For five decades, defined-benefit pensions were the dominant retirement income vehicle in the United States, not because they were simple, but because they solved a specific and technically difficult problem.

They converted a probability distribution of future income needs into a guaranteed, mortality-adjusted cash flow stream.

The actuarial science underlying a pension isn’t about predicting the future; it’s about structuring income so that longevity risk, sequence risk, and purchasing power risk are managed contractually rather than probabilistically.

You receive what the math guarantees, regardless of how the market performs in year three.

The shift to defined-contribution plans; 401(k)s, IRAs, and individual brokerage accounts, transferred that problem to the individual without transferring the tools to solve it.

The result is a retirement income ecosystem built almost entirely on portfolio drawdown models: withdrawal rates derived from historical return sequences, income floors that depend on the market cooperating in the critical early years, and longevity exposure that compounds with every year of a 40-year retirement horizon.

Anyone asking how to optimize retirement income using actuarial science is asking the right question. The answer is not to replicate the pension system, that’s what commercial annuities attempt, with significant trade-offs that matter for the Legacy Architect profile.

The answer is to identify the instrument that imports actuarial-grade income certainty mechanics into a private retirement architecture without surrendering capital flexibility, estate transfer function, or liquidity. That instrument exists. This article makes the technical case for it.

What Actuarial Science Actually Does for Retirement Income

The actuarial optimization problem in retirement income is this: maximize the present value of cash flows across a probability-weighted longevity distribution, while minimizing the variance of outcomes in any given year.

It is not a portfolio construction problem. It is an income engineering problem, and it requires different tools.

Three mechanisms define how actuarial science solves it:

Mortality credits. In any pooled longevity-risk vehicle; a defined-benefit pension, a commercial annuity, or a mutual life insurer’s participating block, individuals who die earlier than the actuarial expectation effectively fund the income of those who live longer.

This pooling mechanism allows surviving participants to receive income that exceeds what their own individual capital base could produce. It is the structural engine behind every pension fund in existence.

The individual benefits from the pool’s aggregate mortality experience, not just their own capital’s return.

Guaranteed cash flow tables. Actuarial instruments produce contractual income projections derived from mortality assumptions and guaranteed interest rates, not market-return assumptions. The income figure at age 75 is not a projection; it is a contractual obligation of the instrument’s issuer, derived from tables that have been stress-tested across multiple economic regimes.

This is categorically different from a Monte Carlo simulation, which is a probability distribution, not a guarantee.

Longevity risk transfer. The individual’s exposure to outliving their capital is transferred, either to the risk pool (in pension and annuity structures) or to the insurer’s balance sheet (in whole life policy structures). The retiree no longer manages longevity risk through portfolio math; the risk has been contractually absorbed by an entity with the balance sheet and actuarial expertise to hold it.

Most private retirement income strategies contain none of these three mechanisms. A 60/40 portfolio with a 4% withdrawal rate is a probabilistic model; it has a historically reasonable success rate across 30-year periods, but it carries sequence-of-returns risk (the order of returns matters enormously in early withdrawal years), it has no mortality credit component, and longevity risk remains entirely with the individual.

If the retirement horizon extends to 40 or 45 years, entirely realistic for someone retiring at 52, the SWR literature offers notably less confidence.

The reader who is asking about actuarial retirement income optimization already knows this gap exists. The question is which instruments close it.

Why the Annuity Comparison Matters — and Where It Breaks Down

Commercial annuities are the actuarially correct answer to the income certainty problem in isolation.

Immediate annuities, deferred income annuities, and longevity annuities all incorporate genuine mortality credit pooling, contractual income guarantees, and longevity risk transfer to the insurer.

If the sole objective were to maximize actuarially-weighted income certainty, annuities solve the problem.

The Legacy Architect profile, however, does not have income certainty as its sole objective, and the trade-offs required to access annuity mechanics are structurally incompatible with the rest of that profile’s financial architecture.

Irrevocable capital lockup. Annuitization converts a capital lump sum into an income stream permanently. The principal is no longer accessible, adjustable, or transferable.

