Most high earners have done the work on tax strategy. They’ve maximized the 401(k). They’ve evaluated the Roth conversion window. They understand tax-loss harvesting. They’ve had the conversation with a CPA about qualified business income deductions.

These are legitimate decisions, executed competently, producing real outcomes. And yet, for many of the same people, the tax drag on their overall financial picture is larger than the individual optimizations suggest it should be.

The instruments are tuned. The system is not coordinated. And the difference between those two things compounds over decades in ways that account-level optimization cannot address.

This article is not a different list of tax tools. It is a different frame: tax efficiency is not a feature of any single account type. It is a property of a whole financial architecture, and building it requires coordinating across every dimension of that architecture simultaneously.

What Single-Dimension Tax Advice Gets Right — and Where It Stops

Single-dimension tax strategy advice is not wrong. It is incomplete.

A 401(k) contribution reduces current-year taxable income. That is true.

A Roth conversion shifts tax exposure from future distributions to the current year, which is advantageous when today’s bracket is lower than tomorrow’s expected bracket. That is also true.

Tax-loss harvesting offsets realized gains and reduces net capital gains exposure. Still true.

These are real tools producing real outcomes. Any financial advisor or CPA worth working with knows them and uses them appropriately.

What this category of advice does not address is the interaction between any single account optimization and the surrounding financial structure.

The 401(k) contribution is evaluated for its current-year tax impact, not for how the deferred balance interacts with your income sourcing flexibility in retirement, your required minimum distribution exposure at 73, or your beneficiary’s income tax liability at transfer.

The Roth conversion is evaluated against your current and projected bracket, not against your liquidity position, your business income variability, or the legacy architecture that determines whether tax-free growth actually reaches your heirs intact.

The analogy is useful: tuning one instrument in an orchestra is real work. A properly tuned instrument sounds better than an out-of-tune one. But if the other instruments are uncoordinated, playing in different keys, at different tempos, without a shared arrangement, the tuned instrument does not produce the sound you were trying to create.

Single-dimension tax advice produces local efficiency. A coordinated architecture produces systemic efficiency. For a high earner operating at real financial complexity, the gap between those two outcomes is not marginal.

The Four Dimensions Where Tax Efficiency Actually Lives

The Perpetual Wealth Strategy framework organizes a complete financial architecture across four dimensions: Certainty, Cash Flow, Tax, and Legacy.

Most tax-strategy advice operates exclusively inside the Tax dimension; account selection, contribution strategy, conversion timing, harvesting mechanics. These are important. They are one of four places where tax efficiency is actually determined.

Certainty: How Your Liquidity Structure Affects Your Tax Exposure

The Certainty layer is your liquidity and protection foundation: the funded reserve, the spending strategy, the baseline coverage that prevents a single disruption from dismantling the structure you’re building.

What most tax-strategy conversations miss is that the Certainty layer has a direct tax dimension. Where your reserve lives determines what you pay, and what you’re forced to do, when you need to access it.

A reserve held in a taxable brokerage account, even in a conservative allocation, is not a reserve. It is an investment exposed to the same market conditions that typically produce disruptions, and liquidating it under pressure triggers a capital gains event at the moment your income may already be compressed.

A reserve held in a money market or savings account is accessible and stable, but it is inert capital: it earns income-taxable interest and does not participate in any compounding mechanism.

Whole life insurance cash value, accessed through policy loans, is neither. It is accessible without a taxable event. It continues compounding on the full cash value while a loan is outstanding. The policy credits interest and dividends as if the loan does not exist. And it does not require liquidation to access, which means a disruption year does not force a taxable event at the worst possible moment.

The Certainty layer either protects your tax position or silently erodes it, depending on how it is structured. Most financial plans do not treat this as a tax question. It is.

Cash Flow: How Income Sourcing Determines Your Tax Reality

The most consequential tax lever available to a high earner is not account selection. It is income sourcing.

Earned income; W-2 wages, Schedule C business income, self-employment income, is taxed at ordinary income rates, subject to self-employment tax for business owners, and has no structural flexibility in timing or sourcing.

Every dollar of earned income arrives in the year you earn it and is taxed at the highest applicable rate for that year.

Passive income from investment distributions, rental income, and business equity distributions is taxed differently depending on its source and how it is structured.

