Best Retirement Plans for Financial Independence: Rethinking Your Approach

When it comes to planning for retirement, the landscape has evolved beyond traditional methods like a 401(k) retirement plan or an IRA (Individual Retirement Account). Today, achieving financial independence—through consistent retirement income, asset protection, and long-term wealth-building—is the ultimate goal. This is possible with the right retirement plans for financial independence. By leveraging the Perpetual Wealth Strategy™, you can create a plan that not only supports you through retirement but also helps secure your legacy for future generations.

This guide will walk you through the best retirement plans for financial independence, including both traditional and alternative retirement plans like the Life Insurance Retirement Plan (LIRP), and explain how to optimize your savings, manage your investment portfolio, and ensure a financially secure future.

The Limitations of Traditional Retirement Plans

Traditional retirement plans, like the 401(k) plan and IRA, are widely used but come with limitations. These accounts often restrict access to funds, limit your contributions, and expose your retirement savings to market risks. While they offer tax advantages, they don’t always provide the flexibility needed to support long-term financial independence.

For example, a 401(k) retirement plan allows for tax-deferred contributions, but taxes are paid when you withdraw the funds—often at a higher rate than when you contributed. Similarly, a 457 retirement plan (designed for government employees) has tax benefits but imposes withdrawal restrictions and penalties for early access. These limitations can leave retirees searching for more versatile options to ensure retirement income and financial security.

Why Traditional Retirement Plans May Not Be Enough

Relying solely on market-based investments like a 401(k) or IRA leaves your retirement savings vulnerable to market volatility, inflation, and changing tax laws. While these accounts have their place, they might not provide the consistent income and flexibility required for a truly secure retirement.

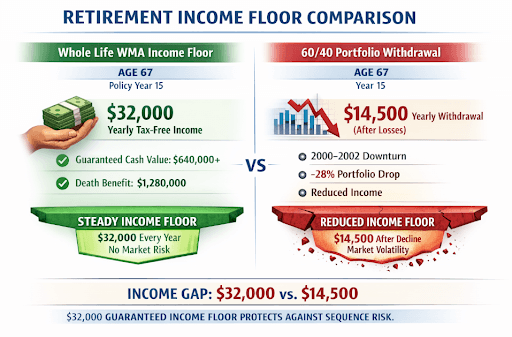

That’s why Paradigm Life recommends considering alternative retirement plans like a Life Insurance Retirement Plan (LIRP), which is built from a whole life insurance policy. A LIRP offers guaranteed growth, tax-free withdrawals, and lifetime protection—providing a level of stability and control that traditional retirement plans often lack.

Understanding Retirement Plans and The Hierarchy of Wealth™

The Hierarchy of Wealth™ is a system that organizes your assets based on risk and control. In this system, traditional retirement plans like a 401(k) plan or IRA fall into Tier 3 because they are tied to market performance and offer limited control.

To create a stable foundation for retirement income, you should consider Tier 1 assets like whole life insurance, which provide guaranteed growth, liquidity, and protection—making them ideal for long-term financial security.

Types of Retirement Plans and Their Place in The Hierarchy of Wealth™:

- 401(k) Retirement Plan: Falls into Tier 3 due to market risk and limited control. While tax-deferred contributions and employer matching can be beneficial, these plans restrict your access to funds until you reach a certain retirement age (59½), and you face penalties for early withdrawals.

- IRA (Individual Retirement Account): Similar to a 401(k), IRAs offer tax-deferred growth but are subject to contribution limits and market risks. Roth IRAs provide tax-free withdrawals but have income restrictions for contributions.

- Tax-Deferred Retirement Plans: This category includes both 401(k)s and IRAs. While tax-deferred growth is an advantage, the future tax rate on withdrawals can reduce the net benefit, especially if tax rates increase.

- Pension Funds: While becoming less common, pensions provide guaranteed income based on years of service. Pensions fall into Tier 3 due to their lack of liquidity and flexibility. Combining pensions with a whole life insurance policy offers a more flexible financial plan.

- Annuities: Annuities provide predictable income but require you to give up control of your capital. Integrating an annuity with whole life insurance (Tier 1) allows you to benefit from guaranteed income while preserving your estate for heirs.

What is a Life Insurance Retirement Plan (LIRP)?

A Life Insurance Retirement Plan (LIRP) is an alternative retirement plan that uses a whole life insurance policy to build cash value over time. And one of the best retirement plans for financial independence. This cash value grows at a guaranteed rate, and you can access it tax-free, making it a flexible, secure way to supplement traditional retirement plans like a 401(k) or IRA.

