Many people fear retirement because traditional planning leaves them uncertain and unprepared. At Paradigm Life, we reframe retirement as a phase of freedom and purpose using the Perpetual Wealth Strategy™. By focusing on cash flow, protection, and confidence—not just accumulation—you gain clarity and control. It’s not about making your money last, but about making your life better.

Whole Life Insurance: The Bedrock of Predictable Wealth

Whole life insurance is a foundational financial asset, offering stability, protection, and long-term value. As a cornerstone of the Perpetual Wealth Strategy™, it provides consistent growth without relying on market performance.

Key Features of Whole Life Insurance:

- Guarantees: Guaranteed cash value growth and a permanent death benefit.

- Non-market correlation: Immune to stock market volatility and economic swings.

- Lifetime coverage: Protection lasts your entire life as long as premiums are paid.

- Tax efficiency: Access your cash value tax-efficiently through policy loans.

Whole Life as a Tier 1 Asset in the Hierarchy of Wealth™:

- Prioritized for its liquidity, safety, and control.

- Provides immediate access to capital without interrupting growth.

- Offers a stable financial base to support more complex strategies.

How Mutual Insurance Companies Ensure Stable Performance:

- Owned by policyholders, not shareholders—profits are returned via dividends.

- Long history of consistent dividend payments—even during downturns.

- Financially conservative and built for long-term reliability.

Long-Term Value and Control vs. Market Volatility:

- Whole life insurance provides predictable growth and flexible access.

- Unlike market-based assets, it doesn’t fluctuate with economic conditions.

- Helps maintain control over your financial strategy across all phases of life.

Creating Flexible Access: Unlocking the Policy’s Living Value

One of the most powerful advantages of whole life insurance is its ability to offer more than just future protection—it provides strategic access to cash value while you’re alive. This living benefit transforms your policy from a passive financial product into an active tool for cash flow, liquidity, and long-term wealth strategy.

How Policy Loans Work

With whole life insurance, you don’t need to surrender your policy to access funds. Instead, you can borrow against your policy’s cash value:

- The insurance company uses your cash value as collateral.

- You receive funds quickly—without credit checks or lengthy approval processes.

- There’s no obligation to repay on a fixed schedule, though interest accrues.

Benefits of Uninterrupted Compounding

When you use a policy loan, the cash value inside your whole life insurance policy continues to grow as if you never touched it. This means:

- Your compounding growth remains uninterrupted.

- Dividends (when paid) and guaranteed interest keep building your wealth.

- You maintain both the asset and the access—simultaneously.

Strategic Use for Life’s Big Moments

The living value of whole life insurance isn’t just for emergencies. It’s a powerful tool for:

- Covering education expenses

- Funding a home renovation or investment

- Managing healthcare costs

- Supplementing retirement income

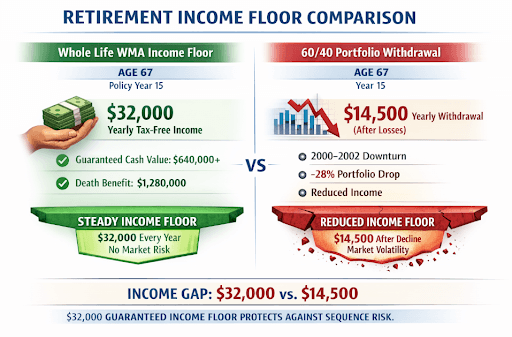

The Volatility Buffer: Income Protection in Down Markets

One of the most overlooked threats in retirement isn’t just market losses—it’s when those losses happen. This is known as sequence of returns risk, and it can quickly derail even the most carefully built retirement plans. Fortunately, whole life insurance provides a built-in solution: the Volatility Buffer Strategy. This strategy leverages your policy’s cash value to help protect your income when the market dips—keeping your lifestyle intact while your investments recover.

Understanding Sequence of Returns Risk

In retirement, you’re no longer just growing wealth—you’re spending it. If you withdraw funds during a market downturn, you may be locking in losses and reducing the long-term sustainability of your portfolio.

Why timing matters:

- Early losses during withdrawal years compound the damage.

- Market recovery becomes harder when asset values are already depleted.

- You may be forced to reduce your lifestyle or risk running out of money.

