Generational wealth refers to financial assets passed down from one generation to the next, think real estate, investments, businesses, and strategic financial tools like whole life insurance. But it’s not just about money. It’s about values, education, and a mindset that shapes how families grow, preserve, and use their wealth over time.

We believe generational wealth is the foundation for lasting impact—not just in your family, but in your community and legacy. This guide will show you how to build generational wealth with intention, control, and clarity.

What Is Generational Wealth?

Generational wealth refers to assets—such as real estate, investments, businesses, or strategically designed financial tools like whole life insurance—that are passed down from one generation to the next. But at Paradigm Life, we define it more broadly: it’s not just about passing on money. It’s about transferring financial capability, opportunity, and mindset.

Generational wealth includes:

- Tangible assets: homes, businesses, savings, retirement accounts, and cash value life insurance

- Financial systems: trusts, family banks, estate plans, and structured ownership

- Intangible legacy: financial literacy, values, and decision-making frameworks that shape how future generations manage money

When properly structured, generational wealth becomes self-sustaining—growing, adapting, and supporting each generation without eroding the core.

Why It’s Different from Ordinary Wealth

Most people accumulate assets for personal retirement or lifestyle. But generational wealth is designed to outlive the wealth creator. It’s structured to:

- Preserve value over time

- Transfer efficiently through tax-smart planning

- Empower heirs with purpose and knowledge, not entitlement

- Support both freedom and responsibility

In essence, generational wealth is legacy in action, your opportunity to influence lives beyond your lifetime.

Why Generational Wealth Matters

Generational wealth isn’t just about accumulating money, it’s about creating lasting financial freedom, opportunity, and stability for the people you care about most. When built intentionally, it becomes a legacy that grows, protects, and empowers each generation.

Stability Across Generations

True wealth preservation provides more than financial comfort—it offers resilience in uncertain times and a foundation for future growth.

- Offers long-term financial security through strategic planning and protected assets

- Shields your family from economic downturns or market volatility

- Provides access to capital for education, launching a business, or investing in opportunities

- Creates a buffer that allows future generations to make decisions from a place of strength, not scarcity

Legacy Wealth with Purpose

Generational wealth shapes your family’s narrative. It allows you to leave behind more than dollars—it gives you the ability to pass down values, vision, and intentionality.

- Helps define your family’s financial story and long-term mission

- Empowers you to influence the next generation’s values, even after you’re gone

- Supports philanthropic goals, community impact, or long-term family culture

- Allows for multi-generational stewardship rather than one-time inheritance

Breaking the Cycle

For many families, creating generational wealth is about changing the future—ending financial instability and building a new standard of independence and education.

- Equips the next generation with critical financial literacy and decision-making tools

- Reduces dependency on government aid or reactive financial behavior

- Contributes to reducing the income inequality gap through strategic knowledge transfer and long-term planning

Developing a Generational Wealth Mindset

Before you start building generational wealth, it’s critical to lay the right foundation—not just financially, but mentally. A generational wealth mindset is the belief that wealth is not just for you, but for those who come after you. It means thinking in decades, not days. Planning for your children’s children. And using money as a tool for freedom, not just consumption.

1. Think in Generations, Not Just Goals

The average person plans for retirement. A generational thinker plans for multi-generational impact. This long-term perspective affects how you:

- Save – with the intention of sustainability over urgency

- Invest – in assets like real estate, life insurance, and business that grow and last

- Protect – by avoiding short-term risks that could jeopardize the family future

Ask Yourself:

- Are my financial decisions designed to serve my heirs, not just myself?

- Do I view wealth as a one-time event, or a system that must endure?

2. Shift from Ownership to Stewardship

One of the most powerful mindset shifts is to stop thinking like an owner—and start thinking like a steward. That means your money doesn’t just belong to you. It belongs to your family’s legacy.

Stewardship thinking leads to:

- Protecting assets through estate preservation tools (trusts, insurance, asset protection)

- Making decisions based on impact and values, not just ROI

- Preparing your heirs to receive—not just inherit—wealth

3. Make Financial Education a Family Value

The biggest threat to generational wealth isn’t taxes or market crashes—it’s a lack of financial literacy. If your heirs don’t understand how wealth works, it will disappear.

