The effects of COVID-19 on life insurance companies and their policyholders is the number one question our Wealth Strategists have been addressing over the past several months. Our most common questions about COVID-19 affecting life insurance include: How does COVID-19 affect my whole life insurance policy? Do mutual life insurance companies have the funds to pay out on policies? What if I can’t pay my premium? If I don’t already have insurance, is it too late to get a whole life policy? How will I take a medical exam? What does the effect of the stock market mean for my potential premium and dividend payouts?

The landscape of life insurance among COVID-19 is rapidly changing, dependent upon the insurance company. It’s easy to become misinformed when you don’t understand the nature of mutual insurance companies or the history of pandemics and life insurance and the various types of insurance policies offered. To help you navigate these uncertain times, let’s break down everything you need to know about COVID-19 and life insurance.

The Benefits of Life Insurance in a Pandemic Like COVID-19

Most people know that when their lives are at risk, having life insurance helps protect their loved ones. But having the right kind of life insurance offers so many benefits beyond a lump-sum death benefit payout to beneficiaries. Whole life insurance has multiple living benefits and can be a very beneficial life insurance for COVID-19.

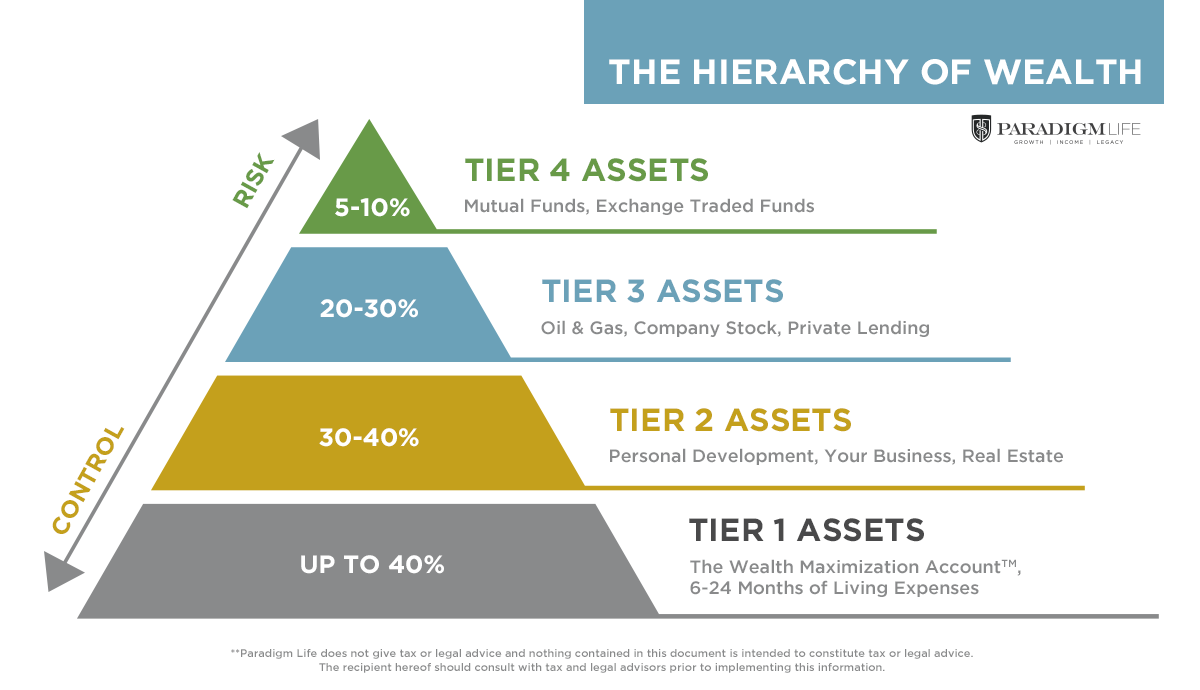

At Paradigm Life, we use The Hierarchy of Wealth to teach our clients how to build a solid financial foundation. This kind of foundation will protect your wealth during pandemics such as COVID-19.

We recommend placing 6-24 months of living expenses in Tier 1 assets. Hold on to these assets for financial emergencies like the market effects of COVID-19, job loss, unexpected medical bills, etc. You could keep 6-24 months of living expenses in a savings account, or you could stash it in an asset like whole life insurance. Whole life insurance is advantageous because it grows cash value and pays out dividends.

We refer to whole life insurance as the “AND Asset”. It serves so many functions you can benefit from while you’re alive, and you don’t have to choose one benefit over the other. It maximizes your cash flow, especially in times of economic crisis. Let’s break down the benefits of whole life insurance and show you how current clients are utilizing these benefits during COVID-19.

