The idea that your family can function like its own private bank isn’t metaphor. Here’s the mechanics, the asset behind it, and how people are using it to build wealth without depending on Wall Street.

The Short Answer

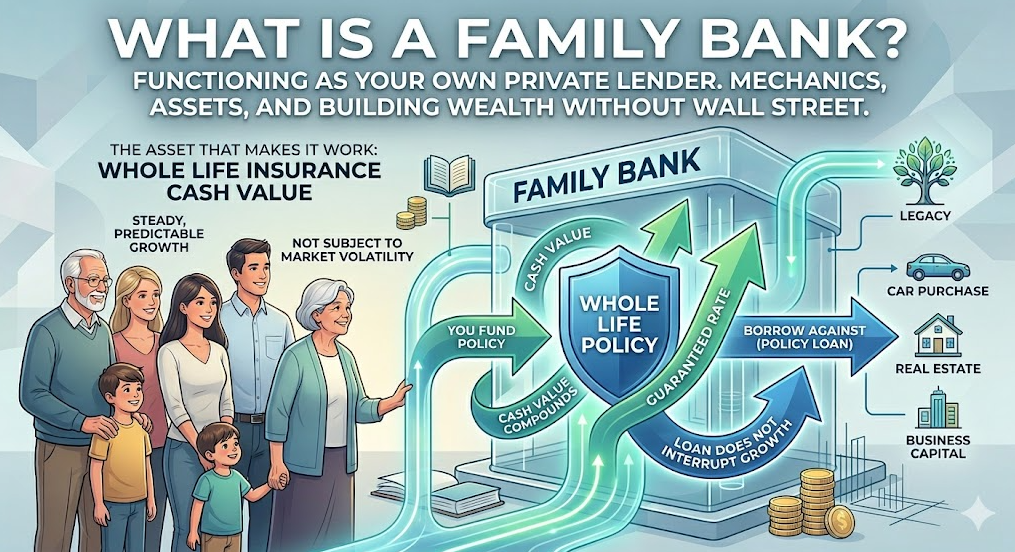

A family bank is a financial structure, typically built around a specially designed whole life insurance policy, that lets you function as your own lender.

You build cash value inside the policy, then borrow against it to fund purchases, investments, or opportunities, while your money continues to grow uninterrupted.

The “bank” is the structure, not a literal institution.

Why People Are Searching for This

You’ve probably heard the concept under a few different names; infinite banking, bank on yourself, the family banking system. Maybe it came up in a podcast, a conversation with an advisor, or an ad that kept appearing in your feed.

The underlying mechanics are the same across all of them. What varies is who’s teaching it and whether the policy behind it is structured correctly.

If you’re here because you’re trying to figure out whether this is real or a sales pitch, that’s the right question to be asking. The answer is that the structure is real, the math is real, and the results depend almost entirely on how the policy is designed.

That’s what we’ll walk through here.

The Asset That Makes It Work: Whole Life Insurance Cash Value

Whole life insurance has two components: a death benefit and a cash value account.

The cash value grows at a guaranteed rate. It is not subject to market performance. It does not drop when the S&P 500 drops. It does not have a “bad year.” It compounds over time at a rate defined in the policy, and because it isn’t tied to any index or fund, it holds its value regardless of what markets are doing.

This makes it a different category of asset, not a stock, not a bond, not a savings account. It’s a policy-based store of value with a predictable growth floor. That’s the stability layer. That’s what the banking function runs on.

For people who’ve spent years watching retirement accounts fluctuate with the market, this distinction matters. The cash value doesn’t participate in the upside of a bull market, but it also doesn’t participate in the losses of a downturn.

For a lot of families, that’s a feature, not a limitation.

How the Banking Function Works

Here’s the mechanics, step by step.

1. You fund a whole life policy.

Contributions go into both the insurance cost and the cash value account. A well-structured policy is designed to minimize the insurance cost and maximize the cash value accumulation from the beginning.

2. The cash value builds over time.

In a well-designed policy, meaningful cash value becomes accessible within two to five years. In a poorly designed one, that window can stretch to ten or fifteen.

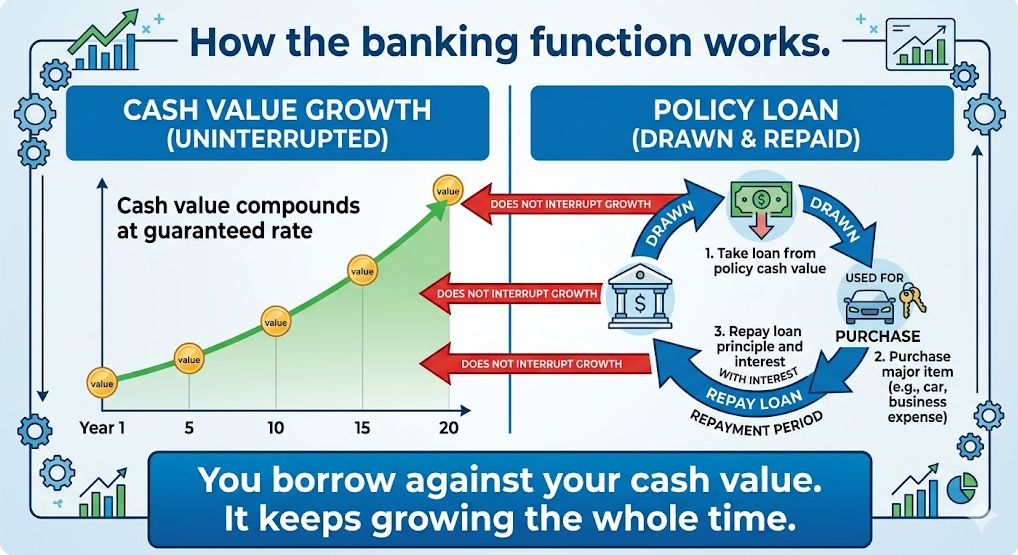

3. You borrow against your cash value — not from it.

When you want to access funds, you request a policy loan from the insurance company, using your cash value as collateral. You are not withdrawing the money. You are borrowing against it while it stays in place.

