When it comes to your money, you face two economic risks: Either you’ll outlive your money, or your family will be faced with unexpected bills if you don’t live long enough. Add market volatility to the mix and it’s no wonder people are so often stressed and worried about their finances. With life insurance products, you can hedge economic risk for both scenarios. Here’s how:

Income for Life

We all want to live long and healthy lives, but what happens if you outlive your retirement funds? An annuity is a life insurance product that guarantees an income for as long as you live, so you never have to worry about outliving your wealth. It hedges the economic risk of life expectancy.

There are various types of annuities. At Paradigm Life, we like fixed indexed annuities because you get to keep all of your investment gains without any risk of loss. Fixed indexed annuities are especially beneficial for people whose retirement portfolios were severely impacted by COVID-19 and its effect on the market. Fixed indexed annuities are not actually invested in the market, but they offer options to link your interest earnings to market upswings. Therefore, you get the benefit of market performance without the loss exposure that typical market investments have.

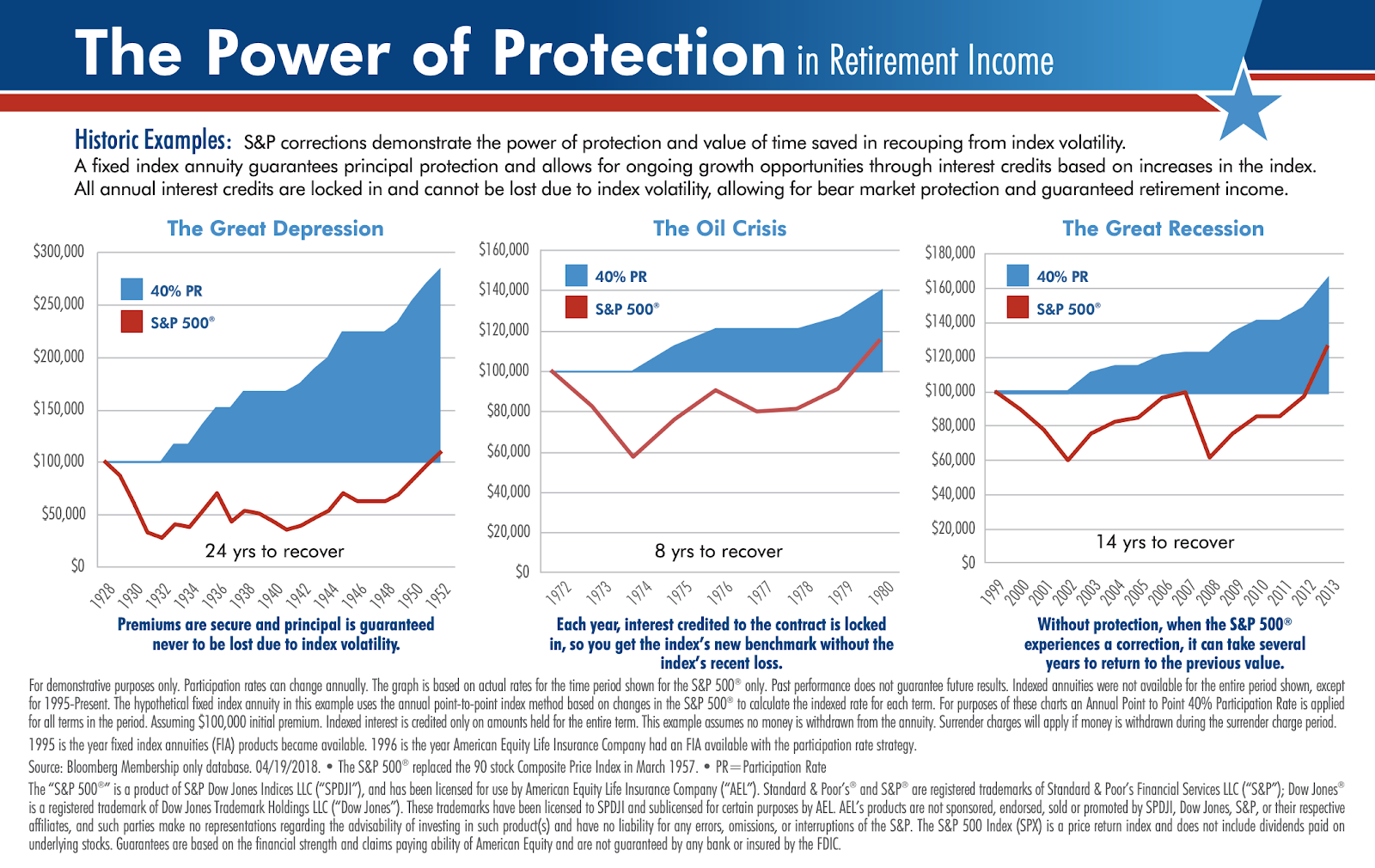

An annuity is a better option than waiting for a market upswing to increase the balance of your current market-based retirement portfolio. These graphs illustrate how an annuity can help your retirement income recover faster with greater returns:

Human Life Value

The most widely known benefit of life insurance is the death benefit. The insurance company will pay your beneficiary a lump sum in the event of your passing. With term life insurance, this benefit safeguards your loved ones in the event of your untimely death within a specified time period. With whole life insurance, your loved ones are provided for no matter when you pass away. Whole life insurance hedges economic risk of mortality.

Life insurance might not seem like an obvious choice when it comes to assets and investment vehicles, but the mutual life insurance companies we work with, like Penn Mutual, MassMutual, Guardian, and New York Life, have been profitable for over 200 years. And they don’t just pay out death benefits to beneficiaries, they also pay out dividends to policyholders and offer other living benefits like tax advantages and policy loans.

