan borrows against the portfolio and exposes the full position to market risk during the loan period, including the margin call mechanism that can force liquidation at precisely the wrong moment.

The portfolio does not compound through the loan; it continues to fluctuate, and the loan can be called when market conditions are worst.

This is not true of a HELOC. A home equity line of credit accesses equity in real estate, but the credit line is subject to bank approval, can be reduced or called by the lender, and does not produce compounding in the underlying asset during the draw period.

The policy loan is unique: it accesses capital through debt (no taxable event), while the underlying collateral continues to grow uninterrupted (compounding continues).

The capital is in use and still growing simultaneously. No other standard capital access mechanism produces both properties at the same time.

A note on individual circumstances: tax treatment of policy loans depends on how the policy is structured and used. Distributions and surrenders are treated differently from loans; modified endowment contracts (MECs) are subject to different rules.

The tax treatment described here applies to properly structured whole life policies that have not been classified as MECs.

A Wealth Strategist can review your specific policy design and tax situation. Additionally, outstanding policy loans reduce the death benefit and cash value available to beneficiaries, this is a material factor in policy design and should be accounted for in the overall architecture.

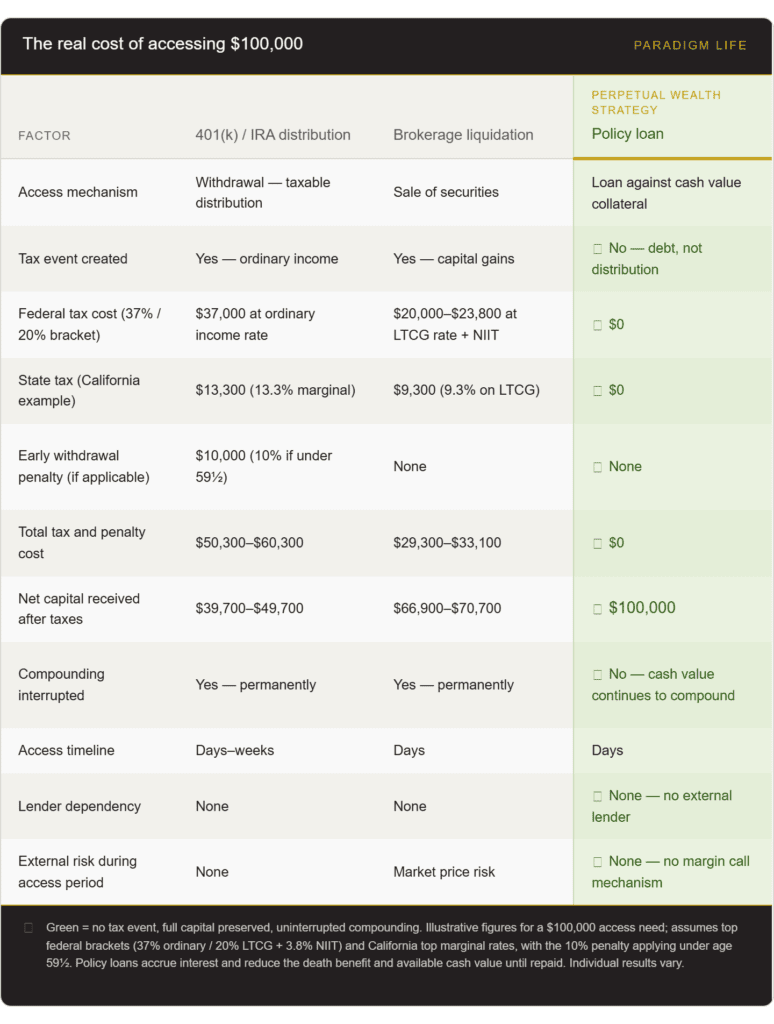

The Three Access Paths Compared: A $100,000 Capital Need

The following comparison models a $100,000 capital need for a Sovereign CEO with a net worth of $1.5M — $400,000 in a traditional 401(k), $600,000 in a taxable brokerage account, $300,000 in whole life cash value, and $200,000 in real estate equity.

Business revenue is strong; individual income is in the 37% federal bracket. The capital need has a 30-day window.

