Most financial advice is built around a single objective: grow capital efficiently. Maximize returns on deployed assets. Put every dollar to work.

The logic is sound on its face; idle capital is underperforming capital, and compounding works best when it is uninterrupted.

The problem is what that design philosophy produces at scale. A high earner who has followed it faithfully for a decade often arrives at a position that looks strong on a balance sheet and feels surprisingly constrained in practice.

The retirement accounts are funded. The real estate is appreciating. The business equity is building. And when a capital need arrives; an opportunity, a disruption, a strategic pivot, the answer is: everything is deployed.

That is not a liquidity problem in the conventional sense. It is a cash flow architecture problem. The individual instruments are working. The system was never designed to be accessible.

This is the design flaw at the center of most high-net-worth financial structures, and it is not inevitable. Liquidity is not a feature you add to a wealth system after the growth positions are funded. It is the first design principle.

When it is built in from the foundation, the architecture performs differently across every dimension. When it is treated as an afterthought, the system is productive and brittle, optimized for the conditions you plan for, exposed in exactly the conditions you cannot.

The False Choice That Most Financial Architecture Is Built On

The conventional framing presents liquidity and growth as competing demands. Capital in a liquid, accessible account is capital not compounding at full efficiency. The efficient portfolio theory runs on this logic: every dollar should be allocated to its highest-return use, and holding liquid reserves is an allocation cost.

That framing is not entirely wrong. It is incomplete, and the incompleteness compounds.

Here is what the efficient-deployment architecture produces in practice: a Sovereign CEO with $5 million in net worth who receives an acquisition offer for a partial stake in a complementary business. The deal requires $800,000 in capital within 30 days.

The $5 million is real. It is held in a real estate position with a 60-day closing minimum, a 401(k) with distribution rules and tax exposure, a brokerage account where liquidation triggers a capital gains event in a high-income year, and a business that does not distribute operating capital to ownership on short notice.

The capital exists. The accessible capital does not. The opportunity is declined; not because of net worth, but because of design.

This scenario is not hypothetical. It is the structural reality of a financial system built entirely around the principle of deployed efficiency without a coordinating accessibility layer.

The false choice: grow your capital, or keep it accessible, is not a constraint of the financial universe. It is a constraint of a specific architectural approach. A system designed with liquidity as a first principle does not choose between the two. It coordinates the architecture so that both are properties of the whole structure simultaneously.

The central question worth asking, and one that most financial planning conversations skip entirely, is this: was your financial architecture designed to be accessible, or only to be productive?

What “Liquidity as a Design Principle” Actually Means

Liquidity, in architectural terms, is not a feature of any single account. It is a property of the system.

A liquid financial architecture is one that can meet a capital need without triggering a cascading disruption: a forced liquidation at an inopportune time, a taxable distribution in a high-income year, a productive position unwound before its term. The capital moves. The rest of the system continues.

That definition distinguishes liquidity-as-architecture from liquidity-as-balance. A savings account balance is liquid in the narrow sense; you can access it.

But a savings account held in isolation, without coordination with the income structure, the protection layer, and the legacy architecture, is not an accessible wealth system. It is a single instrument performing a single function, disconnected from the whole.

Most high earners who examine their financial picture honestly find that this is what they have: a collection of instruments, each performing its individual function, without a coordinating principle that makes the system accessible as a whole.

The retirement account grows tax-deferred but is locked behind distribution rules. The real estate appreciates but does not distribute. The business equity builds but requires a transaction to realize. The brokerage account is technically liquid but taxable on access and exposed to the same market conditions that typically coincide with disruption events.

Every number on the statement is real. The accessible capital at the moment it is needed is a fraction of it.

Within the Perpetual Wealth Strategy framework, the liquidity architecture lives in the Certainty dimension; the foundation layer on which every other financial dimension depends.

When the Certainty layer is properly funded and structured, disruptions are absorbed without dismantling what is above them. An unexpected expense does not force a liquidation. A business revenue dip does not require an IRA withdrawal. A market correction does not compress the capital available for a strategic opportunity.