4. You use the loan for whatever you need.

Car purchase. Real estate down payment. Business capital. Emergency fund. The loan proceeds are yours to direct; no approval process, no stated purpose required.

5. Your cash value keeps growing the entire time.

This is the part that surprises most people. While the loan is outstanding, your full cash value continues to compound at the guaranteed rate. The loan doesn’t interrupt the growth. Your money is doing two jobs simultaneously: collateral for the loan, and an asset earning a return.

6. You repay on your own schedule.

There is no mandatory repayment timeline. You can repay on a schedule you set, repay slowly, or not repay at all; though restoring the loan returns your full borrowing capacity for the next use.

What Makes It a “Family” Bank

The structure is designed to outlast you.

When you die, the death benefit passes to your beneficiaries income-tax-free. But the structure can do more than generate an inheritance; it can become a capital system the next generation inherits and borrows from.

Adult children can be added to the structure. Policies can be stacked across generations. The family bank doesn’t end at your policy, it can become the financial foundation your children build from, not just a check they receive.

This is the generational dimension that most conversations about infinite banking leave out. The structure works in one generation. It compounds across several.

Who This Works For — and Who It Doesn’t

This structure isn’t the right fit for everyone, and we’d rather say that plainly than let you find out later.

It works well for:

- High earners; typically $100,000+ household income, with consistent cash flow available for premiums

- Business owners who want a liquid capital reserve that earns while it sits

- Pre-retirees who want guaranteed growth not tied to market sequence-of-returns risk

- Anyone who regularly borrows to fund purchases (vehicles, real estate, business needs) and wants to recapture the interest they’re currently paying to someone else

It’s less suited for:

- People who need the money in the next one to two years, the first few years are policy-building years, not immediate-liquidity years

- People with significant health challenges; the life insurance component requires underwriting

- People expecting short-term returns that compete with aggressive equity positions; this structure doesn’t work that way, and anyone telling you it does is misrepresenting it

The reason we include this section is simple: a structure this powerful, used in the wrong situation, doesn’t perform. The fit matters as much as the design.

How Paradigm Life Structures These Policies

Not every whole life policy functions as a family bank. The policy has to be designed specifically to maximize early cash value — not to maximize the death benefit, and not to maximize agent commission, which is unfortunately the default in a lot of standard policy designs.

Paradigm Life specializes in Specially Designed Life Insurance; policies structured from the ground up to prioritize cash value accumulation while keeping insurance costs as lean as possible.

The design difference is significant in practical terms: a standard policy might take ten to fifteen years to build meaningful borrowable cash value. A well-designed one can be functional in two to three.

If you’ve looked at whole life insurance before and concluded it was a slow, expensive product, there’s a reasonable chance you were looking at a standard design. The policies we build don’t work that way.

Common Questions

Is a family bank the same as infinite banking?

Yes — they describe the same core structure. “Infinite banking” refers to a specific teaching system built around these mechanics; “family bank” is a broader term for the same concept applied to a family financial unit. The underlying asset and the borrowing mechanic are identical.

Do I need a lot of money to start?

The structure works best for households with consistent cash flow available for premiums; typically $12,000 to $25,000 per year at minimum to build meaningful capital at a useful pace. Policies can be funded at various levels, but the timeline to usable cash value is directly connected to how the policy is funded.

What happens to the money when I die?

The death benefit passes income-tax-free to your beneficiaries. If the policy is part of a multi-generational structure, heirs can inherit both the death benefit and the policy’s framework, continuing the banking function rather than simply receiving a payout.

Is this legal? Is it some kind of tax shelter?

It’s legal — whole life insurance and policy loans are governed by standard insurance law and have been for more than a century. Growth inside the policy is tax-deferred; policy loans are tax-free because they’re loans, not income. It is not a tax shelter in the conventional sense; it’s a standard insurance product with favorable tax treatment built into the structure by law.

How is this different from a savings account or a 401(k)?

A savings account earns interest but has no insurance component and isn’t a borrowable asset in the same sense. A 401(k) is market-correlated, taxed on withdrawal, and carries sequence-of-returns risk, meaning the timing of market downturns relative to your retirement date directly affects what you end up with.

Whole life cash value grows at a guaranteed rate, is not market-correlated, and can be accessed via policy loan without triggering a taxable event. These are structurally different instruments solving different problems.

Ready to Design Your Family Bank?

Paradigm Life works with families to structure policies that maximize early cash value and build a capital system built to last. The starting point is a conversation. No obligation, no pitch, just a clear picture of whether and how this fits your situation.

Not ready for a call? Start with this short, insightful quiz to determine the strength of your wealth strategy: