Generational Wealth Explained

Imagine the life-changing impact of inheriting a small fortune—or better yet, creating your own wealth to pass down to future generations. For many, building generational wealth is the ultimate expression of a life well-lived. It’s not just about leaving behind money or property; it’s about providing your loved ones with financial security, knowledge, and opportunities to thrive long after you’re gone.

At Paradigm Life, we believe in turning this vision into reality through the Perpetual Wealth Strategy™. This holistic approach empowers you to build and protect wealth while creating a legacy of financial literacy and stability for future generations.

But what exactly is generational wealth, and how can the Perpetual Wealth Strategy™ help you establish a lasting legacy? Let’s explore the steps to make it happen.

What is Generational Wealth?

Whether you have been on the giving end or the receiving end of generational wealth, you know that it’s more than birthday money, a check for mowing the lawn, or a handout. It represents decades of hard work and financial education in the form of assets passed to the next generation. It carries a piece of your heritage, helps tell your family story, and perpetuates the values you hold dear.

Examples of generational wealth could include a parent teaching their child about budgeting. It could be helping your teenager buy a car or make a down payment on a home later in life. This kind of wealth transfer isn’t limited to parents and children. It could take the form of financial advice from a successful uncle. Or grandparents contributing to pay a grandchild’s college tuition. Even if you don’t have children of your own, you can still be the successful aunt who leaves your legacy to lucky nieces and nephews!

In fact, the idea of distributing generational wealth doesn’t even have to apply to family. Many wealthy individuals choose to distribute some of their fortune to charities, foundations, and causes they value. Regardless of what you do with your wealth, ensure your plans enable you to create a legacy you would be proud of. Otherwise, your hard earned money will likely end up in the government’s hands, and there’s no legacy in that!

WATCH: How to Build a Legacy of Wealth at Any Age

14 Ways to Build Generational Wealth

Here are several ideas on how to build a lifetime legacy and tips for how to ensure it lives on for generations to come:

Create an emergency fund.

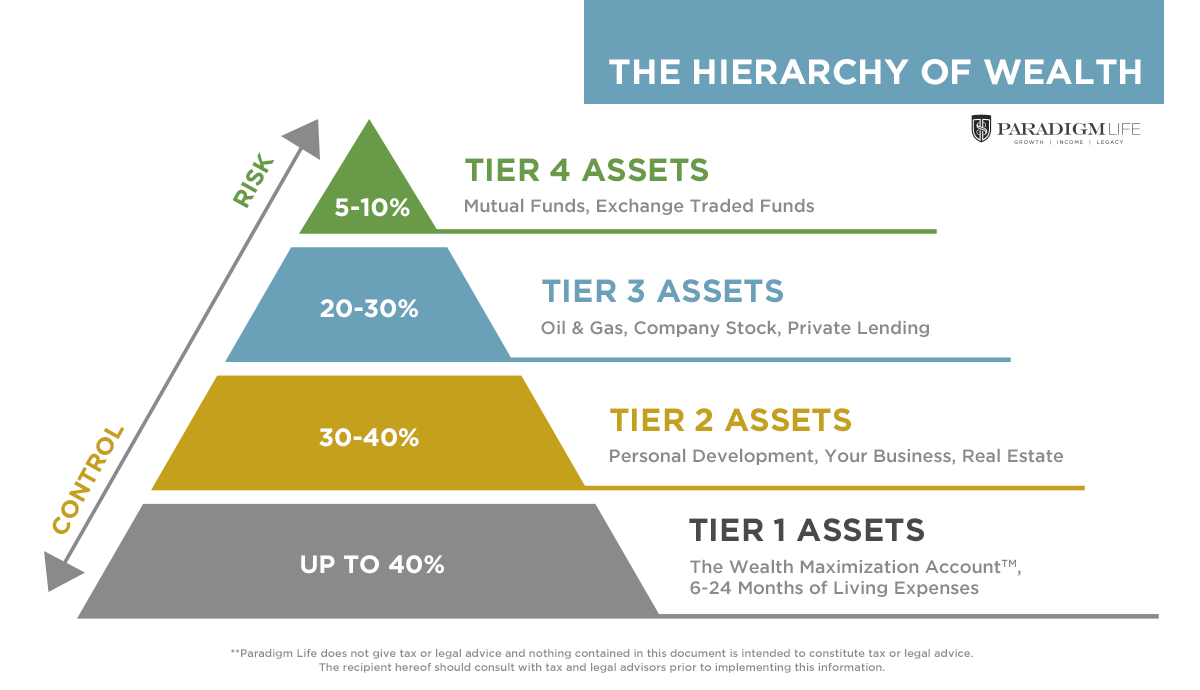

Saving money rarely makes people rich, but not having any savings puts many people in debt. It’s imperative that you create a solid financial foundation to build your generational wealth upon. The Hierarchy of Wealth illustrates this point. It shows how an emergency fund or similar account, like a Wealth Maximization Account™, offers the most financial control with the least amount of risk, allowing you to continue to build wealth even when life takes a sideways turn.

Focus on Tier 1 before making other investments to prevent getting wiped out by a market downturn. Aim to put 40% of your expendable income here. It could be in the form of at least six month’s living expenses in savings or invested in whole life insurance for faster growth. If a market investment tanks, you lose your job, or you have a major unexpected expense, you’ll be protected. You won’t have to turn to banks and creditors for help bailing out.

Learn how to budget.

