In today’s unpredictable world, it’s easy to let emotions drive our financial decisions. Whether it’s fear during a market downturn or the excitement of a “can’t-miss” opportunity, many people make money moves that feel right in the moment—but don’t hold up over time. That’s why understanding the Principles of Rational Finances is so important. At Paradigm Life, we help clients implement strategies like the Perpetual Wealth Strategy™, which offers a steady path to financial control, liquidity, and guaranteed growth, even when the world feels uncertain.

By grounding your personal economy in principles—rather than emotions—you can build a financial foundation that lasts a lifetime and creates a meaningful legacy.

Principle 1: Know Where Your Money Goes

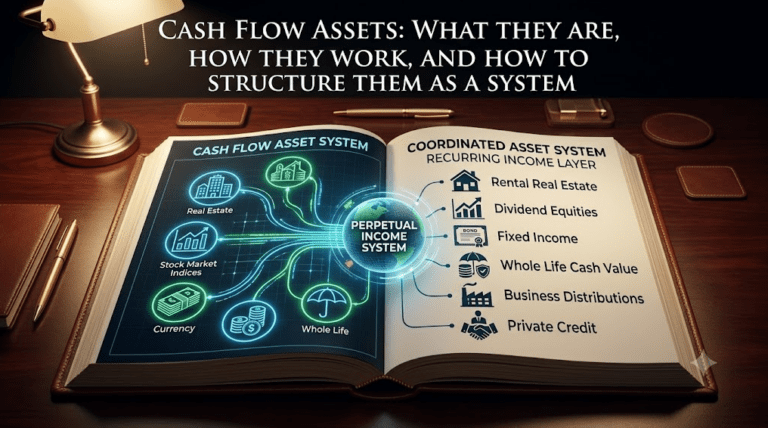

The first step in the Principles of Rational Finances is knowing where every dollar goes. If you don’t track your money, it can disappear fast—and you won’t know why. That’s why understanding your cash flow is the foundation of smart financial decisions.

Why Cash Flow Matters

Cash flow is how much money comes in and how much goes out. When you pay attention to your cash flow:

- You see where you’re overspending

- You find chances to save more

- You feel more financial control every day

Think of it like a scoreboard. When you’re keeping score, you play smarter. You make better choices with your money because you know what’s really going on.

A Smart Way to Save and Grow

At Paradigm Life, we use whole life insurance as part of a smarter savings strategy. Here’s why:

- It builds cash value over time

- That cash value is liquid—you can borrow against it when you need to

- You stay in control, and your money keeps growing, even when you use it

This means you can have a safe place for your money that earns steady growth and gives you options—without touching your emergency fund or investment accounts.

Simple First Steps:

- Track your spending for one week

- Look for things you don’t need (subscriptions, fast food, etc.)

- Set a small savings target from what you cut

- Talk to a Wealth Strategist about using whole life insurance as a cash flow tool

Principle 2: Create a Personal Wealth Strategy

A big part of the Principles of Rational Finances is having a clear path for your money. That means creating a personal wealth strategy—a plan that fits your life, your values, and your future goals.

What Is a Personal Wealth Strategy?

It’s your personal roadmap. You decide:

- Where you want to go

- What matters most to you

- How you want your money to support that

At Paradigm Life, we use the Perpetual Wealth Strategy™ to help people design financial paths that are safe, smart, and built for the long run.

How to Start Your Wealth Strategy

Don’t let it overwhelm you. Just follow these simple steps:

- Set your vision

- Think about where you want to be in 5, 10, or 20 years

- Examples: Buying a home, funding a business, or leaving a legacy for your kids

- Break it down

- Take that big vision and break it into small, doable steps

- Ask: “What do I need to do this year, this month, or this week to move forward?”

- Use tools that support you

- Whole life insurance can help fund your goals through cash value

- It gives you access to tax-advantaged, guaranteed growth—without market risk

- It also lets you use your money while it keeps growing

Why It Works

When you reverse-engineer your dreams into real actions, you stop guessing. You start making rational financial decisions that bring your goals to life.

