Whole Life Insurance is more than just a death benefit—it’s a living, liquid asset designed to help you build lasting financial security. When properly structured, it becomes a cornerstone of the Perpetual Wealth Strategy™, offering guaranteed growth, long-term control, and tax-efficient access to capital. A key feature that enhances this strategy is the Paid-Up Additions (PUA) rider, often underutilized but incredibly powerful.

What Are Paid-Up Additions (PUAs)?

Paid-Up Additions (PUAs) are one of the most powerful and flexible features of a properly structured Whole Life Insurance policy. Simply put, PUAs are small pieces of fully paid-up additional life insurance that you can add to your base policy. Each PUA increases both your policy’s death benefit and its cash value, offering immediate and long-term financial advantages.

Unlike traditional premium payments that primarily go toward the base policy, PUAs supercharge your policy by allowing extra contributions that build equity from day one. These additions can be purchased using out-of-pocket contributions, policy dividends, or a combination of both—making them a key component of the Perpetual Wealth Strategy™ used at Paradigm Life.

Key Characteristics of PUAs:

- Fully paid: Each PUA is self-contained and requires no future premium payments.

- Cash value growth: PUAs begin compounding immediately and contribute significantly to the total cash value.

- Increased death benefit: Every PUA increases the policy’s long-term protection for your beneficiaries.

- Dividend eligible: PUAs are eligible to receive future dividends, amplifying growth even further.

By leveraging Paid-Up Additions in Whole Life Insurance, policyholders gain more control, more liquidity, and more growth—without sacrificing the guarantees and stability that make Whole Life such a unique financial asset.

Core Benefits of Whole Life Insurance

A Whole Life Insurance policy provides more than just lifelong coverage—it offers a suite of built-in benefits that serve as the foundation for long-term financial security. When enhanced by Paid-Up Additions (PUAs), these benefits become even more powerful, accelerating both protection and wealth-building potential.

Here are the core advantages of whole life insurance, all of which are strengthened with PUAs:

- Guaranteed lifetime coverage: Your policy remains in force as long as premiums are paid, providing permanent protection for your loved ones.

- Level premiums: Your base premium never increases, offering predictability and stability over time.

- Guaranteed cash value growth: Your policy accumulates cash value at a fixed rate, and PUAs amplify this compounding power.

- Tax-deferred growth: Cash value grows tax-deferred, and policy loans accessed through PUAs are generally tax-free.

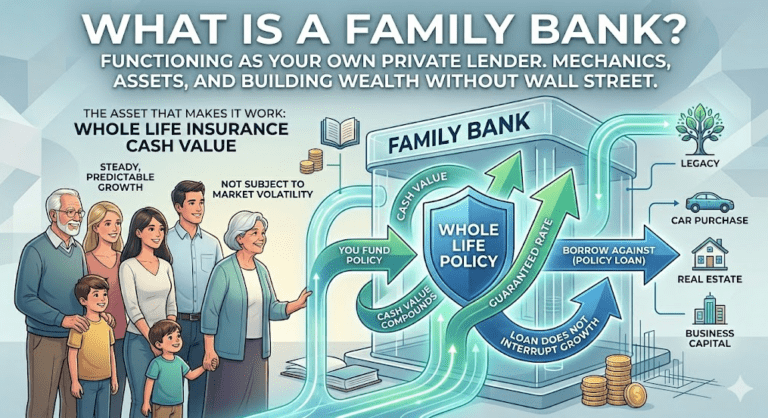

- Liquidity and control: You can access your cash value at any time for any reason—without penalties or market timing risks.

Market protection: Whole Life Insurance is not tied to market performance, making it a stable asset even in downturns. - Dividend eligibility: When issued by a mutual company, your policy can earn non-guaranteed dividends—often used to purchase PUAs for increased growth.

- Retirement income supplement: Policy loans can provide tax-advantaged income in retirement, especially when funded by PUAs that grow early and efficiently.

- Estate and legacy planning: The death benefit passes tax-free to your heirs, helping preserve generational wealth.

When you incorporate Paid-Up Additions into your Whole Life Insurance, you build upon these core strengths, turning a reliable financial product into a personalized, high-performing strategy. This is one of the foundational pillars of the Perpetual Wealth Strategy™ at Paradigm Life.