For a Legacy Architect whose estate plan depends on controlled capital transfer; trust funding, business succession, and charitable giving, this is not a minor trade-off. It removes the primary asset from the estate architecture entirely.

No residual estate value. The mortality credit mechanism that makes annuities actuarially efficient works by pooling capital: early decedents’ capital funds long survivors’ income. This is the mechanism that allows the annuitant to receive more than their own capital could produce, but it means the annuitant’s capital does not transfer to their heirs.

The death benefit, if it exists at all, is typically a return-of-premium guarantee structured to recover the premium base, not to provide meaningful estate transfer value. For a profile whose primary financial identity is controlled multigenerational wealth transfer, this is a structural incompatibility.

Inflation and purchasing power erosion. Most fixed immediate annuities produce nominal cash flows. Over a 30-to-40-year retirement horizon, inflation erosion is not a rounding error, it is a primary risk.

A $5,000 monthly payment at age 60 purchases meaningfully less at age 85. Inflation-adjusted annuities exist but at significantly higher cost (lower initial income), and the inflation adjustment is typically CPI-linked rather than tied to the actual cost structure of a high-net-worth lifestyle.

Counterparty concentration. The actuarial guarantee is only as strong as the insurer’s balance sheet. Concentrating retirement income in a single insurer’s contractual obligation introduces counterparty risk that the diversified portfolio model was specifically designed to avoid.

State guarantee funds provide backstop protection up to statutory limits, but those limits were designed for mainstream retail policies, not large-case institutional placements.

The actuarial principles underlying annuities are sound. The implementation creates structural incompatibilities for the Legacy Architect that cannot be engineered around.

What is needed is a vehicle that imports the actuarial mechanics, guaranteed cash flows, longevity hedge, contractual certainty, without surrendering capital flexibility, estate transfer function, or counterparty diversification. That vehicle is whole life policy architecture.

How Whole Life Policy Architecture Imports Actuarial Mechanics

Whole life policies are actuarial instruments. This is not a marketing claim, it is a technical description. They are priced from mortality tables, their guaranteed cash value growth schedules are actuarially derived and legally binding, and their death benefit is a contractual obligation of the insurer’s balance sheet, not a market-return-dependent projection.

The mechanics that make pensions and annuities actuarially sound are embedded in whole life policy structure at the instrument level.

Three actuarial mechanisms transfer directly from the defined-benefit world into whole life architecture:

Guaranteed cash value growth tables. Every whole life policy illustration contains a guaranteed column: the minimum cash value at each policy year, derived from the policy’s guaranteed interest rate and mortality assumptions.

These are not projections. They are contractual minimums, legally enforceable, actuarially stress-tested, and independent of market conditions. When the equity market loses 40% of its value in 18 months, the guaranteed cash value column does not change.

This is the same contractual certainty that defined-benefit plan participants relied on — the income figure is known before the year begins.

Dividend participation as a mortality credit analog. Mutual life insurers return surplus to participating policyholders as dividends. The mechanical source of that surplus is analogous to mortality credit pooling: the insurer aggregates mortality experience, investment returns, and expense management across its entire block of participating business, then distributes surplus to policyholders based on their contribution to that block.

Dividends are not guaranteed, but their source, favorable aggregate experience across a pooled risk block, is structurally similar to the mechanism that makes pension mortality credits work. The effect is a non-correlated, above-guaranteed income enhancement that reflects the insurer’s actual experience, not the market’s.

Death benefit as longevity hedge without irrevocable annuitization. The whole life death benefit is a contractual transfer value that does not diminish as the retirement horizon extends. Unlike an annuity, it does not require surrendering capital to generate income.

The policyholder can draw from cash value through policy loans during their lifetime, creating income, while the death benefit continues to provide the estate transfer function. This is the structural mechanism that resolves the core annuity incompatibility: longevity risk is hedged by the death benefit’s contractual certainty, but the capital remains accessible and transferable during the policyholder’s lifetime.