How Whole Life Insurance Creates a Volatility Buffer

With whole life insurance, your policy’s cash value grows independently of the stock market. During a downturn, you can draw from this cash value instead of your market-based accounts.

Here’s how it protects your income:

- Maintains cash flow during down markets

- Buys time for your investments to rebound

- Avoids selling at a loss during critical years

- Keeps your retirement strategy on track without lifestyle disruption

Case Example: Protecting an IRA with the Volatility Buffer

Imagine you’re retired with both an IRA and a whole life insurance policy. The market dips 15%, but instead of withdrawing from your IRA—locking in those losses—you take a tax-efficient loan from your policy’s cash value. Your lifestyle remains uninterrupted, and your IRA gets time to recover.

Outcome:

- You preserve long-term growth potential in your investment accounts.

- Your overall retirement income plan stays intact.

- You avoid taxes and penalties that could arise from premature or poorly timed withdrawals.

The Strategic Advantage

The Volatility Buffer Strategy is not just about avoiding losses—it’s about creating financial agility. Whole life insurance offers:

- Predictable access to capital

- No correlation to market volatility

- Tax-efficient income alternatives

- Enhanced longevity of your retirement assets

The Covered Asset Strategy: Optimizing Retirement Income

For many retirees, the challenge isn’t just creating income—it’s doing so with certainty and flexibility while still leaving a legacy. That’s where the Covered Asset Strategy comes in. By combining annuitized income with the guarantees of whole life insurance, this approach helps maximize your spendable income during retirement while ensuring your heirs receive what you intended to leave behind.

What Is the Covered Asset Strategy?

The Covered Asset Strategy is a retirement income solution that lets you enjoy higher, guaranteed income by converting a portion of your assets into a lifetime income stream (annuitization). Then, you use the death benefit from a whole life insurance policy to replace the value of those annuitized assets—effectively “covering” them for your heirs.

Step-by-Step Breakdown

Here’s how this strategic combination works:

1. Annuitize a portion of your assets

- Receive a guaranteed income stream for life (or for a set period)

- Payments are typically higher than traditional withdrawal methods

2. Use whole life insurance to protect your estate

- A properly structured whole life insurance policy provides a guaranteed death benefit

- That death benefit replaces the capital used for annuitization upon your passing

3. Result: You optimize both

- Spendable income during retirement

- Guaranteed legacy for your beneficiaries

Why This Strategy Works So Well

This strategy delivers benefits that traditional retirement approaches often miss. By combining the certainty of annuitized income with the protection of whole life insurance, retirees gain confidence to enjoy their wealth now while safeguarding their legacy. The Covered Asset Strategy aligns perfectly with the Perpetual Wealth Strategy™, offering a holistic financial solution that supports both lifestyle and long-term goals.

- Maximized retirement income: Annuitization provides higher payouts than standard drawdown strategies like the 4% rule. Instead of worrying about whether your portfolio will last, you receive consistent, guaranteed income for life, regardless of market conditions. This transforms your assets into a personal pension, delivering stability during your retirement years.

- Legacy preservation: Whole life insurance ensures that heirs are not left out of the picture—even if the annuitized assets are spent down. The guaranteed death benefit from your policy steps in to restore your estate’s value, providing peace of mind for your family. This approach eliminates the tradeoff between enjoying your wealth and leaving a meaningful inheritance.

- Flexibility in other assets: By covering your legacy goals with life insurance, you can use other assets more freely—whether for travel, gifting, or opportunity investing. Without the pressure to “save just in case,” you gain permission to fully enjoy the fruits of your labor. You can accelerate the use of personal capital, unlock equity, or rebalance portfolios without fear of diminishing your estate.

- Emotional and financial confidence: Knowing both your lifestyle and legacy are secured allows you to retire with clarity and peace of mind. The Covered Asset Strategy removes the uncertainty of market dependence and estate erosion. It empowers you to act with intention, guided by principles rather than fear.

Ideal For Strategic Retirement Planning

The Covered Asset Strategy is ideal for individuals who want steady, guaranteed income throughout retirement without sacrificing their legacy. It’s perfect for those who prefer certainty over market risk, using reliable tools like whole life insurance and annuities instead of speculative investments. This strategy allows you to enjoy your money now while still protecting what you leave behind, thanks to the guaranteed death benefit of a whole life policy.

