You ran the numbers for years.

You tracked every dollar, optimized your savings rate, held through the drawdowns, and one morning your spreadsheet confirmed what you’d been working toward for a decade: you hit the number. The 4% rule cleared. You were done.

Six months later, you’re reading a thread called “the isolation of early retirement” and something in it lands harder than you expected. Not the isolation specifically, maybe that’s not your issue. But the question underneath it: Is this what I thought it would be?

That discomfort isn’t a mindset problem. It’s structural. A number in a brokerage account is not a financial system. And the FIRE movement, for all the rigorous work it’s done on accumulation, left the post-accumulation architecture mostly unbuilt.

What the 4% Rule Actually Is; and What It Isn’t

The 4% rule comes from the Trinity Study; a 1998 analysis of historical portfolio survival rates across 30-year retirement windows. The finding: a 4% initial withdrawal rate, adjusted annually for inflation, survived most historical 30-year periods with a diversified stock and bond portfolio.

That’s a probability framework, not a guarantee. It was designed for a 30-year retirement horizon. It does not address what happens if your retirement runs 40 or 50 years, which is a real scenario for someone who retires at 40 or 42.

The math changes materially when you extend the withdrawal window by 10–20 years.

More importantly, the 4% rule does not address sequence-of-returns risk. A significant market drawdown in years 2 through 5 of retirement creates permanent portfolio damage in a way that the same drawdown in year 15 does not.

If you retire in 2000 or 2008, both real historical moments, the early-year drawdown depletes the principal your future growth depends on. The math doesn’t fail on average. It fails in timing.

The FIRE community knows all of this. The safe-withdrawal-rate debates, the variable withdrawal strategies, the bond tents, the cash buffer arguments, these are active, sophisticated discussions.

The gap isn’t knowledge. The gap is structural: there’s no income-producing *mechanism* in the standard FIRE stack. There’s a pile, and a depletion schedule, and probability math about how long the pile lasts. That’s a different thing than a system.

The Difference Between a Pile and a System

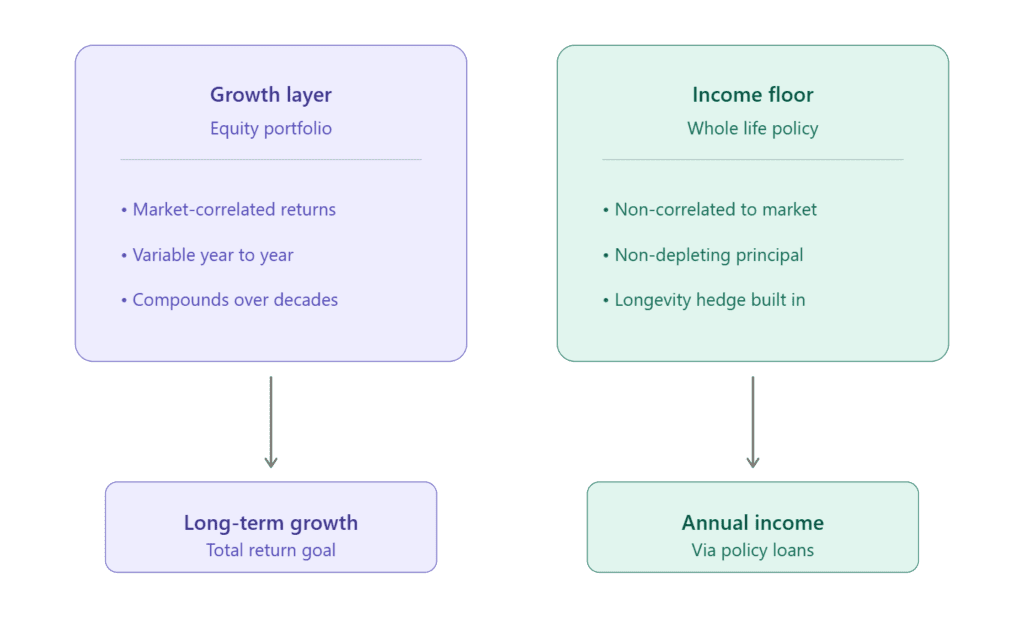

A pile is a store of value that shrinks when you use it. The FIRE portfolio; index funds, bonds, cash, is a pile. A very carefully built, tax-optimized, thoroughly analyzed pile. But a pile.

A system is a structure that produces output. Drawing from it doesn’t necessarily reduce its productive capacity, because the system has feedback loops, replenishment mechanisms, and sources of production that aren’t purely dependent on the pile’s current size.

This distinction matters because the psychological experience of living off a pile is fundamentally different from the experience of living off a system.

When the market is down 25%, drawing from a pile accelerates the damage. When you’re drawing from a system with a non-market-correlated income floor, a 25% drawdown in the equity portfolio is a problem for the growth layer, not an existential threat to the income layer.

The alternatives the FIRE community has largely evaluated and rejected:

Annuities — yes, they produce income, but they require permanent capital lockup and loss of control. The FIRE community, which built an entire framework around controlling their financial life, isn’t handing over a lump sum to an insurance company in exchange for a monthly payment with no access to the underlying asset.

Bonds — low yield, still depleting, and the inflation sensitivity that 2022 made viscerally clear.

Rental real estate — produces income but introduces active management, liquidity risk, and concentration exposure. Not passive. Not simple.

What most FIRE-adjacent financial advisors haven’t clearly explained is a fourth option: a whole life policy architecture designed specifically as a cash-flow layer; one that operates as a parallel structure alongside the equity portfolio, not as a replacement for it.