The comparison to annuities on each actuarial dimension:

| Mechanism | Annuity | Whole Life |

| Guaranteed cash flows | ✓ | ✓ (cash value schedule) |

| Mortality credit / pooled surplus | ✓ (mortality credits) | ✓ (dividend analog) |

| Capital accessibility during lifetime | ✗ (annuitized) | ✓ (policy loans) |

| Residual estate value | ✗ or minimal | ✓ (death benefit) |

| Longevity hedge | ✓ | ✓ (contractual death benefit) |

| Counterparty risk | Present | Present; mitigated by state funds + mutual structure |

The structural conclusion: whole life architecture solves the same income certainty problem as an actuarially sound annuity, while preserving capital flexibility and estate transfer function. The trade-off is cost of insurance, the death benefit requires mortality charges that reduce early cash value relative to a pure investment account.

For the Legacy Architect, that cost of insurance is not a trade-off; it is paying for the estate transfer function they require regardless.

“The actuarial mechanics that make pensions and annuities reliable are not proprietary to institutional instruments. They exist in whole life policy structure at the contractual level — accessible outside the employer-sponsored system for the first time in private retirement architecture.”

The Wealth Maximization Account as an Actuarial Income Layer

The Wealth Maximization Account is Paradigm’s implementation of the whole life cash-flow layer, engineered specifically for the income and transfer use case.

The structural difference from a standard whole life policy is the cash-value-to-premium ratio. A standard whole life policy is optimized for death benefit: it carries a relatively high early insurance cost relative to cash value accumulation.

The WMA is structured to invert that ratio; maximizing cash value accumulation in early policy years (typically through a blend of paid-up additions and reduced base face amount) while maintaining the death benefit’s estate transfer function.

This is an actuarial trade-off: more early liquidity, somewhat lower early death benefit, with both converging toward full actuarial maturity over the policy’s life. The rationale for this structure in the retirement income context is that the policyholder needs accessible cash value at the income floor stage, not maximum death benefit in policy year three.

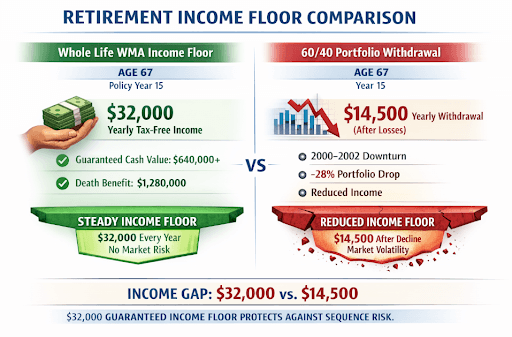

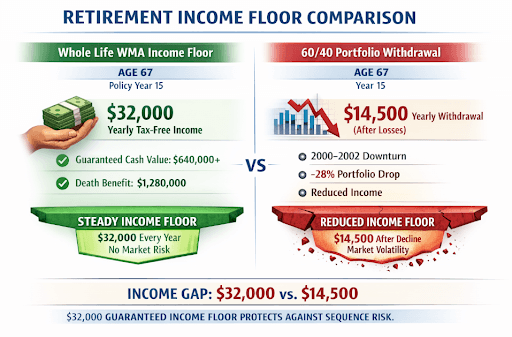

Assume a Legacy Architect, age 52, funding a WMA at $50,000/year for 10 years, $500,000 total premium commitment.

At policy year 15 (age 67, standard retirement entry point):

Guaranteed cash value: approximately $640,000 (contractual minimum, actuarially derived)

Projected total cash value with dividends: approximately $760,000 (non-guaranteed; based on current dividend scale)

Annual policy loan draw at 5% of guaranteed cash value: approximately $32,000/year

Death benefit at year 15: approximately $1,280,000 (net of outstanding loans, which are zero at this point)

*The preceding figures are estimated for illustration/educational purposes only.

The $32,000/year policy loan draw is tax-free (loans are not income), does not trigger a reportable event, has no required minimum distribution, and does not depend on the equity market’s performance in any given year.