Start early with financial education for children. This includes:

- Basic money concepts: saving, investing, compound interest

- How your wealth is structured: explain your business, investments, and life insurance strategy

- Involving them in financial discussions—family budget meetings, legacy talks, or philanthropic planning

We help families adopt the Generational Wealth Mindset by showing them how to use financial tools, like whole life insurance, private family banking, and the Perpetual Wealth Strategy, not just for accumulation, but for intentional transfer and education. When you adopt this mindset, you’re no longer building wealth for yourself, you’re creating a foundation that your family can build on for generations.

How to Build Generational Wealth

We believe building generational wealth is about creating a system that grows and protects your assets while also preparing your family to manage, use, and continue that wealth with purpose. It’s not just about accumulating money—it’s about designing a structure that lives beyond you. Let’s walk through the four foundational pillars of building lasting wealth:

1. Grow High-Quality, Long-Term Assets

The first step is to focus on acquiring assets that appreciate and can be transferred across generations, such as:

- Real estate that produces income and grows in value

- Businesses that can be scaled or passed down

- Dividend-paying whole life insurance with high early cash value

- Private lending or investment accounts designed for long-term growth

Unlike speculative assets or short-term gains, these tools prioritize stability, income, and control, hallmarks of the Perpetual Wealth Strategy.

We structure high-cash-value whole life insurance policies not just for protection, but as Tier-One Assets, safe, liquid, and built to last. These policies allow you to build wealth and access it during your lifetime, without interrupting long-term growth.

2. Design with Control in Mind

Most people build wealth reactively—investing wherever the market points. We encourage a proactive approach, using strategies that prioritize control over capital, such as:

- Private family banking using policy loans, so your money can work in multiple places at once

- Structured insurance design that allows for early liquidity and long-term legacy planning

- Minimizing market dependence by building a financial foundation that doesn’t rise and fall with volatility

3. Protect What You’ve Built

Asset protection and estate preservation are non-negotiable. Your wealth must be guarded from lawsuits, taxes, poor decisions, and market disruptions. This includes:

- Establishing trusts and estate plans to protect heirs and honor your wishes

- Using permanent life insurance to pass on wealth income-tax-free

- Separating personal and business assets through proper entity structuring

- Preparing for the unexpected with living benefits like disability riders or long-term care planning

4. Educate and Empower the Next Generation

Even the most carefully built legacy can collapse if the next generation isn’t prepared to receive it. Financial education, shared vision, and active involvement are the keys to lasting wealth.

- Start teaching basic money principles as early as possible

- Involve your children or grandchildren in business, investments, or giving

- Share the story and purpose behind your wealth

- Document your family’s mission, values, and expectations

By focusing on assets that last, tools that provide liquidity and control, and educating the next generation, you don’t just build wealth, you build a system that supports your family’s values and vision for decades to come.

Generational Wealth Strategies That Work

Creating generational wealth doesn’t happen by chance, it happens by strategy. At Paradigm Life, we teach clients to build systems, not just savings, using proven methods that combine financial growth, liquidity, protection, and transferability.

1. Leverage Whole Life Insurance as a Wealth Engine

Dividend-paying whole life insurance isn’t just for protection—it’s a powerful asset when properly structured. Here’s how it supports generational wealth:

- Guaranteed cash value growth with no market correlation

- Policy loans offer tax-free liquidity without triggering capital gains

- Death benefit passes income-tax free to beneficiaries

- With The Perpetual Wealth Strategy™, cash value can be used during your lifetime and still passed on, keeping your money in motion across generations