The LIRP provides multiple advantages over traditional plans:

- Guaranteed growth: Your cash value grows at a steady rate, regardless of market conditions. Many LIRPs also pay dividends, which can further boost your savings.

- Tax-free withdrawals: Unlike a 401(k) or IRA, you can access the cash value of a LIRP tax-free, giving you more flexibility during retirement.

- No contribution limits: LIRPs have no cap on contributions, making them ideal for high-income earners looking to save beyond the limits of traditional tax-deferred retirement plans.

How to Plan for Financial Independence

Achieving financial independence goes beyond contributing to a qualified retirement plan. Here’s a strategic approach, based on the Perpetual Wealth Strategy™, to ensure your financial future:

1. Assess Your Cash Flow and Assets

Rather than focusing solely on retirement savings, prioritize building positive cash flow now. Your ability to generate consistent income today is key to long-term financial independence. Regularly evaluate your assets, including traditional investments and whole life insurance, to ensure they align with your goals.

Use a retirement planning calculator to estimate how much you’ll need to maintain your desired standard of living, but remember that focusing on cash flow is crucial.

2. Maximize Contributions to the Right Plans

For those contributing to a 401(k), take advantage of employer matching. Once you’ve maximized that, consider contributing to an alternative retirement plan like a LIRP or whole life insurance policy. These plans provide flexibility and protection that traditional qualified retirement plans cannot match.

3. Diversify Beyond Market-Based Investments

Diversification goes beyond just mixing stocks and bonds. To protect your wealth from market volatility, incorporate non-correlated assets like whole life insurance. This is often referred to as the Volatility Buffer strategy, as it protects your retirement savings during market downturns, allowing riskier investments time to recover.

4. Strategize Withdrawals for Stability

How you withdraw your funds in retirement is just as important as how you save. Using the Hierarchy of Wealth™, prioritize withdrawals from market-based assets first, and rely on your whole life insurance (Tier 1 assets) during down markets to avoid selling investments at a loss.

5. Consider Early Retirement or Flexible Work Options

If you’re planning for early retirement, consider maintaining flexibility by working part-time as a consultant or freelancer. This additional income can delay the need to access your retirement savings and provide more financial security.

Beyond Retirement: Securing Your Legacy

The Perpetual Wealth Strategy™ is not just about retirement; it’s about building financial security for future generations. With tools like whole life insurance, you can optimize your assets in retirement and still leave a guaranteed, tax-efficient inheritance through the policy’s death benefit.

Using the Family Bank Strategy, you can pass down financial knowledge and create a self-sustaining system that helps your family grow and protect wealth for generations. By leveraging the cash value and death benefit of your whole life insurance policy, you ensure that your financial legacy is both preserved and accessible when needed.

FAQs: Retirement Plans for Financial Independence

What is a qualified retirement plan?

A qualified retirement plan, such as a 401(k) or pension, meets IRS guidelines for tax benefits. These plans allow for tax-deferred growth, but they often limit contributions and impose penalties for early withdrawals.

What is a 401(k) retirement plan?

A 401(k) is an employer-sponsored retirement plan that allows for tax-deferred contributions, often matched by employers. While beneficial, it ties your savings to market performance and restricts access until a certain retirement age.

How does a Life Insurance Retirement Plan (LIRP) compare to a 401(k)?

While a 401(k) grows tax-deferred, it is tied to the stock market and subject to tax upon withdrawal. A LIRP offers guaranteed growth, tax-free access, and more flexibility, making it a powerful supplement to traditional retirement accounts.

Why is expected income a large factor in choosing a retirement plan?

The amount of income you expect in retirement affects which plan is best for you. If you anticipate high income, a LIRP can help you save beyond the contribution limits of a 401(k) or IRA, while providing tax-free access to your savings.

While traditional retirement plans like 401(k)s and IRAs can be part of a comprehensive financial strategy, they shouldn’t be your only option. By integrating a Life Insurance Retirement Plan (LIRP) and following the Perpetual Wealth Strategy™, you can create a system that ensures financial independence, consistent retirement income, and a lasting legacy for future generations.

Take a proactive approach to your financial future by diversifying your assets with retirement plans for financial independence. Focus on cash flow and build a wealth strategy that goes beyond the limitations of conventional retirement plans.