How the Cash-Flow Layer Works

The post-accumulation investor needs three properties that the standard FIRE stack doesn’t cleanly provide:

A non-depleting income floor. A base income source that doesn’t depend on the market being up in any given year. Not “the portfolio is big enough that 4% is probably fine” an actual floor, structurally separated from market correlation.

Liquidity without a taxable event or a penalty. Access to capital that doesn’t trigger income recognition, doesn’t pull from the equity portfolio at a loss, and doesn’t have surrender charges or lock-in periods.

A longevity hedge. A mechanism that increases in value over time rather than depleting — one that doesn’t care whether the retirement runs 30 years or 50.

A properly structured whole life policy provides all three.

Here’s how it works: the policy accumulates cash value at a guaranteed rate, with additional dividend crediting in participating policies. That cash value is accessible via policy loans, a mechanism that does not trigger a taxable event, does not require selling any underlying asset, and does not reduce the policy’s death benefit at a 1-to-1 ratio (because the death benefit and the cash value are separate policy components).

The death benefit itself transfers outside probate and outside the taxable estate when structured correctly.

The critical insight for the FIRE audience is what this does to the portfolio’s job. If the whole life policy provides an income floor, even a partial one, the equity portfolio no longer has to perform every single year. It has to perform over time.

Sequence-of-returns risk in years 1 through 7 becomes manageable when there’s a non-market-correlated source of income covering baseline expenses during the drawdown period. The portfolio can recover without being simultaneously depleted.

A pile is a store of value. A system is a structure that produces output. The FIRE movement built extraordinary piles. The post-accumulation phase requires a system.*

This isn’t replacing index funds. It’s building the structural layer underneath them that the standard FIRE playbook left out.

The Wealth Maximization Account in a Post-Accumulation Architecture

Paradigm Life’s implementation of this structure is the Wealth Maximization Account; a specifically engineered whole life instrument designed to maximize cash value accumulation while preserving the income and transfer functions.

This is not a standard whole life policy. Standard whole life policies are typically optimized for death benefit, they accumulate cash value slowly because the premium structure prioritizes the insurance component.

The WMA is structured differently: premium design and dividend participation are calibrated to accelerate cash value growth while maintaining the death benefit’s longevity function.

For the FIRE community specifically, the WMA fits at two points in the financial architecture:

During the accumulation phase: The WMA builds a parallel cash-value base alongside the index portfolio. For someone in a 10-year FIRE sprint, this is a second track, growing separately, not correlated to market performance, accessible at any time.

At and after the transition point: The WMA provides the income floor. Policy loans drawn against cash value create a tax-efficient income stream that doesn’t trigger sequence-of-returns risk in the equity portfolio. In a down market year, you draw income from the policy loan rather than the portfolio, the portfolio holds, and the WMA’s internal mechanics replenish against the death benefit over time.

Over the 40-year horizon: The death benefit ensures the wealth transfer function is preserved regardless of how much cash value was accessed during life. The policy is designed to function across a long retirement, not one that runs out if you live longer than the Trinity Study’s 30-year model assumed.

The FIRE community has solved the accumulation problem with exceptional discipline. The WMA addresses the structural gap in what comes after.

What Changes When There’s an Income Floor

Structurally: the portfolio’s mandate shifts. It no longer needs to produce income every year, it needs to produce growth over time. Those are different optimization targets. A portfolio optimized for total return over 40 years can hold through a three-year drawdown if the bills are covered by a non-correlated income floor.

A portfolio that has to produce income every year, regardless of market conditions, is permanently exposed to sequence-of-returns risk.

There’s a second thing that changes, and it’s worth acknowledging even in a piece that’s primarily structural.

Part of what the isolation thread captures is the loss of an external rhythm. A W-2 wasn’t just income, it was a structure that organized time and created an external measure of productive engagement.

When the income comes from selling shares, the income mechanism is invisible. There’s no feedback loop, no signal that the system is working. The number just gets smaller.

When income comes from a system that produces, a policy loan that the underlying cash value continues to compound against, the mechanism is visible. Money arrives not because you sold something, but because the structure is working. That’s a small thing functionally. It’s not a small thing experientially.

This isn’t a pitch for going back to work. It’s an observation that the financial architecture shapes the experience of financial independence, not just the math. Building a system that behaves like a productive mechanism, rather than a pile being drawn down, is both a structural improvement and a qualitative one.

The FIRE community did exceptional work on accumulation. The post-accumulation architecture is the next problem. Most FIRE-adjacent financial advisors aren’t equipped to address it, their models stop at the portfolio, because that’s where the accumulation conversation ends.

The Structural Gap Most Plans Leave Open

The question worth asking your current financial setup is specific: Does my plan account for where the income comes from if the market is down 30% in year 3?

Not “will my portfolio survive over 30 years at historical averages,” that’s the Trinity Study’s question, and you already know the answer. The narrower question: what is the income source during a sustained early-retirement drawdown, and does that source have its own structural independence from the equity portfolio?

If the answer is “I draw less” or “I go back to consulting,” those are valid contingency plans. But they’re contingency plans, not structural solutions. A structural solution is an income floor that doesn’t depend on the portfolio’s performance in any given year, built into the architecture before you need it.

That’s the conversation most FIRE plans haven’t had, and it’s exactly what a WealthScore assessment is designed to surface.

Take the WealthScore Assessment

See where your current financial structure stands on income certainty. The assessment identifies the structural gaps in your post-accumulation architecture — not a sales call, a diagnostic.

Or would you rather talk to one of our Wealth Strategists? Schedule a Discovery Call a direct conversation with a Paradigm advisor on post-accumulation structure.