When the Certainty layer is underfunded, thin, or held in the wrong instrument, the reverse is true: the first disruption that arrives is not absorbed. It cascades. The tax event happens at the wrong time. The growth position is liquidated before its term. The architecture that was performing in the absence of pressure fails precisely when pressure arrives.

That is not bad luck. It is design.

The Four Places Liquidity Determines Your Financial Outcome

The argument for liquidity as a first principle is not that accessibility is an end in itself. It is that a functioning liquidity layer changes the outcome in every other dimension of the financial architecture. Here is where the difference is actually felt.

Certainty: The Foundation Layer

The reserve is where the liquidity architecture begins. How it is funded, where it lives, and how it is accessed determines whether a disruption is an inconvenience or a structural event.

A reserve held in a savings account is stable and accessible, and it earns income-taxable interest at a rate that does not keep pace with inflation. It is not compounding. It is sitting.

A reserve held in a taxable brokerage account in a conservative allocation earns a return, and creates a taxable event when liquidated. The moment you need it most is typically the moment you can least afford the tax drag: a disruption year often coincides with compressed income, not expanded tax room.

Whole life insurance cash value, accessed through a policy loan, performs neither of those tradeoffs. The loan is not a taxable event, you are borrowing against collateral you own, not distributing an asset.

The full cash value continues to compound on the policy’s guaranteed growth and dividend schedule while the loan is outstanding, as if the loan does not exist. There is no credit approval process, no timeline imposed by a lender, no repayment schedule with external enforcement.

The Certainty layer, structured this way, is both stable and productive. It does not sacrifice one to achieve the other. That is what makes it load-bearing, and what makes a reserve held in the wrong instrument a liability masquerading as a safety net.

Cash Flow: How Liquidity Changes Your Income Options

Income sourcing decisions are made under constraint or by design, depending on whether the liquidity layer is funded.

A Sovereign CEO whose only accessible capital is business distributions faces every income decision as a constraint problem: how much can the business afford to distribute this quarter, and what is the tax exposure on that distribution?

The income arrives on the business’s schedule, in the form the business generates it, taxable at the applicable rate.

A Sovereign CEO with a funded whole life policy has an additional income source available at any time: policy loan access, which is not taxable income.

In a high-income year; when additional business distributions would compound the tax exposure, living expenses or capital needs can be funded from the policy loan rather than from a taxable distribution. The following year, when income is lower, the loan is repaid at a lower cost.

This is not a tax strategy in the transactional sense. It is a structural outcome of having a liquid layer coordinated with the income architecture. The tax efficiency is a byproduct of the design, not a maneuver executed on top of it.

Without the liquidity layer, this flexibility does not exist. Income decisions are constrained by the instruments available, not optimized by the structure built.

Tax: How Illiquidity Creates Involuntary Tax Events

The most common source of unnecessary tax drag in a high-net-worth portfolio is not a failed tax strategy. It is a disruption that forces a liquidation at the wrong moment.

- A business slowdown that forces an early IRA withdrawal, taxable as ordinary income, plus a potential penalty.

- A large unexpected expense that forces a brokerage sale, capital gains in a high-income year.

- A real estate gap that forces a distribution from a retirement account to cover carrying costs, compressing the tax room needed for a planned Roth conversion.

Each of these is a structural failure, not a planning failure. The tax event did not arrive because the tax strategy was wrong. It arrived because the liquidity layer was too thin to absorb the disruption, and the architecture had no other option.

A funded Certainty layer prevents these events. Not through tax planning, through design. The policy loan covers the gap. The IRA stays in place. The brokerage position holds through the disruption. The Roth conversion executes on schedule.

The tax outcome improves not because anything in the Tax dimension changed, but because the Certainty layer did its job.

Legacy: How Accessible Wealth Transfers Differently

The architecture that makes wealth accessible during life is largely the same architecture that makes it transferable after it.

Illiquid assets create transfer complexity: probate exposure, estate sale dynamics, forced beneficiary distributions, discounts applied to illiquid positions, and income tax liability that transfers along with the asset.