How Whole Life Insurance Keeps You Protected for COVID-19

Whole life insurance functions as your emergency savings.

COVID-19 has had a massive impact on our economy and threatens many people’s job security. Money in a product backed by a mutual life insurance company, rather than invested in the market, helps you sleep better at night. You can rest easy knowing you’re safeguarded against market fluctuations.

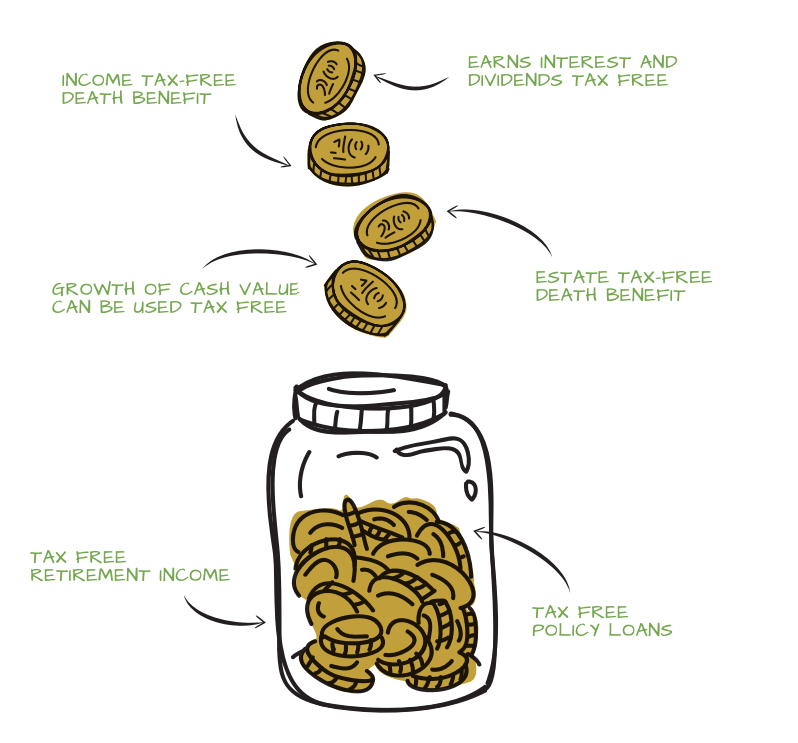

Whole life insurance offers multiple tax advantages.

Stimulus bills like the CARES Act and other financial stimulus packages being debated by congress will eventually need to be paid for. It is highly likely tax rates will increase in the coming years to cover stimulus bill costs. Having a tax shelter in place, like a whole life insurance policy, keeps your wealth protected. Here are six typical tax advantages of whole life insurance*:

*Speak with your tax advisor for details. Tax laws vary by state and policy structure.

Whole life insurance lets you be your own bank.

Arguably the greatest living benefit of whole life insurance is the policy loan feature. This guaranteed option allows you to borrow from the cash value of your policy, up to the maximum loan value. Your insurance company will charge interest on your loan, typically lower than bank or creditor interest rates. You can choose the rate at which you pay back your loan.

You don’t need an application or credit approval to use the policy loan feature, and you don’t need to put up your other assets as collateral. The collateral is the death benefit of your policy. You can use your policy loan for anything you need, and you can take out multiple policy loans over your lifetime. It’s often the most cost-effective way to fund business expenses, college tuition, real estate, and other major purchases.

COVID-19 and Mutual Life Insurance Companies

The mutual insurance companies we work with at Paradigm Life have paid out death benefits and dividends consistently for over 200 years. They have successfully weathered financial events, including the Great Depression and Great Recession, and pandemics like Yellow Fever, Spanish Flu, SARS, Swine Flu, and MERS, not to mention WWI, WWII, and 9/11.

To put COVID-19 into perspective from an insurance point of view, the Spanish Flu killed between 40 and 50 million people between 1918 and 1919. The age group hit hardest by the Spanish Flu wasn’t the elderly, it was young adults. Insurance companies had to pay out death benefits on younger policyholders who hadn’t been contributing premium payments for decades like their elderly counterparts. And yet, mutual insurance companies thrived. Not only did they pay out death benefits, they paid dividends.

COVID-19 is covered under your whole life insurance policy. Once you have a policy in place, your mutual insurance company cannot make changes to it. You’re locked in at your premium, guaranteed your death benefit (provided a fraudulent claim isn’t filed based on falsified information), and guaranteed to be able to take out policy loans on your accumulated cash value.