How Paid-Up Additions Work

Paid-Up Additions (PUAs) are a unique feature of Whole Life Insurance that boost both the death benefit and the living benefits—specifically, your cash value. Each PUA is a small piece of fully paid-up life insurance that’s added to your base policy, delivering immediate value and long-term growth potential.

PUAs work by enhancing your policy in two key ways:

Increase in Cash Value

Each time you purchase a Paid-Up Addition (PUA), it immediately boosts your Whole Life Insurance policy’s cash value. This added equity is available for use through tax-free policy loans, offering flexible access without interrupting growth. Over time, that value compounds with guaranteed interest and potential dividends—supporting liquidity, stability, and long-term wealth.

Boost in Death Benefit

Along with cash value, PUAs raise your overall death benefit, providing more protection for your family. These additions are fully paid up, which means no ongoing premiums are required.

Flexible Funding Options

PUAs can be funded through:

- Out-of-pocket premium contributions

- Dividends earned by your policy

- A combination of both

This flexibility makes it easy to customize and scale your policy in line with your financial goals.

Long-Term Performance

By adding PUAs regularly, your Whole Life Insurance policy can build equity faster and become a more powerful part of your overall wealth strategy. At Paradigm Life, PUAs are essential to the Perpetual Wealth Strategy™, allowing clients to access liquidity while continuing to grow wealth with control and predictability.

Strategic Uses for PUAs

Paid-Up Additions (PUAs) play a central role in enhancing the flexibility and long-term power of your Whole Life Insurance policy. By accelerating cash value growth, PUAs make it easier to access liquidity and use your policy as a financial tool—not just a safety net. When structured properly, PUAs create living benefits you can use throughout your lifetime, aligned with the Perpetual Wealth Strategy™.

- Early cash value accumulation

PUAs boost your policy’s cash value from day one, accelerating your access to living benefits. Unlike base premiums alone, PUAs allow your policy to build equity immediately, giving you usable liquidity within the first year. This early cash value can be leveraged for opportunities, emergencies, or reinvestment—without interrupting compounding growth.

- Increased loan power

As your cash value grows through PUAs, so does your borrowing capacity. You can use policy loans for:

- Business or real estate opportunities

- Emergencies and major purchases

- Supplementing retirement income

PUAs give you access to capital without interrupting the compounding growth of your policy.

- Premium offset or retirement income

Over time, PUAs and dividends can be used to:

- Offset your future premium payments

- Supplement income in retirement

- Add flexibility to your long-term financial plan

How PUAs Support the Perpetual Wealth Strategy™

Paid-Up Additions (PUAs) are a cornerstone of how Whole Life Insurance can be transformed from basic protection into a dynamic financial tool. Within the Perpetual Wealth Strategy™, PUAs provide the acceleration and flexibility needed to grow, protect, and use wealth with intention—while maintaining full control.

1.Accelerate cash value growth: PUAs supercharge your policy’s ability to build cash value, allowing you to access liquidity faster than with base premiums alone. This is essential for clients looking to put their capital to work quickly and efficiently.

2. Enable strategic policy loans: With increased cash value comes greater loan capacity.

PUAs make it easier to implement one of the key tools in the Perpetual Wealth Strategy™—using policy loans to:

- Invest in cash-flowing assets

- Fund a business

- Cover large expenses without interrupting compounding growth

3. Strengthen financial independence: PUAs give you more control over your money, bypassing banks and Wall Street. They create a reliable pool of capital you can access on your terms—no credit checks, penalties, or external approvals. This aligns directly with Paradigm Life’s philosophy of using Whole Life Insurance as a private wealth-building system. Over time, PUAs help build autonomy and long-term financial confidence, central to the Perpetual Wealth Strategy™.

4. Compound tax-advantaged wealt: Since PUAs grow tax-deferred and can be accessed tax-free through policy loans, they maximize long-term efficiency—helping you build wealth while minimizing tax drag over time. This makes them especially powerful when used to fund retirement, business ventures, or large purchases. By keeping more of what you earn compounding within your policy, PUAs support lasting, predictable growth.