For example, qualified dividends carry preferential rates. Long-term capital gains are taxed below ordinary income. Rental income carries depreciation offsets that most other income types do not.

Policy loan access from a whole life policy is not taxable income at all. You are borrowing against collateral you own. There is no W-2, no 1099, no Schedule C entry. The access is flexible, you draw what you need, when you need it, without a tax event.

A Sovereign CEO or high-earning professional who sources income exclusively from earned income or business distributions is exposing every dollar of operational income to the highest applicable rate, in the year it arrives, without flexibility.

A structured financial architecture that coordinates multiple income types, including policy loan access for liquidity needs, reduces peak-year exposure without deferral gymnastics.

This is not a loophole. It is structural. It requires intentional architecture, not a transaction.

Tax: The Dimension Most Advice Actually Addresses

This is where conventional tax-strategy advice lives, and it is real and important. Account selection (401(k), IRA, Roth, HSA, taxable), contribution strategy, Roth conversion timing, tax-loss harvesting, qualified business income deductions, charitable giving vehicles; these are legitimate tools with meaningful outcomes.

The question is not whether these tools are worth using. They are. The question is whether they are coordinated with the other three dimensions or operating in isolation.

A Roth conversion optimized for current-year bracket without considering the liquidity impact, or the policy loan access that might have funded the year’s expenses without requiring a taxable distribution at all, is a locally optimized decision made without full architectural context.

It may still be the right call. But it should be made with the full picture, not just the account-level math.

Legacy: How the Transfer Architecture Determines the Final Tax Event

The tax efficiency you build during accumulation can be reversed at transfer if the legacy architecture is not coordinated with it.

A $2 million traditional IRA transfers to your heirs, and is income-taxable to the beneficiary as it is distributed. The SECURE Act eliminated the stretch IRA for most non-spouse beneficiaries, compressing the distribution timeline and concentrating the tax exposure. The wealth is real; the after-tax transfer is materially lower.

A $2 million whole life death benefit transfers to your beneficiaries income-tax-free, outside of probate, without a 10-year distribution requirement. The transfer is clean. The tax event that would otherwise compress the legacy does not exist.

Both assets represent $2 million on a balance sheet. The after-tax legacy they produce is not equivalent, and the gap compounds as the asset values grow.

Treating legacy planning as a separate conversation from tax planning, as most financial plans do, is the most consequential coordination failure in a high-net-worth financial structure.

The final tax event on your wealth is determined by the transfer architecture, not by the account-level optimizations made during accumulation. Those optimizations matter. They are not sufficient.