A $3 million traditional IRA balance looks like $3 million until the beneficiary runs the distribution math, at their income tax rate, over a 10-year distribution window under current law.

A whole life death benefit transfers income-tax-free to named beneficiaries, outside of probate, immediately upon claim.

The transfer does not require a sale, a distribution schedule, or a tax calculation. It is the most structurally clean legacy transfer mechanism available, and it is a direct byproduct of the same instrument that performs the liquidity function during life.

The legacy transfer architecture and the living liquidity architecture are not separate planning conversations. They are the same design decision, producing outcomes that compound in both directions.

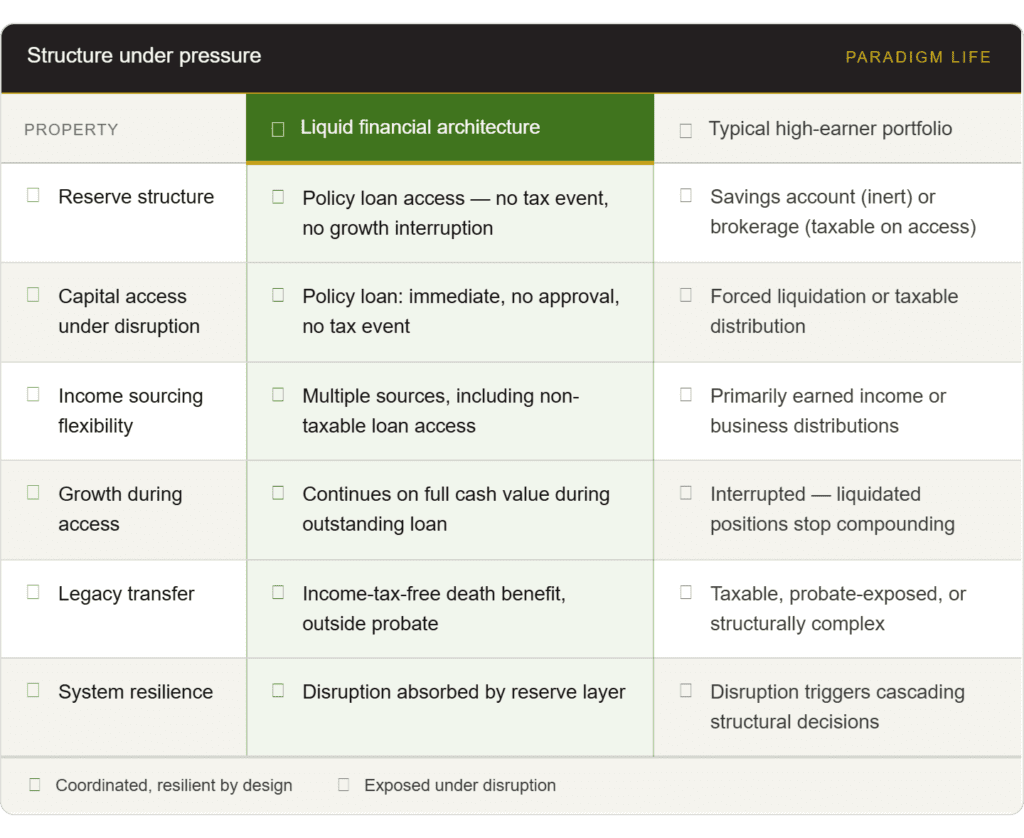

What a Liquid Financial Architecture Looks Like vs. What Most High Earners Actually Have

The gap between a liquid financial architecture and the typical high-earner portfolio is not a function of net worth. It is a function of design. The same net worth can produce entirely different accessible-capital pictures depending on how the architecture was built.

Most high earners who read this table recognize themselves somewhere on the right side. That recognition is worth paying attention to.

The architecture on the left is not a different portfolio. It is not a different level of wealth. It is the same capital coordinated around a different design principle, one that treats accessibility as a structural requirement from the foundation up, rather than a feature to be added when the growth positions are fully funded.