Addressing Misconceptions About PUAs and Whole Life Insurance

Paid-Up Additions (PUAs) and Whole Life Insurance often carry misconceptions that can prevent individuals from exploring their full potential. At Paradigm Life, we believe it’s essential to dispel these myths so clients can make confident, informed decisions aligned with the Perpetual Wealth Strategy™.

- Misconception 1: “PUAs are too complicated”

Reality: PUAs may sound technical, but they’re actually simple to understand and implement. A PUA is just additional, fully paid-up life insurance added to your base policy—providing more cash value and death benefit from day one. Your Wealth Strategist structures them with clarity and transparency.

- Misconception 2: “PUAs make whole life insurance too expensive”

Reality: While PUAs increase the premium, they also boost your policy’s efficiency by accelerating cash value growth. With the option to use policy dividends or flexible contributions, PUAs can be tailored to fit different income levels and financial goals—without overextending your budget.

- Misconception 3: “PUAs aren’t necessary for wealth building”

Reality: PUAs are a key component of a high-performing whole life insurance strategy. They enhance liquidity, borrowing power, and compound growth—essential elements of building tax-advantaged wealth outside of traditional markets. Without PUAs, your policy may grow much slower and offer less flexibility.

FAQs

Understanding how Paid-Up Additions (PUAs) work can unlock powerful advantages in your Whole Life Insurance policy. Below are some of the most frequently asked questions from clients who want to maximize their policy’s living benefits and long-term performance using this strategy.

What are Paid-Up Additions in life insurance?

Paid-Up Additions are small pieces of permanent life insurance that can be added to your base Whole Life policy. Each PUA increases both your death benefit and cash value, offering immediate and compounding benefits. PUAs can be purchased using policy dividends, out-of-pocket contributions, or a combination of both.

How do Paid-Up Additions grow your policy’s value?

PUAs begin earning guaranteed interest and potential dividends as soon as they are added to your policy. This accelerates your cash value growth from day one and enhances your long-term liquidity. Over time, these additions create more borrowing power and expand your policy’s legacy potential.

What are the benefits of using Paid-Up Additions?

Paid-Up additions help:

- Increase cash value faster than base premiums alone

- Boost your total death benefit automatically

- Create more flexibility through accessible policy loans

- Strengthen your ability to self-finance and support long-term goals. They are a cornerstone of the Perpetual Wealth Strategy™ because they compound value while maintaining stability.

Are Paid-Up Additions only funded by dividends?

No. While dividends are a common way to fund PUAs, many policyholders choose to make out-of-pocket contributions to add PUAs manually—especially in the early years of a policy to build cash value more rapidly.

Do PUAs impact your policy’s performance?

Yes—in a positive way. PUAs directly increase the cash value and death benefit, and they’re especially effective when used strategically. However, it’s important to work with a professional to ensure your PUAs are structured in a way that aligns with your financial goals and doesn’t trigger a MEC (Modified Endowment Contract).

Can I stop adding PUAs at any time?

Yes. PUAs are completely optional and flexible. You can scale contributions up or down—or pause them altogether—based on your current needs and budget.

Are there any downsides to using PUAs?

When structured properly, there are very few downsides. The most important consideration is making sure your policy doesn’t exceed IRS limits and become a MEC. A Wealth Strategist at Paradigm Life can ensure your PUAs are optimized within legal guidelines.

How do I know if Paid-Up Additions are right for me?

If your goal is to grow cash value faster, increase long-term liquidity, or create a private banking system using Whole Life Insurance, then Paid-Up Additions are likely an excellent fit. They’re especially useful for individuals focused on financial independence, retirement planning, and multi-generational wealth building.

Talk to a Paradigm Life Wealth Strategist

Paid-Up Additions are one of the most powerful ways to enhance your Whole Life Insurance policy—fueling early cash value growth, increasing long-term flexibility, and supporting the core principles of the Perpetual Wealth Strategy™. If you’re ready to see how PUAs can help you build lasting wealth and liquidity, speak with a Paradigm Life Wealth Strategist.

Request a custom illustration or ask questions—no pressure, just expert guidance tailored to your goals.

For more information read Agent Ryan Lee’s blog about the ‘PUA’ entitled “What is it Good For?”