Beyond the Buzzwords: Reframing What Whole Life Is (and Isn’t)

Whole life insurance often gets misunderstood—reduced to catchy phrases or lumped in with traditional investment products. At Paradigm Life, we believe it’s time to cut through the noise and provide real clarity on what whole life insurance truly offers. It’s not just insurance, and it’s not just another way to invest. It’s a powerful financial system—designed for control, liquidity, and long-term strategy.

Common Misconceptions—Cleared Up

Let’s break down a few of the most common misunderstandings about whole life insurance:

- “It’s just life insurance.”

Actually, a properly structured whole life policy is a living financial tool, not just a death benefit. It offers cash value growth, liquidity, and tax-efficient access while you’re alive. - “It’s just another investment.”

Whole life isn’t meant to compete with your market portfolio. It’s about predictability and guaranteed growth, not market speculation. It complements risk-based assets by adding certainty and control. - “It’s about becoming your own bank.”

While this phrase is popular, we reframe it for clarity: you’re creating a personalized liquidity system, backed by cash value you control—not a literal bank. The point isn’t to replace banks—it’s to reduce dependence on them.

Whole Life Insurance Is a System, Not a Product

Rather than viewing whole life insurance as a single product, think of it as part of a holistic financial system. Here’s what it brings to the table:

- Control: You choose when and how to access your policy’s cash value. There are no restrictions like age limits or penalties.

- Liquidity: Your money is available through policy loans—quick, tax-efficient, and without interrupting growth.

- Intention: You can use whole life insurance to fund family needs, business opportunities, or lifestyle expenses with purpose—not panic.

Whole Life Works With, Not Instead Of, Other Assets

Whole life insurance plays a supporting role in a diversified strategy. It’s not here to replace your investments—but to strengthen your foundation.

- In the Hierarchy of Wealth™, it sits at Tier 1: safe, liquid, and under your control.

- It buffers risk, balances volatility, and ensures cash flow when markets dip.

- It complements IRAs, 401(k)s, and real estate by providing stability.

FAQs

Is this only for high-net-worth individuals?

Not at all. Whole life insurance is highly customizable and can be tailored to suit a wide range of financial situations. Whether you’re building your foundation or managing a complex estate, the strategy works because it’s based on principles of cash flow, control, and protection—not just asset size.

How does this integrate with my existing retirement accounts?

Seamlessly. Whole life insurance complements traditional retirement accounts like 401(k)s, IRAs, and brokerage portfolios. It offers a non-market-correlated asset that adds stability, liquidity, and flexibility—especially useful during down markets or when managing taxable distributions.

What happens if I never repay my policy loan?

No penalties, no panic. Policy loans are optional to repay. If unpaid, the loan amount (plus interest) is simply deducted from your death benefit. Your policy remains intact as long as it’s properly managed, and your heirs still receive the balance of the benefit—tax-free in most cases.

Can I adjust how I use the cash value over time?

Yes—and that’s the beauty of it. You can use your policy’s cash value however and whenever you choose. Fund a child’s education, invest in real estate, or supplement retirement income. The flexibility allows you to align your money with your changing needs and goals.

Is there a best time to start this?

The earlier, the better. Starting sooner gives your policy more time to build cash value, grow through compounding, and become a more powerful financial asset. But it’s never too late—the strategy can be effective at any stage, especially when structured properly.

How do taxes affect this strategy?

Whole life insurance is designed to be tax-efficient. Cash value grows tax-deferred, and policy loans are typically tax-free. The death benefit is also generally income tax-free to your beneficiaries. This creates powerful advantages for both retirement income and legacy planning.

Retire with Confidence, Live with Intention

Retirement should reflect your values—not be driven by fear or uncertainty. With whole life insurance as a core component of your financial strategy, you gain the flexibility, protection, and control to live fully today while preserving your legacy for tomorrow. Integrated through the Perpetual Wealth Strategy™, this approach empowers you to create income with purpose and pass on wealth with clarity.

Now is the time to build a retirement strategy that aligns with your life. Connect with a Paradigm Life Wealth Strategist to design your personal income and legacy plan—tailored to give you confidence every step of the way.