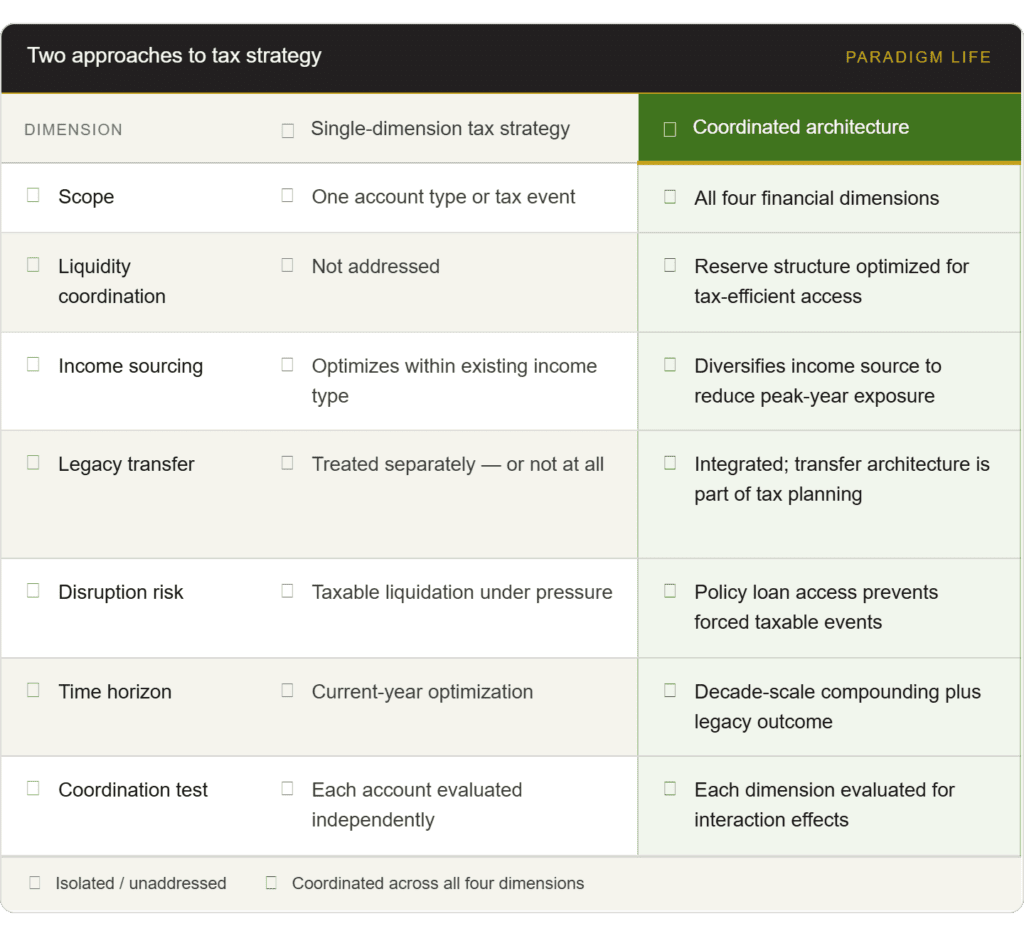

Comparison — Single-Dimension vs. Coordinated Tax Strategy

This table is a framework comparison. The right architecture is specific to your situation, income structure, asset composition, timeline, and legacy objectives. What it is not is a product recommendation.

The 401(k) Rollover Decision — A Case for Why Coordination Matters

The 401(k) rollover is one of the highest-search-volume tax decisions a high earner faces, and it is one of the most commonly under-coordinated.

When a business owner exits a company, changes employment structures, or approaches the distribution window, the question of where the 401(k) balance goes appears on the surface to be a product selection: Traditional IRA, Roth IRA, or leave it in place.

The advice industry treats it this way. The decision is more consequential than that framing suggests.

Traditional IRA rollover: Defers the tax event. Growth continues tax-deferred. Required minimum distributions begin at 73, forcing taxable income in years when you may not need it.

Beneficiaries receive income-taxable distributions, compressed into 10 years under current law for most non-spouse heirs.

Roth conversion: Triggers a current-year tax event on the converted amount. Future growth and qualified distributions are tax-free. No required minimum distributions. Beneficiaries receive tax-free distributions.

The math depends entirely on the gap between your current bracket and your expected future bracket, and on whether you have the liquidity to pay the conversion tax without liquidating other assets or compressing your reserve.

Whole life policy as a parallel structure: Does not receive rollover funds directly; there is no IRS-qualified rollover pathway into a life insurance contract. But a properly structured policy, funded alongside a retirement account portfolio, creates a tax-free income source in retirement (via policy loans).

It eliminates the liquidity pressure that often forces suboptimal rollover timing, and provides a death benefit that transfers income-tax-free outside the 10-year distribution window that applies to inherited IRAs.

The coordination question: The rollover destination that produces the best outcome is not a universal answer. It is a function of your current tax bracket, your income trajectory in retirement, your existing liquidity position, and your legacy architecture.

A reader who has funded a whole life policy has a liquidity source that does not require a taxable distribution to cover living expenses, which changes the Roth conversion math entirely, because the conversion tax can be paid from policy loan proceeds rather than from portfolio liquidation or other income.

That interaction, between the rollover decision and the existing liquidity structure, is not visible if you are evaluating the rollover as a standalone decision. It requires coordination across dimensions to see.

The right answer for your situation is specific to your structure. The right question, the one worth asking before executing any rollover decision, is: what does my full financial architecture look like after this decision, and what has changed?

The 401(k) rollover decision looks simple on the surface. The coordination question; how the rollover fits inside your full financial architecture, is where the real tax outcome is determined.

The WealthScore Assessment measures your financial architecture across all four dimensions and shows you exactly how coordinated your current structure is, including where your tax position is most exposed.

See How Your Structure Scores →

What a Coordinated Tax Strategy Actually Looks Like in Practice

The framework is useful. The mechanics are what make it real.

