You have done the thinking. You have looked at the conventional financial advice model; the 401(k)-first, diversify-everything, wait-40-years playbook, and recognized that it was not designed for you.

It was designed for a median household with predictable income, a steady employer, and a 40-year runway to retirement. For that profile, the advice is adequate.

For a business owner who generates variable income, deploys capital actively, builds equity in illiquid assets, and operates on a non-linear timeline, the conventional model produces the wrong structure.

The Sovereign CEO who has rejected it is not being contrarian for the sake of it. They are being accurate. That recognition is the right starting point. It is not a financial operating system.

Thinking differently about money produces clarity about what not to build.

The financial architecture that makes that position permanent, the system that keeps capital accessible, coordinates income across tax dimensions, and absorbs disruption without dismantling what you have built, is a different kind of work. This article is about that work.

What Contrarian Financial Thinking Gets Right

The conventional financial advice model has a design constraint that rarely gets named directly: it was engineered for the median case, not the complex one.

For the W-2 employee with employer matching and a predictable expense structure, maxing the 401(k) first makes sense. Tax deferral is real, the match is free capital, and the 40-year compounding window is long enough to absorb the access restrictions. The advice fits the profile.

For the Sovereign CEO, none of those constraints hold. Income is variable, some years are exceptional, some are not. Capital needs do not arrive on a predictable schedule. The business is the primary wealth-generation engine, and it is also an illiquid asset that does not distribute on command.

The 401(k) ceiling is low relative to the income the business generates. And the access restrictions; distributions before 59½ are taxable and potentially penalized, create exactly the kind of structural brittleness a business owner can least afford.

The contrarian critique of this model is correct: the conventional path was designed for someone else’s outcome.

Liquidity is systematically undervalued in conventional advice. Ownership and cash flow compound differently than account balances. The financial system should serve the owner’s life, not constrain it at the moments that matter most.

Recognizing this is step one. It is an accurate diagnosis.

But a correct diagnosis without a treatment plan is incomplete. The Sovereign CEO who has internalized the contrarian frame knows what they are rejecting. What they often have not yet built is what replaces it.

Where the Philosophy Stops and the Operating System Begins

A philosophy tells you what to reject. It does not tell you what to build.

The gap between those two things is where most contrarian-minded business owners find themselves: clear on the conventional model’s failures, less clear on what the alternative architecture actually looks like in practice.

Not a collection of individual decisions, a better investment here, a different account structure there, but a coordinated operating system.

The exposure this gap creates is specific.

Capital deployed for growth without an accessible liquidity layer means that a disruption; a business revenue gap, a strategic opportunity with a short timeline, an unexpected obligation, arrives as a structural crisis.

The capital exists on the balance sheet. The path to it runs through a taxable liquidation, a retirement account distribution, or a real estate position that cannot close in 30 days. The contrarian CEO who built the business to operate with flexibility finds the financial architecture constraining it at the exact moment flexibility matters most.

Income sourced primarily from the business means every dollar is taxable at the highest applicable rate. There is no non-taxable access path.

In a high-revenue year, the tax exposure compounds with the income, not because of a bad strategy, but because the sourcing structure was never given an alternative mechanism.

Business equity building without a coordinated legacy transfer structure means the wealth that took a career to build transfers to heirs with income tax liability attached. The 401(k) balance, the business equity, the taxable brokerage account, each carries a tax consequence that reduces what actually arrives.

None of this is a failure of contrarian thinking. It is the natural result of having clarity about what you do not want without yet having built what you want instead.

The operating system question is not: what should I reject? It is: what does a financial architecture that actually serves the Sovereign CEO look like; and does mine have it?

The Four Dimensions a Financial Operating System Covers

A complete financial architecture addresses four distinct dimensions. Each governs a different layer of the structure. Each depends on the layers beneath it.

Certainty: The Load-Bearing Layer

The Certainty layer is the foundation. It covers the reserve and protection structure; the funded liquidity layer that allows disruptions to be absorbed without cascading into decisions elsewhere in the architecture.

When the Certainty layer is in place, a revenue gap is an inconvenience. A capital need is a policy loan. An unexpected expense does not require a conversation about which growth position to liquidate. The disruption hits the foundation and stops there.

When the Certainty layer is absent or underfunded, the disruption does not stop at the foundation. It cascades.

The brokerage account gets liquidated, triggering a capital gains event at a high-income moment. The IRA distribution gets taken, taxable as ordinary income, potentially with a penalty. The business deal that required 30-day capital access gets passed. One disruption produces four downstream decisions, each with its own compounding cost.

A weak Certainty layer does not create a liquidity problem in isolation. It creates exposure in every dimension above it simultaneously.

Cash Flow: How Capital Moves

The Cash Flow layer governs income sourcing and how capital moves through the structure.

