If you were to get into a one-on-one conversation with a financial planner, it would be tempting to not overload the person with questions about what to do with your money for retirement.

If you were to get into a one-on-one conversation with a financial planner, it would be tempting to not overload the person with questions about what to do with your money for retirement.

“How do I get the most from my money?”

“How can my money last longer?”

“What is the best retirement account to use?”

These are just a few of the many questions that could be asked. Among those questions have you ever considered, “Why you should own a whole life insurance policy?” And lastly, “How does a whole life policy compare to other common retirement accounts?”

Why Use Insurance for Retirement

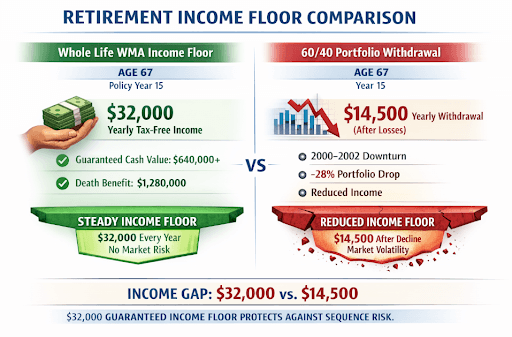

Whole Life Policy Insurance is much more than insurance with a death benefit. Unlike Term Insurance where you pay a monthly fee just to go toward a death benefit; with whole life insurance you can pay a monthly or annual premium (your choice) that is put toward both living benefits and death benefits.

Of course, different financial products meet different people’s needs, but whole life insurance is riddled with inherent benefits that make it a superior choice for retirement. Those benefits include:

- protection of your cash value

- guaranteed money growth

- tax- free dividends

- tax-free / penalty- free liquidity

- transfer of policy ownership without medical exams

These benefits allow you to secure an income during retirement without being subject to government regulation or market volatility. Mutual Insurance companies are among some of the oldest financial institutions, and have used permanent insurance to secure a person’s money and pass along wealth. Your money in an insurance policy is better protected, lasts longer, and can be better passed to your heirs, than any other retirement account.

Roth IRAs and Traditional IRAs

Roth IRAs can be opened at any age, you just have to be earning an income and you can withdraw without tax or fee penalties. However, there are income restrictions that prevent some people from participating in this product (IRA.com).

There are some stipulations: if you are younger than 59 ½ and want to access the liquidity from your Roth IRA, you are required to have it open for 5 years to avoid getting taxed and penalized. With Roth IRA you are paying into your account with after-tax money, so to access the liquidity early would cause a double taxation.

Traditional IRAs are very similar to Roth IRAs with some exceptions. Those exceptions being that the growth is tax deferred, not tax free, and the age at which you can start receiving payment is 70 ½ .

Accessing liquidity early for both Roth and Traditional IRAs is possible, but with heavy tax consequences that can be cumbersome and exhausting to work around. (H&R Block)

401(k)s

It’s startling how much attention this retirement account gets, considering the only control in which the owner has over their 401(k) is how much money they contribute. 401(k)s are volatile, come with penalties if accessed earlier than 59 ½, and you are limited to how much you can contribute. Another restriction with 401(k)s is that a person’s employer chooses the acceptable investment vehicles for this account. With this plan, you’ll likely have a meager retirement, but you will definitely not have access to any liquidity.

Inflation and Tax

The 401k and the IRAs (Roth included) all come with too many rules and regulations. Knowing our government and economy, anyone could tell you that rules, regulations and tax brackets are subject to change. Also, inflation needs to be considered. Financial advisors really don’t talk about how much value your money will have in 20 or 30 years, then throw tax on top of that when you are ready to retire – you’ll be asking yourself where your retirement went.

Life Insurance Protects You during Retirement

Permanent insurance avoids the pitfalls that other retirement accounts are subject to. Whole Life Insurance is nominally regulated by state law, and not subject to most federal mandates. Your Life Insurance policy always grows tax deferred, and careful planning ensures that access to your cash value remains tax free.

To learn more about the living benefits of Whole Life Insurance and why it’s smart to use it for retirement, visit our premier elearning course Infinite 101.

Read: Infinite Wealth: A Different Kind of Retirement

Listen: The Wealth Standard Radio Show – Human Life vs. Capital Life