The after-tax capital comparison is the headline figure: a $100,000 capital need costs the 401(k) holder between $50,000 and $60,000 in tax and penalty to net $40,000–$50,000.

The same need costs the brokerage holder $29,000–$33,000 in tax to net $67,000–$71,000.

The policy loan holder receives $100,000, pays no tax, and continues compounding on the full cash value during the loan period.

The policy loan does accrue interest; this is the actual cost of access. For a properly structured whole life policy from a participating mutual company, the net economic cost of the loan (interest rate minus dividend credited to the full cash value during the loan period) is typically a fraction of the tax cost comparison above.

The access is not free; it is significantly less expensive, and it does not create a taxable event.

*Figures are illustrative and based on 2025 federal tax brackets and California state rates. Individual tax situations vary. Consult a qualified tax advisor for your specific circumstances.

Capital Velocity: Why Access Architecture Is a Compounding Advantage

There is a second-order effect in the policy loan structure that the comparison table above does not capture: what happens to the capital that was not paid in taxes.

A business owner who accesses $100,000 via a 401(k) distribution in a high-income year nets roughly $40,000–$50,000 after tax. The other $50,000–$60,000 went to federal and state taxes. That capital does not compound. It does not return. It is permanently removed from the wealth-building architecture.

A business owner who accesses $100,000 via a policy loan nets $100,000 and pays a fraction of that figure in loan interest, the remaining capital stays deployed, continues compounding, and returns to the architecture when the loan is repaid.

At scale, and over time, this difference is not marginal.

DALBAR’s annual Quantitative Analysis of Investor Behavior research consistently measures the behavior gap; the return investors actually receive versus the return their investments generate, at approximately 6% annually, driven primarily by forced or reactive liquidation decisions.

When capital access requires a taxable event, the architecture creates pressure to liquidate at the wrong moment. When capital access is structurally non-taxable and does not interrupt compounding, that pressure disappears. The architecture does the behavioral work.

Berkshire Hathaway arrived at the same structural conclusion independently.

Warren Buffett maintains approximately 30% of Berkshire’s assets in cash and short-term treasury instruments; not because higher-yield positions are unavailable, but because the reserve infrastructure enables deployment into asymmetric opportunities without requiring distress selling in correlated assets.

The institutional capital management framework is identical to the PWS Tier 1 thesis: the reserve is not a drag on returns. It is the mechanism that makes the rest of the portfolio operate offensively.

The business owner who has built a functioning Tier 1 layer; whole life cash value sized to the actual disruption scenarios and capital needs their situation generates, has a structural advantage in every deployment decision.

The opportunity that requires capital in 30 days does not require selling a position. The bad revenue quarter does not require a taxable distribution. The acquisition, the bridge, the strategic hire; each one can be funded from the non-taxable path while the underlying capital continues to compound.

Capital velocity is not just how fast capital grows in a single position. It is how efficiently the total architecture puts capital to work and keeps it working, including during the periods when it needs to be accessed.

A high-yield position that gets liquidated in a disruption scenario does not outperform a lower-stated-yield position that stays deployed and continues compounding while a tax-free loan funds the need.

The design decision at the Tier 1 foundation is not a conservative choice. It is the decision that makes every other position in the architecture perform at its full potential.

Know Your Capital Access Number

The most useful thing a business owner can do with the framework in this article is not to evaluate it in the abstract, but to run the numbers for their specific situation.

What is your actual accessible capital across each of the three paths?

What does each path cost in the year you are most likely to need it; a high-revenue year, a market dislocation, a moment when the disruption and the opportunity arrive simultaneously?

What is the gap between your current accessible capital and what your actual disruption scenarios require?

WealthScore maps your financial architecture across these four dimensions: Certainty, Cash Flow, Tax, Legacy, and shows you specifically where your capital is accessible, where it is locked, and what the design decision is that closes the gap.

It takes less than 10 minutes and produces a specific output: not a generic financial health score, but a real picture of your architecture against your actual disruption exposure.

The business owner who knows their accessible capital number before the moment arrives makes a different quality of decision than the one who discovers it under pressure.

Complete Your WealthScore Assessment

Free. Built for business owners. Your numbers, your architecture.