Income sourcing coordination in practice:

A Sovereign CEO with business distributions, investment income, and a funded whole life policy can draw from different income sources in different tax years.

In a high-income year, living expenses are covered by business distributions, which may be partially offset by business deductions.

The policy loan access is reserved for the following year when a planned capital event compresses available cash flow. The result is that neither year carries the full income burden that a single-source strategy would impose.

This is not tax avoidance. It is structural; the natural result of having multiple income types coordinated intentionally rather than operated independently.

Liquidity coordination in practice:

A Legacy Architect with significant IRA balances, real estate equity, and a funded whole life policy faces a common disruption scenario: an unexpected large expense in a year when liquidating any position would trigger a significant tax event. The IRA distribution is ordinary income. The real estate sale is a capital gain plus depreciation recapture.

The policy loan is neither. The policy loan covers the gap. The IRA stays in place. The real estate stays in place. The compounding on both continues. The tax event that would have occurred, and that would have taken a meaningful percentage of the distribution off the top, does not happen.

A reserve too thin to perform this function forces the liquidation. The tax event is not optional; it is the only available path. This is the coordination failure that a funded Certainty layer prevents.

Legacy transfer coordination in practice:

A client with $4 million in retirement accounts and $2 million in whole life death benefit does not have $6 million in equivalent legacy assets.

They have $4 million in income-taxable assets that will be distributed to beneficiaries over 10 years under current law, and $2 million in income-tax-free assets that transfer immediately and cleanly.

The after-tax legacy from the retirement accounts depends on the beneficiary’s tax bracket over the distribution window, and that bracket may be higher than expected if the beneficiary is in peak earning years.

A legacy architecture that recognizes this distinction, and coordinates the accumulation strategy around maximizing the after-tax transfer, not just the gross balance, produces materially different outcomes over time.

The difference is not a matter of which account earned higher returns. It is a matter of which structure was designed to transfer efficiently.

The integration test:

Apply this question to any tax advice you receive: does this recommendation coordinate with your liquidity structure, your income sourcing, and your legacy transfer architecture?

If the answer is “I don’t know” or “that’s a separate conversation,” the advice is single-dimension. It may still be correct within its scope. It is not complete.

Why This Gap Is Getting Wider — Not Smaller

A decade ago, a high earner with a 401(k), a taxable brokerage account, and a primary residence faced a manageable set of tax decisions. The product-by-product advice model was adequate for that level of complexity.

The portfolio of a Sovereign CEO or Legacy Architect today looks different.

Business equity, real estate positions, deferred compensation arrangements, equity compensation, retirement accounts at multiple former employers, charitable giving vehicles, trust structures, life insurance policies; each of these carries its own tax treatment, its own interaction effects with the others, and its own timeline for when the tax event actually occurs.

The financial services industry’s advice model has not kept pace with that complexity. Tax advice still comes primarily from CPAs focused on the current filing year. Investment advice comes from advisors focused on portfolio performance.

Protection and legacy advice comes from insurance professionals. Each advisor optimizes their dimension. Nobody coordinates across all of them simultaneously.

The gap between what each individual optimization produces and what a coordinated architecture produces is not visible in any single year’s tax return.

It accumulates over decades, in deferred tax events that arrive at inopportune moments, in legacy transfers that deliver less than the balance sheet suggested, in liquidity crises that force taxable liquidations at the worst possible time.

The high earners building genuinely durable wealth are the ones who recognized that optimization by dimension is not the same as a coordinated system, and who built the architecture to match.

The Foundation Question

You did not read this far because you needed a list of tax tools. You already have those. You read this far because something in your existing structure does not quite add up; the individual optimizations are in place, and the systemic outcome is still not what you expected.

That gap is real. And it is not closed by adding another account type or executing another conversion. It is closed by stepping back from the instrument-level decisions and asking what the whole system is designed to do, and whether the pieces you have, actually coordinate to do it.

The WealthScore Assessment measures your financial architecture across the Certainty, Cash Flow, Tax, and Legacy dimensions. It shows you which layers are in place, where the coordination gaps are, and in what order they need to be addressed. Free. No sales call required.

Ready to move from diagnosis to a concrete action plan? Schedule a Strategy Session with a Paradigm Life Wealth Strategist →