For the Sovereign CEO, the most consequential question in this layer is not how much revenue the business generates; it is how many meaningfully different sources that capital can flow from, and whether any of them are non-taxable.

A business owner who draws exclusively from business distributions has one source, fully taxable at ordinary income rates. A business owner with a coordinated Cash Flow layer has additional access paths; policy loans that are not taxable income events, that create structural flexibility.

In a high-revenue year, living expenses or capital needs can be funded from the non-taxable path rather than adding to an already elevated distribution total. The tax outcome improves not through a transaction, but through the design of the sourcing structure.

Without this layer, every income decision is made under constraint. With it, income decisions are made by design.

Tax: Structural, Not Transactional

Most tax advice for business owners operates at the transaction level: which accounts to contribute to, when to convert, how to structure a distribution. These decisions are real and matter. They are not the whole picture.

Tax architecture at the system level coordinates something larger: how income is sourced across years, how account structures interact with each other, how access mechanisms affect taxable income in any given year.

The Sovereign CEO who has only done transaction-level tax work is operating with structural inefficiency that transaction-level decisions cannot resolve, because the inefficiency is in the design of the system, not in any individual move made within it.

A coordinated Tax dimension does not eliminate the need for transactional tax strategy. It provides the framework within which individual decisions compound into structural efficiency.

Legacy: How the Operating System Ends

The Legacy layer covers how wealth transfers and what arrives after the tax consequences of that transfer are accounted for.

The Sovereign CEO who has built substantial wealth across a business, real estate positions, and retirement accounts often has a legacy picture that looks very different before and after tax.

A $2 million traditional IRA balance is a $2 million IRA until the beneficiary runs the distribution math at their income tax rate over a 10-year distribution window. The business equity that took a career to build requires a transaction, with all of its timing and valuation complexity, to realize.

A coordinated Legacy layer includes income-tax-free transfer mechanisms scaled to the total picture: a death benefit that transfers immediately, outside of probate, with no distribution schedule and no income tax liability to the beneficiary.

The financial operating system that served the owner well during accumulation serves the family efficiently at transfer.

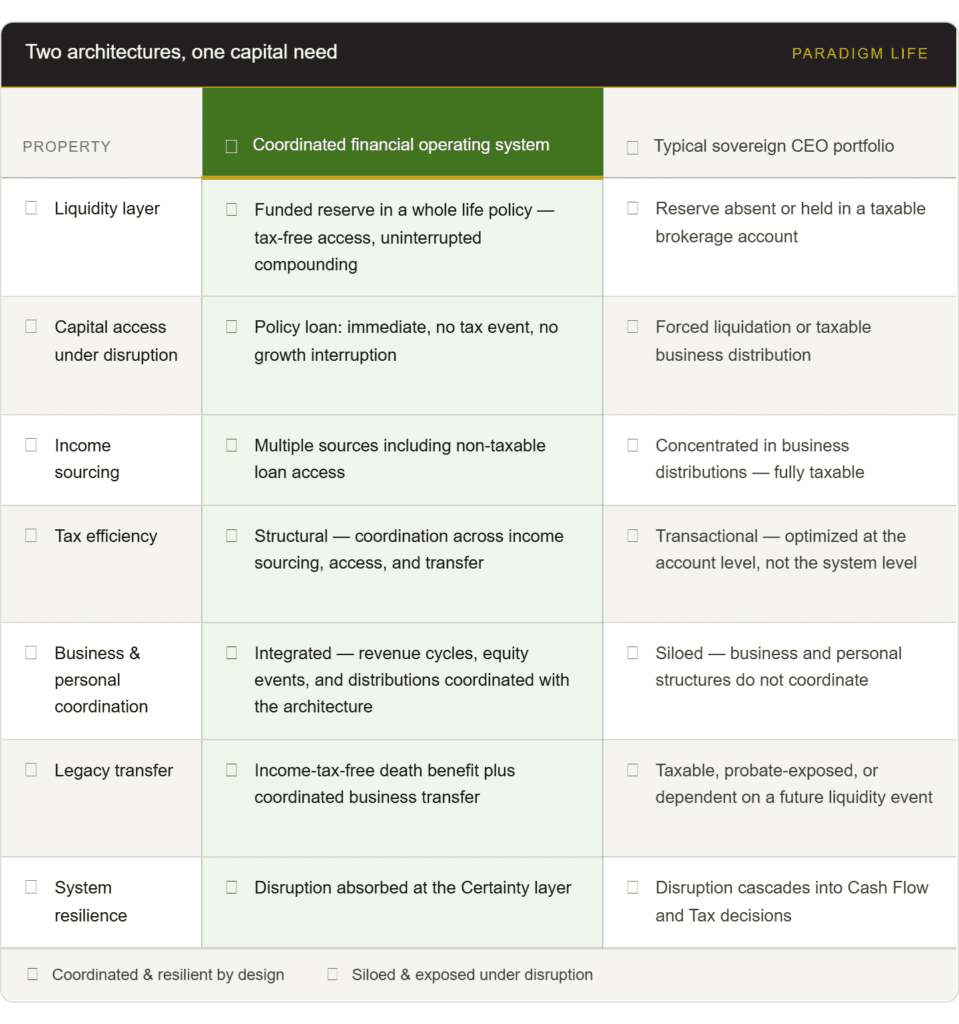

Two Architectures, One Capital Need

The distance between a coordinated financial operating system and the typical Sovereign CEO financial picture is not a matter of net worth. It is a matter of design. Here is what the same capital looks like in two different architectures.

The Sovereign CEO who recognizes their own financial picture on the right side of this table is not looking at a failure. They are looking at the natural result of building a business with a clear operating model and a financial structure that was never given the same clarity of design.

The WealthScore Assessment measures your financial architecture across all four dimensions: Certainty, Cash Flow, Tax, and Legacy, and shows you exactly where the operating system is in place and where the gaps are.

Complete Your WealthScore Assessment →

Free. No sales call required.

Building the Operating System: The Sequence That Makes Contrarian Positions Permanent

Understanding the four dimensions is not the same as having the architecture in place. The sequence in which the architecture is built matters, and the sequence that most high earners follow produces the structure on the right side of the table above.

The Foundation Comes First

The conventional financial planning sequence starts with growth: fund the retirement accounts, deploy capital into investment positions, and hold whatever remains as a reserve. The reserve is what is left over after everything else is funded.

This sequence produces an underfunded Certainty layer by design. The reserve is thin because it was built last. And a thin reserve means the first meaningful disruption to arrive does not stay at the foundation, it cascades.

The sequence that produces a coordinated operating system reverses this.

The Certainty layer is established first: a funded reserve, properly structured, in the right instrument. Growth positions are built on top of a functioning foundation, which means the compounding happens on a structure that can absorb pressure, not one that depends on the absence of it.

This is not a conservative approach. It is a load-bearing sequencing decision. The same capital, deployed in the right order, produces a fundamentally different system.

The Reserve Instrument Is Not a Trivial Decision

Where the liquidity layer lives determines three structural properties: the tax treatment when accessed, whether the underlying asset continues compounding during use, and how it interacts with the rest of the architecture. These are not interchangeable decisions dressed up as a product selection.

Whole life insurance cash value, specifically, the policy loan structure, performs all three reserve functions simultaneously.

A policy loan is not a taxable event. You are borrowing against collateral you own, not distributing an asset. There is no W-2, no 1099, no capital gains calculation regardless of the size of the draw or the timing.

The full cash value continues to credit guaranteed growth and dividends during the loan period, as if the loan does not exist, the capital is in use and it is still compounding. And the access is available on your terms: no credit committee, no approval timeline, no lender setting the conditions.

This is not the instrument the conventional financial advice model defaults to. It is also not the instrument that contrarian financial content typically introduces, because the contrarian frame is primarily concerned with identifying what to reject, not with building what replaces it.

It is the instrument that solves the accessibility problem at the structural level, without sacrificing the compounding that makes the growth positions valuable.

The Business and the Architecture Need to Coordinate

The Sovereign CEO’s business is not separate from their financial architecture. It is the primary input to it; the source of the income, the primary illiquid asset, and the structure that generates the tax exposure the personal financial architecture has to manage.

A coordinated financial operating system integrates the business structure with the personal financial architecture: revenue cycles coordinated with policy loan timing, equity events planned alongside the legacy transfer structure, distribution timing managed in coordination with the income sourcing layer.

The business decision and the financial architecture decision are the same decision, made with visibility into both structures simultaneously.

Most Sovereign CEOs have built one of those structures with deliberate precision and treated the other as a consequence. The operating system that makes the contrarian position permanent treats both as design problems, and coordinates them accordingly.

The Architecture That Makes It Permanent

The Sovereign CEO who has thought carefully about what they do not want in a financial system, who has rejected the conventional model with clear reasons and built a business that operates outside conventional constraints, is already most of the way to the right question.

The remaining question is not philosophical. It is architectural. What does the operating system that makes the contrarian position permanent actually look like? Which dimensions of your current financial structure are in place? Where are the gaps?

Those are specific questions with specific answers, and they are different for every financial picture.

The WealthScore Assessment is where the diagnostic starts: a four-dimension evaluation of your current financial architecture that shows you exactly where the operating system is functioning and where the design decisions need revisiting.

A contrarian financial position is a starting point. The financial operating system that makes it permanent is the work.

Complete Your WealthScore Assessment →

Free. Three minutes. A specific picture of where your architecture stands.

Ready to move from diagnostic to design?