The loan accrues interest against the policy’s cash value, but the policy’s internal growth (guaranteed plus dividends) historically offsets loan interest at current dividend scales in properly structured policies. The death benefit remains intact as the estate transfer mechanism.

Sequence-of-returns comparison:

Same $500,000 invested in a 60/40 portfolio at age 52, drawing 4% annually ($20,000/year) beginning at age 67.

If retirement begins in a sequence analogous to 2000–2002, where a 60/40 portfolio experienced cumulative losses of approximately 28% over the first three years of withdrawal, the portfolio value by the end of year three would be approximately $362,000.

A retiree responding to a 27% drawdown by re-anchoring withdrawals to current portfolio value cuts income to roughly $14,500 — a 27.5% reduction.

The WMA draw during those same three years: $32,000/year. Unchanged. The cash value growth schedule is a contractual table, not a function of equity market performance. The sequence-of-returns problem, the primary risk that makes the 4% rule probabilistic rather than certain, is orthogonal to the WMA income layer.

The practical integration model: the WMA’s $32,000 income floor covers fixed expenses. The 60/40 portfolio, no longer required to produce income in every year, is free to compound through the drawdown sequence without forced selling at depressed prices.

Sequence risk is neutralized at the layer designed to absorb it, not at the layer designed for long-term growth.

Integrating Actuarial Mechanics Into an Existing Retirement Architecture

This is not an argument for replacing the portfolio. The Legacy Architect with a well-constructed equity and fixed-income portfolio does not need to liquidate it to access actuarial income certainty. The WMA functions as an architectural layer beneath the portfolio — the income floor that changes what the portfolio is required to do.

The integration model for the Legacy Architect profile:

Income floor layer (WMA). Policy loan draws cover baseline income requirements: housing, fixed expenses, lifestyle minimum. This income is contractually certain, non-correlated with market conditions, and does not require selling portfolio assets in any given year.

The floor is actuarially grounded, it exists because of the policy’s guaranteed cash value schedule, not because the market cooperated.

Growth layer (equity/fixed-income portfolio). Once the income floor is covered by a non-market-correlated source, the portfolio’s mandate changes from “produce income every year” to “grow over the full horizon.”

The portfolio no longer needs to be positioned defensively for early-year income production. Sequence-of-returns risk, the primary argument for heavy fixed-income allocation in early retirement years, is dramatically reduced. The portfolio can hold a more growth-oriented allocation because the floor doesn’t depend on it.

Estate layer (WMA death benefit + trust structure). The death benefit provides the controlled transfer value that funds the trust architecture. Trust instruments define how and to whom capital transfers; the WMA death benefit provides the contractual, actuarially-certain capital that trust structure requires at the moment of transfer.

This is the same function the whole life policy serves in a multigenerational wealth transfer architecture, the mechanism that makes the estate plan executable, not just structurally correct.

The actuarial insight here is the same one that defined-benefit architects have applied for decades: income certainty is built from the floor up, not from the portfolio down.

Establish a contractually guaranteed base, then layer growth and flexibility above it. The WMA is the mechanism that imports this architectural principle into a private, non-employer-sponsored retirement structure.

For the reader asking how actuarial science applies to individual retirement income optimization: this is the answer. The mechanics exist. The instrument is not institutional.

The structure is available outside the pension system, designed for exactly the retirement income architecture problem that the defined-contribution era transferred to individuals without transferring the tools to solve it.

Schedule a Legacy Planning Call

If your retirement income architecture does not yet include a non-market-correlated income floor with actuarial-grade certainty, the structural gap is knowable and closable.

A Legacy Planning conversation at Paradigm is an architectural review: your current income structure, your longevity exposure, your estate transfer objectives, and where a WMA income layer integrates with what you’ve already built. Not a product pitch — a technical review at the level of sophistication this problem requires.

Schedule a Legacy Planning Call

Not ready for a call? The WealthScore Assessment provides a diagnostic baseline on your current income certainty, liquidity structure, and estate transfer readiness.