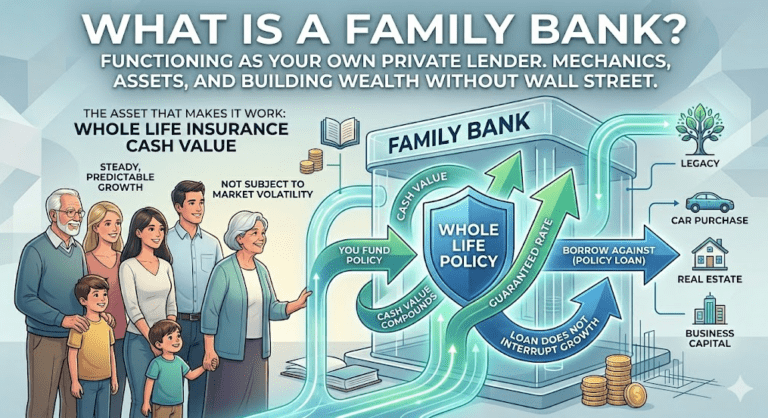

2. Use Private Family Banking to Keep Capital in Motion

Private family banking allows you to become your own source of financing. Instead of borrowing from banks, you borrow against your own life insurance policies, keeping your wealth within the family system.

Benefits include:

- Immediate access to capital

- No loan applications or credit checks

- Continued compounding of cash value—even when borrowing

- Teaches the next generation how to manage, borrow, and repay responsibly

3. Invest in Long-Term, Transferable Assets

To build generational wealth, you need assets that grow and can be passed down efficiently:

- Real estate: rental income, appreciation, tax benefits, and legacy potential

- Businesses: create a family-owned enterprise that can be scaled and inherited

- Cash-flowing investments: structured for stability and generational transfer

- Life insurance policies on multiple family members: create multi-tiered protection and growth

4. Build a Legacy Plan That Goes Beyond a Will

Wills are essential, but they’re not enough. Building generational wealth requires a comprehensive estate plan:

- Revocable or irrevocable trusts

- Tax mitigation strategies to preserve more of your estate

- Succession planning for businesses

- Letters of intent or family constitutions to pass down values, not just assets

5. Make Education Part of the Inheritance

Many wealth transfers fail because heirs aren’t prepared. Include:

- Age-appropriate financial training

- Family meetings about wealth and values

- Opportunities for hands-on involvement in family finances or philanthropy

- A clear philosophy about money’s purpose and stewardship

Real Estate: A Pillar of Generational Wealth

When it comes to building generational wealth, few assets have the track record and flexibility of real estate. From cash flow to appreciation, from leverage to tax advantages, real estate offers multi-dimensional value that makes it a cornerstone in most family wealth strategies. We often help clients structure real estate acquisitions using policy loans from whole life insurance, enabling them to access opportunity without interrupting long-term compounding or relying on bank financing.

Why Real Estate Builds Generational Wealth

- Appreciation over time: Real estate generally increases in value, especially in growing markets.

- Cash flow potential: Rental income can provide ongoing returns for multiple generations.

- Tax advantages: Depreciation, 1031 exchanges, and interest deductions make real estate a tax-efficient asset.

- Tangible inheritance: Unlike stocks or digital assets, real estate is a physical, usable, and often emotionally connected asset.

- Leverage and control: You can use debt to grow a real estate portfolio while maintaining ownership and control.

Strategies for Building Generational Wealth Through Real Estate

- Buy and Hold Residential Property

Purchase single-family or multi-unit properties in appreciating areas. Rent them out, maintain them, and pass them down. - Create a Family Real Estate Trust or LLC

Hold property in a family entity to streamline inheritance, reduce tax exposure, and create shared ownership. - Use Whole Life Policy Loans for Down Payments

Access capital from your cash value life insurance policy to fund real estate purchases—without disrupting policy growth. - Teach the Next Generation

Involve your children in managing, maintaining, and understanding your real estate assets. Show them how it creates ongoing opportunity.

How to Integrate Real Estate with The Perpetual Wealth Strategy™

- Use policy loans to fund a purchase, then repay the loan using rental income.

- Keep your policy compounding while the property appreciates and cash flows.

- Upon death, the death benefit pays off the policy loan, and the property continues as a legacy asset.

- This creates a circle of capital—a private banking model where wealth stays within your family ecosystem.

Protecting Generational Wealth

Building wealth is only half the journey. The true mark of generational wealth is its ability to endure, through tax seasons, lawsuits, life events, and generational handoffs. At Paradigm Life, we teach that unprotected wealth is vulnerable wealth, and the best way to honor your legacy is to shield what you’ve built with care and intention.