Most financial systems are designed to grow capital. Whether yours is also designed to be accessible is a diagnostic question, not a general one.

The WealthScore Quiz is a six-question diagnostic that shows whether your capital is liquid, protected, and coordinated so no single event can force a bad financial decision.

How to Build Liquidity Into the Architecture — Not Onto It

The distinction between liquidity built in and liquidity bolted on is not semantic. It produces different outcomes under pressure, and the difference only becomes visible when pressure arrives.

The order of operations matters.

Most financial planning sequences start with growth positions and work backward to reserve sizing: fund the 401(k) to the contribution limit, deploy excess capital into investment accounts or real estate, and hold whatever remains in a savings account as the reserve.

The reserve is what is left over after everything else is funded. This sequence produces the architecture on the right side of the table above.

The reserve is underfunded because it was funded last. The liquidity layer is thin because it was treated as a residual.

The sequence that produces a liquid financial structure runs in the opposite direction. The Certainty layer; the funded reserve, structured in the right instrument, is established first.

Growth positions are built on top of a functioning foundation. This is not a conservative strategy; it is a load-bearing sequence. You cannot build a durable structure on an unfunded base.

The reserve sizing problem.

The conventional “three to six months of expenses” guidance was not designed for financial complexity. It was designed for a W-2 household with predictable income, predictable expenses, and a single income source.

Applied to a Sovereign CEO with variable business revenue, multiple income streams, and capital needs that can arrive in large, non-linear amounts, it produces a reserve sized for a simpler problem than the one actually being solved.

Proper reserve sizing for real complexity models the actual disruption scenarios: a quarter with compressed business revenue, a strategic opportunity requiring immediate capital, a major unexpected expense, a market environment where liquidating growth positions would lock in losses.

The reserve needs to be adequate to absorb any one of those scenarios without triggering a cascade. The multiple-of-expenses calculation does not produce that number.

The instrument selection problem.

Where the reserve lives determines its tax treatment on access, its compounding behavior, and its interaction with the rest of the financial structure. These are not interchangeable decisions.

A properly structured whole life policy performs every reserve function simultaneously: stable (guaranteed cash value growth, not subject to market fluctuation), accessible (policy loan available without approval, timeline, or credit event), tax-efficient on access (loan proceeds are not taxable income), and continuously compounding (full cash value credits growth during the loan period).

No other single instrument does all four.

This is not a product recommendation. It is an architectural observation. The reserve instrument should be selected for its structural properties, how it performs the reserve function, how it interacts with the income and tax layers, and how it contributes to the legacy architecture.

A decision made at this level on the basis of yield alone misses the load-bearing role the reserve actually plays.

The coordination requirement.

Liquidity is not something you add to a financial system by purchasing an instrument. It is a property that emerges from coordinating the reserve structure, the income sourcing, the protection coverage, and the legacy architecture around a shared design principle.

That coordination requires seeing the whole structure, not just its individual components, to build it correctly.

The Foundation Question

You did not arrive here because you lacked financial instruments. You arrived here because the instruments you have are not coordinating the way you expected. The net worth is real. The accessible wealth is smaller than the balance sheet suggests. The system is working, and somehow, it still feels constrained.

That is a design signal. It is not a market problem, not a product problem, and not a problem that resolves by adding another instrument to an architecture that was never designed around accessibility in the first place.

The question worth asking, before any new allocation, any rollover decision, any next financial move; is whether your current architecture was built with liquidity as a first principle or as an afterthought.

The answer to that question shapes every outcome downstream: the tax events you can avoid, the income flexibility you can exercise, the disruptions you can absorb, and the legacy your structure ultimately produces.

The WealthScore Quiz is where that diagnostic begins. Six questions. Free. No sales call required to complete. It shows whether your capital is liquid, protected, and coordinated so no single event can force a bad financial decision.

It turns wealth from something you worry about managing into a system that supports your life, opportunities, and legacy with confidence.

Get Your Free WealthScore Here

Ready to move from diagnostic to architectural redesign?