When you hedge for economic risk with a balance of insurance products like whole life and annuities, you protect against both unknowns: living too long and dying too soon. Either way, you (and your family) benefit. You benefit from an annuity if you survive longer than your 401(k) or IRA. Your beneficiaries benefit as survivors from your whole life insurance policies. You can successfully navigate both risks!

How Insurance Companies Hedge Economic Risk

So what makes insurance companies so reliable, especially in difficult financial times? How are they able to pay dividends and death benefits consistently for over 200 years? The answer: Mutual life insurance companies also hedge their economic risk.

In order to grow wealth, mutual insurance companies reduce volatility by diversifying their portfolios. In addition to stocks and bonds, they diversify with a variety of insurance products. For example, Penn Mutual’s insurance offerings are a balance of various annuity products and different types of life insurance products. By maintaining this balance, Penn Mutual has sufficient funds from purchased annuities to pay out death benefits on life insurance claims, and sufficient premium payments on life insurance to pay annuity incomes.

Whole life insurance isn’t the only life insurance product our carriers offer. Because they also carry policies for term life insurance and a variety of universal life insurance, they increase the diversification of their portfolio, which mitigates risk and volatility and increases profitability. Universal and term insurance policies don’t pay out death benefits to the degree of whole life, which means mutual insurance companies receive millions of dollars in premium payments for these types of insurance while paying out very little to their respective policyholders and their beneficiaries. The remainder is profit for the insurance company, which translates to profit for whole life insurance policyholders. As a whole life insurance policy owner, you reap the benefits in the form of dividends and interest.

WATCH: Hedging Dual Economic Risk

Conclusion

Take a note from mutual life insurance companies, which have weathered crises like the Spanish Flu, WWI, WWII, the Great Depression, the Great Recession, and now COVID-19. Hedge your economic risk with a balanced portfolio that includes whole life insurance, plus annuities if you’re 55+, and enjoy the peace of mind felt when you’re not exposed to market volatility.

At Paradigm Life we can customize a policy to fit your financial situation. Our expert Wealth Strategists are available to answer your questions and show you customized illustrations, outlining an individual plan of action to help you achieve your goals.  , no strings attached.

, no strings attached.