1. Establish a Comprehensive Estate Plan

A basic will isn’t enough. To truly preserve generational wealth, you need a multi-layered estate strategy that ensures your assets are transferred efficiently and according to your values.

- Revocable or irrevocable trusts to control how wealth is distributed

- Healthcare proxies and powers of attorney for emergencies

- Clear beneficiary designations on all financial accounts and policies

- Letters of intent or family governance documents to pass on values, not just assets

Many families lose wealth in probate or legal disputes simply because a full estate plan was never put in place.

2. Use Permanent Life Insurance for Tax-Free Transfers

One of the most efficient ways to pass wealth to the next generation is through whole life insurance:

- Income-tax-free death benefit to heirs

- Avoids probate when properly structured

- Can equalize inheritance among heirs (e.g., if one child inherits a business or property)

- Liquidity to cover estate taxes or other final expenses, preventing forced asset sales

3. Protect Assets with Smart Legal Structuring

Wealth without legal structure is an open target. To prevent erosion from lawsuits, divorce, or mismanagement:

- Hold assets in LLCs or trusts rather than individual names

- Separate personal and business finances

- Create buy-sell agreements for any business assets

- Consider asset protection trusts for higher-net-worth scenarios

4. Prepare Heirs to Receive Wealth Wisely

The most overlooked (and costly) threat to generational wealth? Heirs who are unprepared to manage it.

- Set expectations early: wealth comes with responsibility and stewardship

- Use family education, governance meetings, and mentoring

- Encourage earning before inheriting—build character, not just cash flow

- Define roles within the family legacy: philanthropy, business, real estate, etc.

Protection isn’t just about documents, it’s about direction. It means knowing your legacy will continue, with clarity and purpose, long after you’re gone.

FAQs: Generational Wealth

How much money is needed for generational wealth?

There’s no exact number. Even a modest estate can become generational wealth if it’s managed properly and passed on with intention. The key isn’t the size—it’s the structure:

- Strategic use of whole life insurance

- Ownership of cash-flowing assets

- Clear estate planning and education for heirs

A well-designed system beats a one-time windfall every time.

How long does generational wealth last?

Statistically, most wealth is lost by the third generation—but it doesn’t have to be. With the right planning:

- Wealth can grow instead of depleting

- Assets can be protected from taxes, lawsuits, and mismanagement

- Education and structure can extend wealth indefinitely

The key is ongoing communication, planning, and stewardship.

How does generational wealth contribute to income equality?

By transferring wealth intentionally, families can:

- Break cycles of financial insecurity

- Equip the next generation to create more income

- Fund education, businesses, or philanthropy that benefits the community

Generational wealth offers a practical solution to closing the opportunity gap—within families and across society.

Which is better: building wealth or generating income from investments?

It’s not either/or—it’s both. Wealth-building is about growing your net worth over time. Income generation gives you cash flow. The right strategy blends them:

- Real estate = appreciation + rent

- Whole life insurance = cash value growth + liquidity

- Business = equity + owner’s income

At Paradigm Life, we help clients balance both goals to support present needs and future legacy

How do I build generational wealth with life insurance?

Whole life insurance is one of the most effective tools for building and preserving generational wealth:

- Cash value grows tax-deferred and can be accessed during your lifetime

- Policy loans allow you to leverage your capital while preserving compounding

- Death benefit passes income-tax free to beneficiaries

- When structured properly, it supports wealth transfer, asset protection, and family banking

It’s not just protection, it’s a permanent financial asset.

Legacy Is a Choice

Generational wealth doesn’t happen accidentally. It’s built intentionally—through thoughtful decisions, powerful tools, and a long-term mindset that puts your family’s future first. At Paradigm Life, we believe that true wealth goes beyond dollars. It’s about freedom, control, values, and vision. Whether you’re just starting or refining an existing legacy plan, the right strategies can help you create a system that grows, protects, and empowers your family for generations to come.

If you are curious how generational wealth fits into your financial strategy, a conversation with a Paradigm Life Wealth Strategist can help you explore customized solutions built to last, because legacy isn’t something you hope for. It’s something you design. Schedule Your Strategy Session.