While some dividend rates have dropped in light of COVID-19’s effect on the market, you’ll likely see rebounds over the coming months. Remember, mutual insurance companies have historically paid out dividends for over 200 years. The exact amount of your dividend depends on the company who insures you. All of the mutual companies we work with are experts at assessing and pricing risk. It is their responsibility to put you, the policyholder, first. By funding a policy, you’re in a position to reap reliable financial benefits that stock market investors will never enjoy.

How Does COVID-19 Affect Your Life Insurance? FAQs

What if I can’t pay my insurance premium?

You may have recently been laid off, furloughed, or under a stay-at-home order but unable to work from home. Mutual insurance companies understand this, and some are offering extensions on premium payments. Additionally, some states are implementing regulations specific to COVID-19 to help protect your policy. To find out if your state or insurance company offers these types of assistance, contact your mutual insurance company directly or call your Paradigm Life Wealth Strategist. Once a policy lapses, it can be incredibly difficult or impossible to reinstate. If you’re experiencing financial uncertainty, it’s imperative that you speak with your Wealth Strategist or insurance company as soon as possible.

If your mutual insurance company isn’t currently offering an extension or grace period on your premium, you still have plenty of options. Insurance policies are built to weather tough times. If you’re concerned about paying your premium on time, it’s possible to adjust your payment schedule, use your accumulated cash value to pay your premium, or take out a policy loan to cover your premium. The right answer for you depends on your financial needs and goals, and your insurance carrier.  to go over all the options available to you.

to go over all the options available to you.

If I’m currently uninsured, is it too late to open a policy?

It’s not too late to protect yourself with a whole life insurance policy. But remember, the sooner you act, the sooner you’re protected. Don’t let financial uncertainty deter you from creating a solid financial foundation for you and your family. Regardless of your situation, we can find an insurance product to meet your needs, even if that means opting for a term life insurance policy you can convert to whole life at a later date, or setting up an annuity if you’re over 55.

Underwriting guidelines have become stricter among some insurance carriers. Namely, carriers may want to know if you’ve been out of the country recently, if you plan to travel outside the country, if you’ve been in contact with someone with COVID-19, or if you yourself have been diagnosed with COVID-19. None of this will solely disqualify you from obtaining life insurance indefinitely; most carriers will require a 30-day waiting period to ensure you’re not showing signs of COVID-19.

Your policy application could be delayed if you’ve been hospitalized for any reason. It’s not grounds for disqualification, but you will need additional documents from your doctor to explain your hospital stay and verify you’re in good health.

What if I need a medical exam?

Most mutual insurance companies will require you to take a medical exam when applying for a life insurance policy. There are exceptions to this rule and they depend on the amount of life insurance you’re applying for, as well as your overall health and age. A Wealth Strategist will guide you in the right direction to find the insurance product best suited to your needs.

If you do, in fact, require a medical exam before your insurance application can be approved, you do not have to go to a doctor’s office or hospital to take your exam. The paramedical team we work with, ExamOne, can arrange to come to your home and you can take your medical exam there. ExamOne is taking extra social distancing precautions right now, consistent with CDC COVID-19 recommendations, to keep clients safe.

Most insurance companies will give you 120 days to complete your exam. So if you’re unable to schedule or uncomfortable having someone in your home, you have options. Keep in mind the longer you postpone your medical exam, the longer it will take to receive insurance coverage, but the 120-day grace period is there if you need it. If you’ve already applied for insurance but still haven’t taken your exam, contact your insurance company or agent to make sure your application doesn’t lapse.

If you have questions about your current insurance products or are looking for a proven way to protect yourself and your loved ones financially, we’re here for you.

At Paradigm Life we can customize a policy to fit your financial situation. Our expert Wealth Strategists are available to answer your questions and show you customized illustrations, outlining an individual plan of action to help you achieve your goals. , no strings attached.

Act now and start building a financial foundation that you can rely on for a lifetime.

FAQ

Q: How has COVID-19 impacted life insurance policies?

A: COVID-19 has brought about new considerations for life insurance, including policy coverage related to the pandemic and the handling of claims arising due to COVID-19.

Q: Can life insurance policies provide financial relief during the pandemic?

A: Many life insurance policies offer options that can aid in financial relief during challenging times like the COVID-19 pandemic, including flexible premium payments or accessing cash value.

Q: Are life insurance companies stable during the COVID-19 pandemic?

A: The stability of life insurance companies during COVID-19 varies, but many mutual life insurance companies have shown resilience, maintaining their long-term financial commitments to policyholders.