You gain:

- Financial control

- A clear sense of direction

- Peace of mind about your future

Principle 3: Plan for Taxes—They’re a Big Deal

When thinking about money, many people forget one major thing: taxes. But if you want to follow the Principles of Rational Finances, you need to plan ahead—because taxes can take a big bite out of your future wealth.

Most People Miss This

Many savings plans—like 401(k)s or IRAs—defer taxes until later. That might sound helpful now, but it’s a gamble. You don’t know what tax rates will be in the future. They could go up—and that means you’ll owe more when it’s time to use your money.

This common mistake leaves people with less than they expected when it matters most.

The Risk of Waiting

Here’s why tax-deferred accounts can be risky:

- You can’t control future tax rates

- Withdrawals are taxed as regular income

- You might pay more in retirement than you would now

That’s why smart savers look for tax-advantaged ways to grow their money.

A Better Way: Whole Life Insurance

At Paradigm Life, we use whole life insurance as part of a tax-smart financial strategy. When structured properly, it offers:

- Guaranteed growth of your cash value

- Tax-deferred accumulation

- Tax-free access through policy loans

- A tax-free death benefit for your family

With whole life insurance, you’re not guessing what your tax bill might be later. You’re gaining financial control and long-term stability—two major parts of the Principles of Rational Finances.

Principle 4: Be Ready for the Unexpected

Life is full of surprises. Some are good. Some are not. If you want to follow the Principles of Rational Finances, you need to be ready for both.

Unexpected things happen—job loss, health problems, market crashes. You can’t control these events, but you can control how prepared you are.

Why Preparation Matters

Most people only plan for what they hope will happen. But smart money decisions include plans for what might happen.

When you’re not ready, small problems can turn into big money troubles. But with the right tools in place, you can stay strong—even during tough times.

Your Financial Safety Net

At Paradigm Life, we teach the Volatility Buffer Strategy. It’s a way to protect your future income during market downturns by using the cash value of a whole life insurance policy.

Here’s how it helps:

- When the stock market drops, don’t pull from your investments

- Instead, use the liquid cash from your policy’s cash value

- This gives your investments time to recover

- And you avoid selling at a loss or going into debt

What Makes Whole Life Insurance Powerful?

- It offers guaranteed growth year after year

- You can access the cash value anytime—no penalty or approval needed

- It provides a tax-free death benefit for your family

- It gives you true financial control in good times and bad

These benefits make whole life insurance an essential part of the Principles of Rational Finances—because it helps you plan for the known and the unknown.

FAQs About Principles of Rational Finances In an Irrational World

What are the four principles discussed in the article for rational financial management?

The four principles are gaining control over your finances, creating a deliberate financial strategy, considering future tax implications, and preparing for unexpected financial challenges. These principles provide a comprehensive approach to rational financial decision-making in a complex world.

Why is gaining control over one’s finances important?

Gaining control over finances enables individuals to have a clear understanding of their financial situation, make informed decisions, and establish a solid foundation for effective financial management. It empowers them to align their financial goals with their current resources.

How does considering future tax implications contribute to rational financial planning?

Anticipating future tax implications allows individuals to make tax-efficient financial decisions, potentially reducing their tax burden and optimizing their financial strategies. It ensures that financial plans are aligned with long-term tax goals.

Why is preparing for unexpected financial challenges a crucial aspect of rational finances?

Preparing for unexpected financial challenges ensures resilience in the face of unforeseen events such as emergencies or economic downturns. It helps individuals maintain financial stability and continue pursuing their financial goals even in uncertain times.

Take the Next Step: Build Your Perpetual Wealth Strategy™

The Principles of Rational Finances give you more than just peace of mind—they give you the tools to make smart, confident decisions in any market. At Paradigm Life, we don’t believe in guesswork or one-size-fits-all plans. We believe in proactive, principle-based strategies that put cash flow, protection, and wealth at the center of your personal economy.

The Perpetual Wealth Strategy™ is your path to financial control, guaranteed growth, and lasting legacy. And it starts with one simple step.

Connect with a Wealth Strategist today to design your custom strategy and take control of your financial future—on your terms.