Rather than subscribing to a cookie-cutter budget, find one that works with what you find the most enjoyment in. This is called “Values Based Budgeting”. No one elses budget will look exactly the same as yours, because no one else has the same goals and values as you do. Regardless of what you prioritize in your budget, be it travelling, dining, education, etc., structure it in a way that you can save and/or invest in something every month.

Earn passive income.

No matter how you budget, the amount you’re able to use to grow your legacy won’t drastically change unless you increase your income. But there are only so many hours in the day! This is why earning passive income through various financial assets is vital to growing wealth. One way or another, you need to make your money work for you.

There are a number of income producing assets you can utilize to start growing passive income. We’ve compiled a list of the nine most common here.

Know what you’re worth.

Using a tool called The Human Capital Statement, define your strengths and weaknesses. Your strengths are your assets and your weaknesses are your liabilities. Find skills and talents you can monetize and look for areas of improvement. The fact that you currently make money shows that you’re worth something. It also shows that you have the capacity to be worth more.

Invest in education.

The phrase “You have to spend money to make money” is never truer than when it comes to education. Going back to college for a second degree might not be the best use of your dollars, depending on tuition rates, but there are plenty of online courses, business conferences, webinars, and community classes you can take to expand your skills, thereby increasing your earning potential. Education may not be hard assets passed from one generation to the other, but it can pay dividends.

Paradigm Life offers a number of free educational resources to boost your financial education.

Look for opportunities.

A key component in building generational wealth is knowing a good opportunity when you see one. Educate yourself on investing and keep an eye out for investments that align with your risk tolerance and abilities. Warren Buffet made an entire career (and became one of the wealthiest men in the world) by looking for opportunities. So can you.

Recently, Paradigm Life CEO Patrick Donohoe wrote an entire bulletin on uncommon investment opportunities and how to find them. In it, he outlines 10 traits for successful investments and lists tools to help you find your investment personality. Read the full bulletin here.

Build a business.

A family business is a great tool for building a legacy and to build wealth. It also has the added benefits of allowing you to be your own boss and teach your children about ownership. Encourage them to learn the family business and prepare them to take it over someday. If your children don’t show interest in the business, you can sell the company and use the funds to distribute generational wealth in a different manner.

Buy real estate.

Whether you’re looking to grow a real estate empire to increase your passive income or to purchase a small family cabin, property is a common legacy. While single-family properties might not be as lucrative as rental properties, they do require less management and usually less upkeep. Leaving a vacation home to your heirs is more than just leaving them real estate; you’re passing down family memories for generations to come. Regardless of the property type, real estate is known to hold its value. It is widely considered a relatively safe investment to build generational wealth.

Take advantage of tax shelters.

Keep more of your hard-earned income off the government’s radar by using investment products that offer tax advantages and minimize estate taxes. Depending on your income and financial goals, you might opt for tax-deferred savings, tax-free savings, or a mix of both. The federal estate tax is significant for wealthy families if you’re not able to plan for it ahead of time.

Buy stocks.

Investing in the stock market is arguably the riskiest way to grow generational wealth. But if you’re buying stocks for grandchildren who have decades to let their money ride out the market, it can be a viable option for growth. When considering stocks and mutual funds, refer back to The Hierarchy of Wealth. Make sure you have a solid financial foundation before you take on riskier investments.

Purchase cash value whole life insurance.

Whole life insurance policies from mutually-funded insurance companies offer multiple benefits to help you build generational wealth and leave a legacy. They come with built-in tax advantages and grow cash value to be used for large purchases like business expenses, real estate, and college tuition payments. A whole life policy can function as your emergency savings and financial foundation. It also features a guaranteed death benefit to pass on to your heirs.

Prepare your heirs for inheritance.

The Rockefellers have passed down their wealth for generations by minimizing estate taxes and investing in generational wealth transfers, while the Vanderbilts have lost nearly all their fortune. The difference? The Rockefellers valued the importance of education and financial literacy from generation to generation. They prepared their children from a young age on how to use the family money for continued growth.

Statistics show that 70% of wealth is gone after the second generation and 90% after the third. Let your beneficiaries know that they will be receiving money and prepare them so they know what to do with it. “Surprise” money left to an heir rarely gets spent wisely, and if that is the case for you, building generational wealth in the first place may be in vain! Make sure that your generational wealth transfers to your heirs!

Make an estate plan.

Consult an attorney and make an estate plan to outline how you wish your wealth to be distributed. Wills are usually included as part of your estate plan, and save loved ones a lot of headaches and legal disputes down the road. Your estate plan ensures a smooth asset transition, keeping your goals in mind, distributing generational wealth to the beneficiaries and charities you choose.

Starting Now is the Way to Building Generational Wealth

It’s never too early or too late to shape the legacy you want to leave behind. Whether you’re just beginning your career or approaching retirement, generational wealth is more than just money—it’s a reflection of your values and the lasting impact you want to make on your loved ones and the causes you care about.

By starting early, you can amplify the benefits of your wealth during your lifetime. From providing financial education and tuition assistance to supporting charitable causes and funding milestones for your family, your legacy can make a difference now and for generations to come.

At Paradigm Life, we specialize in crafting personalized strategies to help you build and pass down generational wealth. Our expert Wealth Strategists will guide you through customized illustrations and actionable plans tailored to your financial goals.

Take the first step toward creating your lasting legacy. Request a free virtual consultation today—mention the Perpetual Wealth Strategy™ for insights into how we can help you achieve your vision.